S-ar putea să vă placă și

- Value Chain Management Capability A Complete Guide - 2020 EditionDe la EverandValue Chain Management Capability A Complete Guide - 2020 EditionÎncă nu există evaluări

- Index: S.No Date NO RemarksDocument23 paginiIndex: S.No Date NO RemarksSathya Kamaraj0% (1)

- Cost - Vi SemDocument18 paginiCost - Vi SemAR Ananth Rohith BhatÎncă nu există evaluări

- Ever Blue Apparel LTDDocument19 paginiEver Blue Apparel LTDRinha MuneerÎncă nu există evaluări

- Bhel Case StudyDocument15 paginiBhel Case StudySanjeev SinghÎncă nu există evaluări

- Amul (POM)Document105 paginiAmul (POM)Gurpadam LutherÎncă nu există evaluări

- Internal Reconstruction: by Cheranjit DasDocument20 paginiInternal Reconstruction: by Cheranjit DasCheranjit Das100% (1)

- CA Final Old Syllabus PDFDocument114 paginiCA Final Old Syllabus PDFKovvuri Bharadwaj ReddyÎncă nu există evaluări

- Final Project On: Punjab National Bank ScamDocument22 paginiFinal Project On: Punjab National Bank ScamacharyamalvikaÎncă nu există evaluări

- Buyback of Shares of HulDocument7 paginiBuyback of Shares of HulBoota DeolÎncă nu există evaluări

- Reliance Industries - Wikipedia, The Free EncyclopediaDocument9 paginiReliance Industries - Wikipedia, The Free Encyclopediapaulrulez31570% (2)

- TH THDocument8 paginiTH THM Noaman AkbarÎncă nu există evaluări

- Sandip Voltas ReportDocument43 paginiSandip Voltas ReportsandipÎncă nu există evaluări

- Fifco Usa Brands Breweries Job Application FormDocument6 paginiFifco Usa Brands Breweries Job Application FormAnishaÎncă nu există evaluări

- Cost Accounting Standard On Capacity DeterminationDocument6 paginiCost Accounting Standard On Capacity DeterminationEduardo PatachoÎncă nu există evaluări

- Cash Flow Statement Analysis Hul FinalDocument10 paginiCash Flow Statement Analysis Hul FinalGursimran SinghÎncă nu există evaluări

- Al Shaheer CorporationDocument3 paginiAl Shaheer CorporationTaha IrfanÎncă nu există evaluări

- Amalgamation & Sale of Partnership FirmDocument24 paginiAmalgamation & Sale of Partnership FirmJoshua johnÎncă nu există evaluări

- The Raymond Limited: A Study: Director (Research) ICSI-CCGRT, Navi MumbaiDocument14 paginiThe Raymond Limited: A Study: Director (Research) ICSI-CCGRT, Navi Mumbaioptra ceraÎncă nu există evaluări

- Buy-Back of SharesDocument19 paginiBuy-Back of SharesChirag VashishtaÎncă nu există evaluări

- Kim FullerDocument3 paginiKim FullerVinay GoyalÎncă nu există evaluări

- ITC Report and Accounts 2018Document332 paginiITC Report and Accounts 2018Anonymous DfSizzc4lÎncă nu există evaluări

- Corporate Financial Reporting - Chapter I-1Document18 paginiCorporate Financial Reporting - Chapter I-1Namrata BhaskarÎncă nu există evaluări

- ACC803 Advanced Financial Reporting: Week 2: Financial Statement Preparation and PresentationDocument21 paginiACC803 Advanced Financial Reporting: Week 2: Financial Statement Preparation and PresentationRavinesh PrasadÎncă nu există evaluări

- Exempt IncomeDocument18 paginiExempt IncomeSarvar PathanÎncă nu există evaluări

- Darson Securities PVT LTD Internship ReportDocument90 paginiDarson Securities PVT LTD Internship Report333FaisalÎncă nu există evaluări

- Benefice Limited - Team 5Document16 paginiBenefice Limited - Team 5DEMIÎncă nu există evaluări

- Nov 2019Document39 paginiNov 2019amitha g.sÎncă nu există evaluări

- Numericals On Cost of Capital and Capital StructureDocument2 paginiNumericals On Cost of Capital and Capital StructurePatrick AnthonyÎncă nu există evaluări

- Habib Oil Mills Compensation Management ReportDocument22 paginiHabib Oil Mills Compensation Management Reportsjay cwÎncă nu există evaluări

