S-ar putea să vă placă și

- Tax Sales for Rookies: A Beginner’s Guide to Understanding Property Tax SalesDe la EverandTax Sales for Rookies: A Beginner’s Guide to Understanding Property Tax SalesÎncă nu există evaluări

- Loan Agreement Paperwork of $5000.00Document8 paginiLoan Agreement Paperwork of $5000.00Alex SpecimenÎncă nu există evaluări

- Middle & Back Office Treasury ManagementDocument3 paginiMiddle & Back Office Treasury Managementlinkrink68890% (2)

- Commercial Law (UCC 3, 4, 9)Document23 paginiCommercial Law (UCC 3, 4, 9)Victoria Liu0% (1)

- Customs ActDocument43 paginiCustoms ActAbhishek AgarwalÎncă nu există evaluări

- Torts, Negligence and Product Liability Chapter 7 (2ed)Document32 paginiTorts, Negligence and Product Liability Chapter 7 (2ed)api-522706100% (5)

- Customs DutyDocument17 paginiCustoms DutyBabasab Patil (Karrisatte)100% (1)

- Import Procedure - TanzaniaDocument4 paginiImport Procedure - TanzaniaSam RamÎncă nu există evaluări

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionDe la EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionÎncă nu există evaluări

- Government ProcurementDocument4 paginiGovernment ProcurementPauline Vistan GarciaÎncă nu există evaluări

- Joint Venture Agreement - DRAFT CriptocurrencyDocument10 paginiJoint Venture Agreement - DRAFT CriptocurrencyTomás González CuervoÎncă nu există evaluări

- Agreement For Distributorship MDH DistributorshipDocument5 paginiAgreement For Distributorship MDH DistributorshipDrv LimtedÎncă nu există evaluări

- NestleDocument14 paginiNestleSiddharth Sourav PadheeÎncă nu există evaluări

- Export Assmnt and ExamnDocument33 paginiExport Assmnt and Examnpavan kumar gothwalÎncă nu există evaluări

- 9 Role of Customs in Regulating International TradeDocument36 pagini9 Role of Customs in Regulating International Tradesukriti bajpaiÎncă nu există evaluări

- Tax 4Document33 paginiTax 4Thái Minh ChâuÎncă nu există evaluări

- Goods Subject For Consumption Under Formal Entry ProcessDocument13 paginiGoods Subject For Consumption Under Formal Entry ProcessElaine Antonette RositaÎncă nu există evaluări

- Coffee Importers in KoreaDocument22 paginiCoffee Importers in KoreazmahfudzÎncă nu există evaluări

- Chapter 3 Import Policy of BDDocument25 paginiChapter 3 Import Policy of BDArafat RahmanÎncă nu există evaluări

- Ley de Nigeria PDFDocument12 paginiLey de Nigeria PDFElena RSÎncă nu există evaluări

- UntitledDocument26 paginiUntitledsuyash dugarÎncă nu există evaluări

- Import RegulationsDocument3 paginiImport RegulationsNehal SarhanÎncă nu există evaluări

- MIS CustomsDocument9 paginiMIS Customsشمائل میرÎncă nu există evaluări

- Ata Carnet Guidelines BookletDocument12 paginiAta Carnet Guidelines Bookletkishore13Încă nu există evaluări

- CustomsDocument34 paginiCustomsRachna Jayaraghav100% (1)

- Mamta BhushanDocument26 paginiMamta BhushanDinesh HegdeÎncă nu există evaluări

- International TradeDocument21 paginiInternational Tradenkhokha3931Încă nu există evaluări

- Sri Lank ADocument6 paginiSri Lank AKelz YouknowmynameÎncă nu există evaluări

- Historical Development of The Customs Act and Customs DutyDocument47 paginiHistorical Development of The Customs Act and Customs Dutysuyash dugarÎncă nu există evaluări

- Assessment of EXPORT Credit Requirement.Document22 paginiAssessment of EXPORT Credit Requirement.Anantharaman Rajesh0% (2)

- Import: ClearanceDocument30 paginiImport: Clearancesethupathy sÎncă nu există evaluări

