S-ar putea să vă placă și

- Kieso - Inter - ch10 - Ifrs Psak Ppe RevDocument59 paginiKieso - Inter - ch10 - Ifrs Psak Ppe RevJhoÎncă nu există evaluări

- Slide AKT 202 Akuntansi Keuangan Menengah Presentasi 12Document44 paginiSlide AKT 202 Akuntansi Keuangan Menengah Presentasi 12Alan KurniawanÎncă nu există evaluări

- Tugas: English For Accounting (SESSION 12)Document4 paginiTugas: English For Accounting (SESSION 12)Muh Insanul KamilÎncă nu există evaluări

- Accounting For LeasesDocument112 paginiAccounting For LeasesPoomza TaramarukÎncă nu există evaluări

- CH 11Document50 paginiCH 11Mareta Vina ChristineÎncă nu există evaluări

- Intermediate Financial Accounting Chapter 7 SolutionDocument12 paginiIntermediate Financial Accounting Chapter 7 SolutionDrm BluÎncă nu există evaluări

- BAB 2 Analisis TransaksiDocument84 paginiBAB 2 Analisis TransaksiScouter SejatiÎncă nu există evaluări

- Soal Latihan Sia 20192020 Dagang-JasaDocument3 paginiSoal Latihan Sia 20192020 Dagang-JasaJhoni LimÎncă nu există evaluări

- Soal AkuntansiDocument1 paginăSoal Akuntansinidya eka putriÎncă nu există evaluări

- Chapter 2 The Recording ProcessDocument42 paginiChapter 2 The Recording ProcessShihab AhmedÎncă nu există evaluări

- REG.a - Laras Sukma Nurani T - 0320101001 - Tugas 6Document5 paginiREG.a - Laras Sukma Nurani T - 0320101001 - Tugas 6Laras sukma nurani tirtawidjajaÎncă nu există evaluări

- Tugas Sesi 7Document5 paginiTugas Sesi 7mutmainnahÎncă nu există evaluări

- Name: Exercise: Exercise E7-5, Record Sales Gross and Net Course: DateDocument3 paginiName: Exercise: Exercise E7-5, Record Sales Gross and Net Course: DaterahmawÎncă nu există evaluări

- Chapter 1 AccountingDocument64 paginiChapter 1 AccountingMasum HossainÎncă nu există evaluări

- Intermediate: AccountingDocument108 paginiIntermediate: AccountingDieu NguyenÎncă nu există evaluări

- Kieso - Inter - Ch20 - IfRS (Pensions)Document47 paginiKieso - Inter - Ch20 - IfRS (Pensions)hidaÎncă nu există evaluări

- Penngaruh Intensitas Research and Development Dan Keuangan Sebagai Variabel Intervening Pada Perusahaan Lq45 Yang Terdaftar Di Bei Periode 2016-2020Document15 paginiPenngaruh Intensitas Research and Development Dan Keuangan Sebagai Variabel Intervening Pada Perusahaan Lq45 Yang Terdaftar Di Bei Periode 2016-2020Nur WijayantiÎncă nu există evaluări

- Soal Akuntansi Perusahaan JasaDocument2 paginiSoal Akuntansi Perusahaan JasasaharaoaoaÎncă nu există evaluări

- Bab 9 AkmDocument44 paginiBab 9 Akmcaesara geniza ghildaÎncă nu există evaluări

- Akuntansi Kreatif PDFDocument14 paginiAkuntansi Kreatif PDFMarlim JayantaraÎncă nu există evaluări

- Uts Bahasa Inggris Stie1Document2 paginiUts Bahasa Inggris Stie1Tia MitraÎncă nu există evaluări

- Chapter 11-Part 1 Share Transaction Soal 1Document2 paginiChapter 11-Part 1 Share Transaction Soal 1Nicko Arisandiy0% (1)

- Solman Dulu DehDocument3 paginiSolman Dulu Dehbaru uuÎncă nu există evaluări

- Elizar Sinambela (Hal 484-495) - 0Document12 paginiElizar Sinambela (Hal 484-495) - 0banu wicakÎncă nu există evaluări