- Dabur India-CorporateGovernance ReportDocument24 paginiDabur India-CorporateGovernance ReportRomesh Angom100% (1)

- Beml Project Print OUTDocument144 paginiBeml Project Print OUTanon_196360629Încă nu există evaluări

- Question Income From Salary Solved in ClassDocument4 paginiQuestion Income From Salary Solved in ClassFozle Rabby 182-11-5893Încă nu există evaluări

- Audit of Sole Trader and A Small CompanyDocument14 paginiAudit of Sole Trader and A Small CompanyrupaliÎncă nu există evaluări

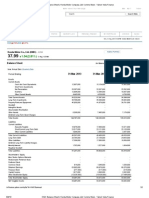

- HMC Balance Sheet - Honda Motor Company, LTD PDFDocument2 paginiHMC Balance Sheet - Honda Motor Company, LTD PDFPoorvi JainÎncă nu există evaluări

- Solved Problems: OlutionDocument5 paginiSolved Problems: OlutionSavoir PenÎncă nu există evaluări

- Ril Case StudyDocument2 paginiRil Case StudyHema Sharist100% (1)

- Long-Term Financial Planning and Growth Chap4Document39 paginiLong-Term Financial Planning and Growth Chap4spectrum_48Încă nu există evaluări

- Mbo HerohondaDocument22 paginiMbo HerohondavithanibharatÎncă nu există evaluări

- Colgate-Palmolive Annual Report 2011Document64 paginiColgate-Palmolive Annual Report 2011Marium Khan100% (2)

- Working Capital MGTDocument14 paginiWorking Capital MGTrupaliÎncă nu există evaluări

- Bu Shivani Report 4Document31 paginiBu Shivani Report 4Shivani AgarwalÎncă nu există evaluări

- Assessment of Tax For FirmsDocument18 paginiAssessment of Tax For FirmsOrko AbirÎncă nu există evaluări

- Cash Flows IIDocument16 paginiCash Flows IIChristian EstebanÎncă nu există evaluări

- A Study of Memorandum of Association and Articles of AssociationDocument6 paginiA Study of Memorandum of Association and Articles of AssociationJyoti Arvind PathakÎncă nu există evaluări

- Lecture Note-Foreign SubsidiaryDocument10 paginiLecture Note-Foreign Subsidiaryptnyagortey91Încă nu există evaluări

- Utkarsh FinalDocument32 paginiUtkarsh FinalSunit ShandilyaÎncă nu există evaluări

- The Cryptms Group-V3 (1) 2Document16 paginiThe Cryptms Group-V3 (1) 2Kavita BaeetÎncă nu există evaluări

- Punit Sahu PPT On RanbaxyDocument24 paginiPunit Sahu PPT On Ranbaxypunitsahu5Încă nu există evaluări

- Gul Ahmed Annual Report 2007Document73 paginiGul Ahmed Annual Report 2007AISHASABAHATÎncă nu există evaluări

- BRM0012 - Consumer's Perception On Inverters in IndiaDocument3 paginiBRM0012 - Consumer's Perception On Inverters in Indiavarun kumar Verma0% (2)

- Human Resource Management: Textile Institue of PakistanDocument19 paginiHuman Resource Management: Textile Institue of PakistanSaba FatmiÎncă nu există evaluări

- Accounting and Taxation AspectsDocument25 paginiAccounting and Taxation Aspectsankit varunÎncă nu există evaluări

- Amalgamation VS AbsorptionDocument7 paginiAmalgamation VS AbsorptionAbhinav RandevÎncă nu există evaluări

- ACCOUNTING-IMPLICATION Merger and AcquisitionDocument32 paginiACCOUNTING-IMPLICATION Merger and AcquisitionPrison PubgÎncă nu există evaluări

- Accounting For AmalgamationsDocument20 paginiAccounting For Amalgamationsrumit2123Încă nu există evaluări

- AmalgamationDocument3 paginiAmalgamationKdlr RRÎncă nu există evaluări

- Accounting Standard - 14Document13 paginiAccounting Standard - 14Manav GuptaÎncă nu există evaluări

- M&a FMSDocument17 paginiM&a FMSfunshareÎncă nu există evaluări

- Amalgamation NoteDocument4 paginiAmalgamation Notekscbwrsyd5Încă nu există evaluări

