S-ar putea să vă placă și

- 201B 6E Chap001Document61 pagini201B 6E Chap001chanelnguyenÎncă nu există evaluări

- 201B 6E Chap002Document69 pagini201B 6E Chap002chanelnguyenÎncă nu există evaluări

- OLD Cost Model For ManufacturingDocument2 paginiOLD Cost Model For ManufacturingchanelnguyenÎncă nu există evaluări

- 201B 6E Chap001Document61 pagini201B 6E Chap001chanelnguyenÎncă nu există evaluări

- ExfgfgfDocument10 paginiExfgfgfchanelnguyenÎncă nu există evaluări

- Sonnet GesturesDocument1 paginăSonnet GestureschanelnguyenÎncă nu există evaluări

- Chapter 7Document1 paginăChapter 7chanelnguyenÎncă nu există evaluări

- Lecture Slide 1-1 PDFDocument20 paginiLecture Slide 1-1 PDFchanelnguyenÎncă nu există evaluări

- Lecture Slide 1-1 PDFDocument20 paginiLecture Slide 1-1 PDFchanelnguyenÎncă nu există evaluări

- CH 2 Newtons First Law of MotionDocument8 paginiCH 2 Newtons First Law of MotionchanelnguyenÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Go Go International-3Document2 paginiGo Go International-3sahil.goelÎncă nu există evaluări

- Tô Thị Thùy Duyên - 21dh716422Document2 paginiTô Thị Thùy Duyên - 21dh716422Thuỳ DuyênÎncă nu există evaluări

- Date Payment Interest Principal Present Value: Table of AmortizationDocument6 paginiDate Payment Interest Principal Present Value: Table of AmortizationJekoeÎncă nu există evaluări

- Hingur RampurDocument23 paginiHingur RampurJeewanti panchpalÎncă nu există evaluări

- Tally ERP AssignmentDocument42 paginiTally ERP Assignmentdisha_200983% (93)

- Consolidated Income Statement or Statement of Profit or Loss and Other Comprehensive IncomeDocument4 paginiConsolidated Income Statement or Statement of Profit or Loss and Other Comprehensive IncomeOmolaja IbukunÎncă nu există evaluări

- Capitals and LiabilitiesDocument13 paginiCapitals and LiabilitiesVandita KhudiaÎncă nu există evaluări

- AccountingDocument4 paginiAccountinganca9004Încă nu există evaluări

- NISM Investment Adviser Level 1 PDFDocument190 paginiNISM Investment Adviser Level 1 PDFTrinath SharmaÎncă nu există evaluări

- RCM - FaDocument40 paginiRCM - Favikrant durejaÎncă nu există evaluări

- Profit and Loss WorksheetDocument1 paginăProfit and Loss WorksheetNEWS CENTER MaineÎncă nu există evaluări

- Abm1 LPDocument79 paginiAbm1 LPMark Marasigan100% (2)

- Nykaa EDocument7 paginiNykaa EAditya KumarÎncă nu există evaluări

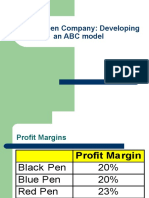

- Classic Pen Company: Developing An ABC ModelDocument22 paginiClassic Pen Company: Developing An ABC Modeljk kumarÎncă nu există evaluări

- Pre Feasibility Business Plan of Poultry Farming in PakistanDocument19 paginiPre Feasibility Business Plan of Poultry Farming in PakistanTanveer100% (1)

- Assignment From Text P2Document3 paginiAssignment From Text P2pedroÎncă nu există evaluări

- TCS 2010 AnalysisDocument22 paginiTCS 2010 AnalysisDilip KumarÎncă nu există evaluări

- H and V Anal ExerciseDocument3 paginiH and V Anal ExerciseSummer ClaronÎncă nu există evaluări

- Anurag ShuklaDocument23 paginiAnurag Shukladeepkamal_jaiswalÎncă nu există evaluări

- Hilton7e SM Ch06 Final RevisedDocument82 paginiHilton7e SM Ch06 Final RevisedJohn100% (4)

- Revenue Recognition Challenges For Disruptive InnovationDocument21 paginiRevenue Recognition Challenges For Disruptive InnovationRishiraj Sisodiya100% (1)

- SAAO As of January 31, 2011Document73 paginiSAAO As of January 31, 2011Budget Department - GenSan LGUÎncă nu există evaluări

- Cash Flow Statement Format 2021Document5 paginiCash Flow Statement Format 2021VV MusicÎncă nu există evaluări

- Lecture-13 Standard Costing Review ProblemDocument22 paginiLecture-13 Standard Costing Review ProblemNazmul-Hassan Sumon67% (3)

- Iebc Act 2011Document29 paginiIebc Act 2011alado lawrenceÎncă nu există evaluări

- DeltaDocument5 paginiDeltahajarzamriÎncă nu există evaluări

- Bikaner Gypsums LTD Edited For PrintDocument9 paginiBikaner Gypsums LTD Edited For Printgrmjain08Încă nu există evaluări

- Topic 4 - Quiz Types of Major Accounts PDFDocument4 paginiTopic 4 - Quiz Types of Major Accounts PDFSarah Santos33% (3)

- Chapter - 12 - Inventory Accounting For Consumable SuppliesDocument10 paginiChapter - 12 - Inventory Accounting For Consumable SuppliesJa Mi LahÎncă nu există evaluări

- Chapter 06 - Intercompany Profit Transactions - Plant AssetsDocument28 paginiChapter 06 - Intercompany Profit Transactions - Plant AssetsTina Lundstrom100% (1)