- Akun PT SEJAHTERADocument2 paginiAkun PT SEJAHTERAYuni MarlinaÎncă nu există evaluări

- Soal Surya Catering Multi Currency PDFDocument9 paginiSoal Surya Catering Multi Currency PDFDestiÎncă nu există evaluări

- Pertemuan Ke-8 - Implementasi Strategi - Manajemen Dan OperasiDocument35 paginiPertemuan Ke-8 - Implementasi Strategi - Manajemen Dan OperasiSalma AufadinaÎncă nu există evaluări

- Intermediate Debt and Leasing: Debagus SubagjaDocument12 paginiIntermediate Debt and Leasing: Debagus SubagjaDebagus SubagjaÎncă nu există evaluări

- Analisis Laporan Keuangan Perusahaan Blue BirdDocument216 paginiAnalisis Laporan Keuangan Perusahaan Blue BirdDini KrisdianiÎncă nu există evaluări

- Daftar Akun Nomor Nama Akun Fungsi Untuk Mencatat Mutasi NilaiDocument4 paginiDaftar Akun Nomor Nama Akun Fungsi Untuk Mencatat Mutasi NilaiFhina LarioÎncă nu există evaluări

- Materi Kuliah 2 - Financial Reporting and AnalysisDocument90 paginiMateri Kuliah 2 - Financial Reporting and Analysisvia nurainiÎncă nu există evaluări

- Intercompany Transfers of Services and Noncurrent AssetsDocument134 paginiIntercompany Transfers of Services and Noncurrent AssetswindyÎncă nu există evaluări

- CH 12Document2 paginiCH 12flrnciairn100% (1)

- FY 2015 MYRX Hanson+International+TbkDocument146 paginiFY 2015 MYRX Hanson+International+TbkFirman HiremaxiÎncă nu există evaluări

- Akuntansi Keuangan Menengah 1Document54 paginiAkuntansi Keuangan Menengah 1Rindi FiaaniÎncă nu există evaluări

- Scott CH 3Document16 paginiScott CH 3RATNIDAÎncă nu există evaluări

- NDocument2 paginiNFreya EvangelineÎncă nu există evaluări

- Kelas A PA1 Matcha Hal 93 Dan 154Document7 paginiKelas A PA1 Matcha Hal 93 Dan 154Kinka NurrindraÎncă nu există evaluări

- CITA Annual Report 2014Document136 paginiCITA Annual Report 2014masitha100% (1)

- Principles of Managerial Finance: Fifteenth Edition, Global EditionDocument22 paginiPrinciples of Managerial Finance: Fifteenth Edition, Global Editionpatrecia 18960% (1)

- Sesi 13 & 14Document15 paginiSesi 13 & 14Dian Permata SariÎncă nu există evaluări

- Istilah Akuntansi DLM Bhs. InggrisDocument6 paginiIstilah Akuntansi DLM Bhs. InggrisBugawatiÎncă nu există evaluări

- Annual Report PT. Jembo Cable Company, TBK 2007Document90 paginiAnnual Report PT. Jembo Cable Company, TBK 2007Rizal KudiartoÎncă nu există evaluări

- PR 14-4A Accounting QuestionsDocument2 paginiPR 14-4A Accounting QuestionsLegnaÎncă nu există evaluări

- E3-5 (LO 3) Adjusting Entries: InstructionsDocument6 paginiE3-5 (LO 3) Adjusting Entries: InstructionsAntonios Fahed0% (1)

- Chapter 10 Credit AnalysisDocument69 paginiChapter 10 Credit AnalysisRobertus GaniÎncă nu există evaluări

- ForumDocument5 paginiForumMariana Hb0% (1)

- Ch01 Financial Reporting and Accounting StandardsDocument27 paginiCh01 Financial Reporting and Accounting StandardsyyanpangÎncă nu există evaluări