- ERP Project - FinalDocument66 paginiERP Project - FinalHiral PatelÎncă nu există evaluări

- International BusinessDocument8 paginiInternational BusinessHiral PatelÎncă nu există evaluări

- Management of Financial ServicesDocument346 paginiManagement of Financial ServicesHiral PatelÎncă nu există evaluări

- Basics of Micro FinanceDocument3 paginiBasics of Micro FinanceHiral PatelÎncă nu există evaluări

- CDR Final ProjectDocument65 paginiCDR Final ProjectHiral PatelÎncă nu există evaluări

- GST at 2 YearsDocument36 paginiGST at 2 YearsHiral PatelÎncă nu există evaluări

- Currency and Interest Rate SwapsDocument33 paginiCurrency and Interest Rate SwapsHiral PatelÎncă nu există evaluări

- Jan 2014 IssueDocument124 paginiJan 2014 IssueAshish KumarÎncă nu există evaluări

- Sun - Pharma - Ranbaxy - Nishiyj Desai PDFDocument32 paginiSun - Pharma - Ranbaxy - Nishiyj Desai PDFRajesh KatareÎncă nu există evaluări

- Delivering HappinessDocument18 paginiDelivering HappinessHiral PatelÎncă nu există evaluări

- TATA CommunicationsDocument9 paginiTATA CommunicationsHiral PatelÎncă nu există evaluări

- LarsenDocument11 paginiLarsenHiral PatelÎncă nu există evaluări

- Zero To One1Document10 paginiZero To One1Hiral Patel0% (1)

- Crisis - Html?utm SourceDocument9 paginiCrisis - Html?utm SourceHiral PatelÎncă nu există evaluări

- ERP Implementation LifecycleDocument31 paginiERP Implementation LifecycleRaj ShekharÎncă nu există evaluări

- Direct Taxes Code 2013Document11 paginiDirect Taxes Code 2013Hiral PatelÎncă nu există evaluări

- Brad Stone, The Everything Store: Jeff Bezos and The Age of Amazon. New York: Little Brown, 2013. $28 ClothDocument14 paginiBrad Stone, The Everything Store: Jeff Bezos and The Age of Amazon. New York: Little Brown, 2013. $28 ClothHiral PatelÎncă nu există evaluări

- FY16 Budget - DeloitteDocument50 paginiFY16 Budget - Deloittevivek_bansal_24Încă nu există evaluări

- Mini Project On Goods and Services TaxDocument26 paginiMini Project On Goods and Services TaxHiral Patel20% (5)

- Management Style of Sir Richard BransonDocument7 paginiManagement Style of Sir Richard BransonHiral PatelÎncă nu există evaluări

- Project Report On GSTDocument32 paginiProject Report On GSTHiral Patel50% (4)

- Goods and Services TaxDocument35 paginiGoods and Services TaxHiral PatelÎncă nu există evaluări

- Book Review - Delivering HappinessDocument18 paginiBook Review - Delivering HappinessHiral PatelÎncă nu există evaluări

- Carton, Adam & Sammon - ERP ImplementainDocument19 paginiCarton, Adam & Sammon - ERP ImplementainHiral PatelÎncă nu există evaluări

- Management of Financial ServicesDocument346 paginiManagement of Financial ServicesHiral PatelÎncă nu există evaluări

- Direc Tax Code 2010Document29 paginiDirec Tax Code 2010Hiral PatelÎncă nu există evaluări

- Jan 2014 IssueDocument124 paginiJan 2014 IssueAshish KumarÎncă nu există evaluări

- Value Chain AnalysisDocument33 paginiValue Chain AnalysisAbhinav GoelÎncă nu există evaluări

- Latest Development in GSTDocument11 paginiLatest Development in GSTHiral PatelÎncă nu există evaluări

- Crusader Castle Al-Karak Jordan Levant Pagan Fulk, King of Jerusalem MoabDocument3 paginiCrusader Castle Al-Karak Jordan Levant Pagan Fulk, King of Jerusalem MoabErika CalistroÎncă nu există evaluări

- Subject: PSCP (15-10-19) : Syllabus ContentDocument4 paginiSubject: PSCP (15-10-19) : Syllabus ContentNikunjBhattÎncă nu există evaluări