- Vietnam: Goods Documents Required Customs Prescriptions RemarksDocument6 paginiVietnam: Goods Documents Required Customs Prescriptions RemarksKelz YouknowmynameÎncă nu există evaluări

- Customs Duty Note (International Finance)Document7 paginiCustoms Duty Note (International Finance)GODBARÎncă nu există evaluări

- ZambiaDocument2 paginiZambiaKelz YouknowmynameÎncă nu există evaluări

- Import Procurement Process in SAP MMDocument1 paginăImport Procurement Process in SAP MMJayabalaji GÎncă nu există evaluări

- Procesos Aduaneros: Semana 6 DrawbackDocument28 paginiProcesos Aduaneros: Semana 6 DrawbackSabrina MalarinÎncă nu există evaluări

- Export Incentives in IndiaDocument12 paginiExport Incentives in IndiaFasee NunuÎncă nu există evaluări

- Basic Customs Procedure-SHORTDocument27 paginiBasic Customs Procedure-SHORTOmerÎncă nu există evaluări

- ImpEx 11 - 12Document18 paginiImpEx 11 - 12Nasir HussainÎncă nu există evaluări

- Import Procedure: Prof. C. K. SreedharanDocument68 paginiImport Procedure: Prof. C. K. Sreedharanamiit_pandey3503Încă nu există evaluări

- Basic Customs Procedures, Including Trade Facilitation in BangladeshDocument29 paginiBasic Customs Procedures, Including Trade Facilitation in BangladeshArifur Rahman MunnaÎncă nu există evaluări

- 3 Customs ActDocument26 pagini3 Customs ActHaritaa Varshini BalakumaranÎncă nu există evaluări

- Central Sales TaxDocument30 paginiCentral Sales TaxkhiraniektaÎncă nu există evaluări

- Overview of Goods and Services Tax (GST) in Malaysia and Risk ManagementDocument47 paginiOverview of Goods and Services Tax (GST) in Malaysia and Risk ManagementDanish LeongÎncă nu există evaluări

- Actividad de Aprendizaje 10 Evidencia 6 InglesDocument11 paginiActividad de Aprendizaje 10 Evidencia 6 InglesMaria Emilcen Sanchez UribeÎncă nu există evaluări

- UNIT - 2custom and Central ExciseDocument25 paginiUNIT - 2custom and Central ExciseShishir Bharti StudentÎncă nu există evaluări

- Custome Process - Advances Commercial InformationDocument37 paginiCustome Process - Advances Commercial Informationreme moÎncă nu există evaluări

- 2 .The Invoice 2.1 Types of InvoiceDocument3 pagini2 .The Invoice 2.1 Types of InvoiceIfrah SajidaÎncă nu există evaluări

- SIMS Exim ManagementDocument56 paginiSIMS Exim ManagementRounaq DharÎncă nu există evaluări

- EOU Audit ChecksDocument5 paginiEOU Audit Checksశ్రీనివాసకిరణ్కుమార్చతుర్వేదులÎncă nu există evaluări

- Custom DutyDocument17 paginiCustom DutyMubbashir Khan RanaÎncă nu există evaluări

- Finance DepartmentDocument16 paginiFinance DepartmentAkriti SrivastavaÎncă nu există evaluări

- Bill of Entry: - Evidence of Import in ToDocument16 paginiBill of Entry: - Evidence of Import in TosantoshÎncă nu există evaluări

- Thailand Customs Information Foreign Citizens: Documents RequiredDocument4 paginiThailand Customs Information Foreign Citizens: Documents RequiredsnowgardÎncă nu există evaluări

- Import / Export Policy & Procedures: Zewdu LDocument17 paginiImport / Export Policy & Procedures: Zewdu LZewdu Lake TÎncă nu există evaluări

- Fedex Import Clearance Guide en inDocument3 paginiFedex Import Clearance Guide en inSanskarÎncă nu există evaluări

- Country India LocalizationDocument19 paginiCountry India Localizationmksingh_24Încă nu există evaluări

- 2015 VAT in Cambodia Sesion II 22aug 2015Document27 pagini2015 VAT in Cambodia Sesion II 22aug 2015Sovanna HangÎncă nu există evaluări