- Time Value of Money Assignment A. GutierrezDocument6 paginiTime Value of Money Assignment A. GutierrezTPA TPAÎncă nu există evaluări

- Jurnal Riset Akuntansi & Keuangan: Pengaruh Stock Split Terhadap Likuiditas Emiten Di Bursa Efek IndonesiaDocument10 paginiJurnal Riset Akuntansi & Keuangan: Pengaruh Stock Split Terhadap Likuiditas Emiten Di Bursa Efek IndonesiaJokiÎncă nu există evaluări

- Chapter 14 SolutionsDocument11 paginiChapter 14 Solutionssalsabilla rpÎncă nu există evaluări

- Akun-Akun Dalam English & IndonesiaDocument5 paginiAkun-Akun Dalam English & IndonesiaHachi MiwaÎncă nu există evaluări

- Balance Sheet Completion Using RatiosDocument1 paginăBalance Sheet Completion Using RatiosTrần Thủy VânÎncă nu există evaluări

- PV TablesDocument7 paginiPV Tablesaditi shuklaÎncă nu există evaluări

- Latihan MikroDocument12 paginiLatihan MikroSunny AimezahraÎncă nu există evaluări

- Rangkuman Chapter 9 Cost of CapitalDocument4 paginiRangkuman Chapter 9 Cost of CapitalDwi Slamet RiyadiÎncă nu există evaluări

- Chapter 17 Investasi IFRS MhsDocument49 paginiChapter 17 Investasi IFRS MhsNindy PutriÎncă nu există evaluări

- UNIT 2 (Financial Statements and Ratios) Class DDocument17 paginiUNIT 2 (Financial Statements and Ratios) Class DDinda Yuniar A.Încă nu există evaluări

- Acquisition and Disposition of Property, Plant and EquipmentDocument63 paginiAcquisition and Disposition of Property, Plant and EquipmentKashif Raheem100% (1)

- 7 22 13+Slides+Chapter+10+for+Students+Document88 pagini7 22 13+Slides+Chapter+10+for+Students+etafeyÎncă nu există evaluări

- 1Document22 pagini1Sri Apriyanti HusainÎncă nu există evaluări

- Zhafirah Islamic FashionDocument2 paginiZhafirah Islamic FashionSri Apriyanti HusainÎncă nu există evaluări

- Latihan 1Document1 paginăLatihan 1Sri Apriyanti HusainÎncă nu există evaluări

- Financial Engineering 1-4 DrSami SuwailamDocument20 paginiFinancial Engineering 1-4 DrSami Suwailamjanee8_2k2175Încă nu există evaluări

- Lembar MutabaahDocument2 paginiLembar MutabaahSri Apriyanti HusainÎncă nu există evaluări

- Merino 2005Document36 paginiMerino 2005Sri Apriyanti HusainÎncă nu există evaluări

- Accounting and The EnvironmentDocument7 paginiAccounting and The EnvironmentSri Apriyanti HusainÎncă nu există evaluări

- Takehome Assessment No. 4Document9 paginiTakehome Assessment No. 4Raezel Carla Santos Fontanilla0% (4)

- 2016 Policy Topicality FileDocument164 pagini2016 Policy Topicality FileSeed Rock ZooÎncă nu există evaluări

- Drill Exercises 2Document4 paginiDrill Exercises 2Enerel TumenbayarÎncă nu există evaluări

- 9708 w08 Ms 2 PDFDocument4 pagini9708 w08 Ms 2 PDFKarmen ThumÎncă nu există evaluări

- Business To Business Precise Software Solutions Shyamal Jyoti - ePGP-02-073Document7 paginiBusiness To Business Precise Software Solutions Shyamal Jyoti - ePGP-02-073kg7976Încă nu există evaluări

- Principles of Marketing Diagnostic ExamDocument2 paginiPrinciples of Marketing Diagnostic ExamAlex DrakeÎncă nu există evaluări