- MotorsDocument116 paginiMotorsAmália EirezÎncă nu există evaluări

- Schermer 1984Document25 paginiSchermer 1984Pedro VeraÎncă nu există evaluări

- Purposive Communication Preliminary DiscussionDocument2 paginiPurposive Communication Preliminary DiscussionJohn Mark100% (1)

- Catch Up RPHDocument6 paginiCatch Up RPHபிரதீபன் இராதேÎncă nu există evaluări

- Windows Insider ProgramDocument10 paginiWindows Insider ProgramVasileBurcuÎncă nu există evaluări

- Carbonate Platform MateriDocument8 paginiCarbonate Platform MateriNisaÎncă nu există evaluări

- Company Registration Procedure Handbook in Cambodia, EnglishDocument124 paginiCompany Registration Procedure Handbook in Cambodia, EnglishThea100% (16)

- Thompson, Damon - Create A Servitor - How To Create A Servitor and Use The Power of Thought FormsDocument49 paginiThompson, Damon - Create A Servitor - How To Create A Servitor and Use The Power of Thought FormsMike Cedersköld100% (5)

- Characteristics of Trochoids and Their Application To Determining Gear Teeth Fillet ShapesDocument14 paginiCharacteristics of Trochoids and Their Application To Determining Gear Teeth Fillet ShapesJohn FelemegkasÎncă nu există evaluări

- Project On Mahindra BoleroDocument35 paginiProject On Mahindra BoleroViPul75% (8)

- ITCNASIA23 - Visitor GuideDocument24 paginiITCNASIA23 - Visitor Guideibrahim shabbirÎncă nu există evaluări

- International Business ManagementDocument3 paginiInternational Business Managementkalaiselvi_velusamyÎncă nu există evaluări

- OnTime Courier Software System Requirements PDFDocument1 paginăOnTime Courier Software System Requirements PDFbilalÎncă nu există evaluări

- State Farm Claims: PO Box 52250 Phoenix AZ 85072-2250Document2 paginiState Farm Claims: PO Box 52250 Phoenix AZ 85072-2250georgia ann polley-yatesÎncă nu există evaluări

- Dashboard - Reveal Math, Grade 4 - McGraw HillDocument1 paginăDashboard - Reveal Math, Grade 4 - McGraw HillTijjani ShehuÎncă nu există evaluări

- Paper 4 Material Management Question BankDocument3 paginiPaper 4 Material Management Question BankDr. Rakshit Solanki100% (2)

- Course: Introduction To Geomatics (GLS411) Group Practical (2-3 Persons in A Group) Practical #3: Principle and Operation of A LevelDocument3 paginiCourse: Introduction To Geomatics (GLS411) Group Practical (2-3 Persons in A Group) Practical #3: Principle and Operation of A LevelalyafarzanaÎncă nu există evaluări

- Chapter 08 MGT 202 Good GovernanceDocument22 paginiChapter 08 MGT 202 Good GovernanceTHRISHIA ANN SOLIVAÎncă nu există evaluări

- Heat Pyqs NsejsDocument3 paginiHeat Pyqs NsejsPocketMonTuberÎncă nu există evaluări

- NZ2016SH (32k) - e - NSC5026D 3.3V +100ppmDocument2 paginiNZ2016SH (32k) - e - NSC5026D 3.3V +100ppmDumarronÎncă nu există evaluări

- 16-ELS-Final-Module 16-08082020Document18 pagini16-ELS-Final-Module 16-08082020jeseca cincoÎncă nu există evaluări

- 2 Calculation ProblemsDocument4 pagini2 Calculation ProblemsFathia IbrahimÎncă nu există evaluări

- Book of IQ TestsDocument124 paginiBook of IQ TestsFox Mango100% (4)

- Ceo DualityDocument3 paginiCeo Dualitydimpi singhÎncă nu există evaluări

- CO 101 Introductory Computing CO 102 Computing LabDocument17 paginiCO 101 Introductory Computing CO 102 Computing Labadityabaid4Încă nu există evaluări

- Verilog GATE AND DATA FLOWDocument64 paginiVerilog GATE AND DATA FLOWPRIYA MISHRAÎncă nu există evaluări

- Papalia Welcome Asl 1 Guidelines 1 1Document14 paginiPapalia Welcome Asl 1 Guidelines 1 1api-403316973Încă nu există evaluări

- Java Edition Data Values - Official Minecraft WikiDocument140 paginiJava Edition Data Values - Official Minecraft WikiCristian Rene SuárezÎncă nu există evaluări