- Workshop On Finance For Non-Finance Executives: Mining & BeneficiationDocument36 paginiWorkshop On Finance For Non-Finance Executives: Mining & BeneficiationSaikumar SelaÎncă nu există evaluări

- EXPORT Procedure (Basic) in Sri LankaDocument6 paginiEXPORT Procedure (Basic) in Sri Lankapreassess100% (3)

- Duty Drawback Ebook 6.3.20Document12 paginiDuty Drawback Ebook 6.3.20Ratnakar moreÎncă nu există evaluări

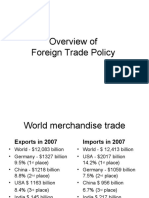

- Foreign Trade PolicyDocument26 paginiForeign Trade PolicySamuel Aravind GunnabathulaÎncă nu există evaluări

- Indirect Tax - Customs DutyDocument22 paginiIndirect Tax - Customs Dutyshiva977Încă nu există evaluări

- Main Features of VATDocument3 paginiMain Features of VATSiva Subramanian100% (2)

- 3 Import ManagementDocument30 pagini3 Import ManagementExim ConsultantsÎncă nu există evaluări

- Export Process in ColombiaDocument23 paginiExport Process in ColombiaFrank QuinteroÎncă nu există evaluări

- The ContractDocument18 paginiThe Contractapi-522706Încă nu există evaluări

- WEEK 8 Dispute Settlement Details Mar 3 5 7 08 Chapter 11Document7 paginiWEEK 8 Dispute Settlement Details Mar 3 5 7 08 Chapter 11api-522706100% (3)

- The ProposalDocument18 paginiThe Proposalapi-522706100% (1)

- The European UnionDocument9 paginiThe European Unionapi-522706Încă nu există evaluări

- US BusinessLawDocument13 paginiUS BusinessLawapi-522706100% (1)

- Chapter 10 (2ed) 2Document12 paginiChapter 10 (2ed) 2api-522706Încă nu există evaluări

- Foreign Direct Investment and Political RiskDocument23 paginiForeign Direct Investment and Political Riskapi-522706100% (4)

- Regional Trade Groupings 2Document8 paginiRegional Trade Groupings 2api-522706100% (1)

- Chapter 11 (2ed)Document14 paginiChapter 11 (2ed)api-522706Încă nu există evaluări

- Creation of A Joint VentureDocument3 paginiCreation of A Joint Ventureapi-522706Încă nu există evaluări

- NAFTA CertificateDocument2 paginiNAFTA Certificateapi-522706100% (4)

- Intellectual PropertyDocument11 paginiIntellectual Propertyapi-522706Încă nu există evaluări

- Chapter 10 (2ed) 3Document16 paginiChapter 10 (2ed) 3api-522706Încă nu există evaluări

- Chapter 2 (2ed)Document18 paginiChapter 2 (2ed)api-522706Încă nu există evaluări

- Chapter 9 (2ed)Document12 paginiChapter 9 (2ed)api-522706Încă nu există evaluări

- Chapter 10 (2ed) 1Document20 paginiChapter 10 (2ed) 1api-522706Încă nu există evaluări

- Chapter 6 (2ed)Document24 paginiChapter 6 (2ed)api-522706Încă nu există evaluări

- Chapter 7 (2ed)Document29 paginiChapter 7 (2ed)api-522706100% (1)

- Chapter 7 (2ed) 2Document7 paginiChapter 7 (2ed) 2api-522706100% (1)

- Chapter 1 (2ed)Document23 paginiChapter 1 (2ed)api-522706100% (1)

- USCustoms Bonds FTZDocument26 paginiUSCustoms Bonds FTZapi-522706100% (1)

- USCustoms 1 TopostDocument31 paginiUSCustoms 1 Topostapi-522706Încă nu există evaluări

- Chapter 8 (2ed)Document24 paginiChapter 8 (2ed)api-522706Încă nu există evaluări

- Chapter 5 (2ed) 2Document13 paginiChapter 5 (2ed) 2api-522706Încă nu există evaluări

- NAFTA3Document42 paginiNAFTA3api-522706100% (1)

- NAFTA3 ADocument10 paginiNAFTA3 Aapi-522706Încă nu există evaluări

- Wto & WcoDocument18 paginiWto & Wcoapi-522706100% (1)