- Examination: Subject CT8 Financial Economics Core TechnicalDocument148 paginiExamination: Subject CT8 Financial Economics Core Technicalchan chadoÎncă nu există evaluări

- BSNL Balance SheetDocument15 paginiBSNL Balance SheetAbhishek AgarwalÎncă nu există evaluări

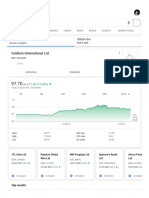

- Goldiam Share - Google SearchDocument5 paginiGoldiam Share - Google SearchDudheshwar SinghÎncă nu există evaluări

- Ogilvy - Social CRM AnalysisDocument49 paginiOgilvy - Social CRM AnalysisFlorin BucaÎncă nu există evaluări

- Sustaining Innovation and Growth Public Policy Support For EntrepreneurshipDocument26 paginiSustaining Innovation and Growth Public Policy Support For EntrepreneurshipAdnan AshrafÎncă nu există evaluări

- Je Uris Sen 2000Document3 paginiJe Uris Sen 2000DikaGustianaÎncă nu există evaluări

- Sparkline Venture CapitalDocument17 paginiSparkline Venture CapitallycancapitalÎncă nu există evaluări

- 20230801052909-SABIC Agri-Nutrients Flash Note Q2-23 enDocument2 pagini20230801052909-SABIC Agri-Nutrients Flash Note Q2-23 enPost PictureÎncă nu există evaluări

- John J Murphy - Technical Analysis of The Financial MarketsDocument547 paginiJohn J Murphy - Technical Analysis of The Financial MarketsJaime González100% (1)

- CRM - Avala Shanmukharao 16016Document11 paginiCRM - Avala Shanmukharao 16016Avala ShanmukharaoÎncă nu există evaluări

- 03 - Management AccountingDocument7 pagini03 - Management AccountingRigner ArandiaÎncă nu există evaluări

- INV1 - Document - Lines1Document13 paginiINV1 - Document - Lines1Ceclie DelfinoÎncă nu există evaluări

- Information Management AssignmentDocument19 paginiInformation Management AssignmentskemuelÎncă nu există evaluări

- Booth Cleary 2nd Edition Chapter 6 - Bond Valuation and Interest RatesDocument93 paginiBooth Cleary 2nd Edition Chapter 6 - Bond Valuation and Interest RatesQurat.ul.ain MumtazÎncă nu există evaluări

- ADMS 4250 - Team I - Round 1Document10 paginiADMS 4250 - Team I - Round 1Naqiya HussainÎncă nu există evaluări

- Economic Order QuantityDocument10 paginiEconomic Order Quantitypapia rahmanÎncă nu există evaluări

- VP Director Finance Securitization in USA Resume Timothy LoganDocument3 paginiVP Director Finance Securitization in USA Resume Timothy LoganTimothyLoganÎncă nu există evaluări

- Tax InvoiceDocument1 paginăTax Invoiceaqib sofiÎncă nu există evaluări

- Chapter 4: Cost Volume Profit Analysis: Garrison, Noreen, BrewerDocument32 paginiChapter 4: Cost Volume Profit Analysis: Garrison, Noreen, Brewernaura syahdaÎncă nu există evaluări

- Fund Distribution & Sales PracticesDocument15 paginiFund Distribution & Sales PracticessidhanthaÎncă nu există evaluări

- ACCT 323 - Stockholder's Equity Project - 100 Points Due April 27 at Midnight ESTDocument2 paginiACCT 323 - Stockholder's Equity Project - 100 Points Due April 27 at Midnight ESTAhmed AdamjeeÎncă nu există evaluări

- Madeviral - Social Media Management ServicesDocument12 paginiMadeviral - Social Media Management ServicesBombom WillkinsonÎncă nu există evaluări

- Coffee Shop Business PlanDocument21 paginiCoffee Shop Business PlanCherry PieÎncă nu există evaluări

- Stone Container Case DiscussionDocument6 paginiStone Container Case DiscussionAvon Jade RamosÎncă nu există evaluări