S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- CASE STUDY of Akhuwat BankDocument3 paginiCASE STUDY of Akhuwat BankabiraÎncă nu există evaluări

- Riya Chawla's Accountant ResumeDocument2 paginiRiya Chawla's Accountant ResumeAbhishek PathakÎncă nu există evaluări

- Property Law - Killi NancwatDocument213 paginiProperty Law - Killi NancwatEsther Oluwaseyitan SodiyaÎncă nu există evaluări

- Which of The Following Is/are An Example(s) of Interest?Document11 paginiWhich of The Following Is/are An Example(s) of Interest?asdfasdfÎncă nu există evaluări

- Oblicon Chap 1 5 Lecture Notes 1Document27 paginiOblicon Chap 1 5 Lecture Notes 1darren chen100% (1)

- 3 - Estate TaxDocument10 pagini3 - Estate TaxVernnÎncă nu există evaluări

- Goldman Sachs Introduction - PDF - Investment Banking - Goldman SachsDocument51 paginiGoldman Sachs Introduction - PDF - Investment Banking - Goldman Sachsdamaxip240Încă nu există evaluări

- Caltex Philippines, Inc. v. Intermediate Appellate Court, G.R. No. 74730, August 25, 1989Document8 paginiCaltex Philippines, Inc. v. Intermediate Appellate Court, G.R. No. 74730, August 25, 1989Anonymous DoJcWEI8HxÎncă nu există evaluări

- Sta. Ignacia Rural Bank Inc. vs. Court of Appeals, 230 SCRA 513Document6 paginiSta. Ignacia Rural Bank Inc. vs. Court of Appeals, 230 SCRA 513MaLizaCainapÎncă nu există evaluări

- Partnership Liquidation (Installment)Document3 paginiPartnership Liquidation (Installment)Johncel TawatÎncă nu există evaluări

- Introduction To Adjusting EntriesDocument1 paginăIntroduction To Adjusting EntriesAnj HwanÎncă nu există evaluări

- Ques No 1.briefly Explain and Illustrate The Concept of Time Value of MoneyDocument15 paginiQues No 1.briefly Explain and Illustrate The Concept of Time Value of MoneyIstiaque AhmedÎncă nu există evaluări

- Multiple Choices QuestionsDocument7 paginiMultiple Choices QuestionsrenoÎncă nu există evaluări

- Special Contracts-1Document7 paginiSpecial Contracts-1GiridharManiyedathÎncă nu există evaluări

- CredTrans - Ablaza V Ignacio - VilloncoDocument3 paginiCredTrans - Ablaza V Ignacio - VilloncoChino VilloncoÎncă nu există evaluări

- UTC - Sept2016 - Restat 2d of Trusts - 203Document2 paginiUTC - Sept2016 - Restat 2d of Trusts - 203OneNationÎncă nu există evaluări

- Economics Assignment - State Bank of IndiaDocument6 paginiEconomics Assignment - State Bank of Indiaananya sharmaÎncă nu există evaluări

- Pledge vs. Chattel Mortgage vs. Real Estate MortgageDocument4 paginiPledge vs. Chattel Mortgage vs. Real Estate MortgageAngelica SumatraÎncă nu există evaluări

- Equity, Trust, FudiciaryDocument28 paginiEquity, Trust, FudiciaryTax NatureÎncă nu există evaluări

- Slidebusinesslaw 160930132004Document19 paginiSlidebusinesslaw 160930132004Rishindran Paramanathan100% (1)

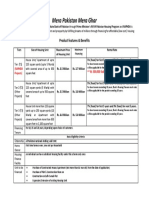

- Mera Pakistan Mera Ghar: Product Features & BenefitsDocument1 paginăMera Pakistan Mera Ghar: Product Features & BenefitsAli Azhar KhanÎncă nu există evaluări

- Stamp DutyDocument4 paginiStamp DutyArushi KumarÎncă nu există evaluări

- Article 1366. There Shall Be No Reformation in The Following CasesDocument6 paginiArticle 1366. There Shall Be No Reformation in The Following CasesKhim Cortez100% (1)

- Commercial Private Equity Announces A Three-Level Loan Program and Customized Financing Options, Helping Clients Close Commercial Real Estate Purchases in A Few DaysDocument4 paginiCommercial Private Equity Announces A Three-Level Loan Program and Customized Financing Options, Helping Clients Close Commercial Real Estate Purchases in A Few DaysPR.comÎncă nu există evaluări

- VILLALVA V RCBC BankDocument1 paginăVILLALVA V RCBC BankNino Kim AyubanÎncă nu există evaluări

- Music Mart Solution - 1decDocument5 paginiMusic Mart Solution - 1decSana LeeÎncă nu există evaluări

- Canlas vs. CA 164 SCRA 160Document7 paginiCanlas vs. CA 164 SCRA 160Marienyl Joan Lopez VergaraÎncă nu există evaluări

- What Is Legal and Technical Verification in Home Loan Processing, NIDHIDocument9 paginiWhat Is Legal and Technical Verification in Home Loan Processing, NIDHIVivek LedwaniÎncă nu există evaluări

- PVL3701 - Definitions and Short QuestionsDocument10 paginiPVL3701 - Definitions and Short QuestionsCoxn EbrahimÎncă nu există evaluări

- DHFL Project Final PDFDocument78 paginiDHFL Project Final PDFChinmay VangeÎncă nu există evaluări