- NAFTA2 ApostDocument23 paginiNAFTA2 Apostapi-522706Încă nu există evaluări

- Nafta 1Document15 paginiNafta 1api-522706100% (1)

- ThesisDocument104 paginiThesisJerry B CruzÎncă nu există evaluări

- Marginal Costing Home AssignmentDocument8 paginiMarginal Costing Home AssignmentRakshaÎncă nu există evaluări

- ECON 1012 - Market Power, RevisedDocument63 paginiECON 1012 - Market Power, RevisedTami GayleÎncă nu există evaluări

- Tax Rev (Dec22)Document187 paginiTax Rev (Dec22)Hope Tariro91% (11)

- Growth & Changing Structure of Non-Banking Financial InstitutionsDocument14 paginiGrowth & Changing Structure of Non-Banking Financial InstitutionsPuneet KaurÎncă nu există evaluări

- CDMDocument2 paginiCDMi am tadaeiÎncă nu există evaluări

- EU Transition Timeline Whitepaper PDFDocument10 paginiEU Transition Timeline Whitepaper PDFWFreeÎncă nu există evaluări

- Comm3201 Individual Case Study (June 2020)Document3 paginiComm3201 Individual Case Study (June 2020)Scarlett WangÎncă nu există evaluări

- CSR Group Activity - Week 4Document3 paginiCSR Group Activity - Week 4Kenisha ManicksinghÎncă nu există evaluări

- Amazon Case Solution, Strategic Management: Concepts and Cases, 14th Edition by Fred R. DavidDocument11 paginiAmazon Case Solution, Strategic Management: Concepts and Cases, 14th Edition by Fred R. DavidNabeel OpelÎncă nu există evaluări

- Intermediate Accounting Vol 1 4th Edition Lo Solutions ManualDocument40 paginiIntermediate Accounting Vol 1 4th Edition Lo Solutions Manualflynnanselm32fyx1100% (18)

- Online Demo Session - FICO - 14 April 2021Document48 paginiOnline Demo Session - FICO - 14 April 2021Md Mukul HossainÎncă nu există evaluări

- Business Options and Business Plan in Haldwani and KathgodamDocument17 paginiBusiness Options and Business Plan in Haldwani and KathgodamShivam ShardaÎncă nu există evaluări

- Tutorial 7: Capital Budgeting and Valuation With Leverage: Alter The Firm's Debt-Equity RatioDocument8 paginiTutorial 7: Capital Budgeting and Valuation With Leverage: Alter The Firm's Debt-Equity RatioYovna SarayeÎncă nu există evaluări

- Blackrock Special Report - Inflation-Linked Bonds PrimerDocument8 paginiBlackrock Special Report - Inflation-Linked Bonds PrimerGreg JachnoÎncă nu există evaluări

- A Summer Internship Project Report ON "Online Ordering Business"Document35 paginiA Summer Internship Project Report ON "Online Ordering Business"Ankur Guglani50% (2)

- Innovation: Innovated by Professor Vijay Govindarajan, Tuck School of Business, Dartmouth CollegeDocument13 paginiInnovation: Innovated by Professor Vijay Govindarajan, Tuck School of Business, Dartmouth CollegeManikandan SuriyanarayananÎncă nu există evaluări

- Tally Acc TermsDocument22 paginiTally Acc TermsShekhar Chandra SahuÎncă nu există evaluări

- Entrepreneur DevelOpment MCQSDocument12 paginiEntrepreneur DevelOpment MCQSHardik Solanki100% (3)

- Computing Profits LessonDocument22 paginiComputing Profits LessonMYRRH TRAINÎncă nu există evaluări

- Enterprise Integration Point Setup Between People Soft Enterprise Campus Solutions and People Soft Enterprise CRMDocument92 paginiEnterprise Integration Point Setup Between People Soft Enterprise Campus Solutions and People Soft Enterprise CRMmilindsusÎncă nu există evaluări

- Performance Health CheckDocument2 paginiPerformance Health CheckRavi Theja SolletiÎncă nu există evaluări

- BUSI 353 S18 Assignment 6 SOLUTIONDocument4 paginiBUSI 353 S18 Assignment 6 SOLUTIONTanÎncă nu există evaluări