S-ar putea să vă placă și

- (Assgn&Quiz) - BCADocument1 pagină(Assgn&Quiz) - BCAsonaÎncă nu există evaluări

- (Assgn&Quiz) - BBA BCOMDocument14 pagini(Assgn&Quiz) - BBA BCOMsonaÎncă nu există evaluări

- Bcom IV MeetingsDocument25 paginiBcom IV MeetingssonaÎncă nu există evaluări

- FS Mod 7Document35 paginiFS Mod 7sonaÎncă nu există evaluări

- FS MOD 3 Part 2Document19 paginiFS MOD 3 Part 2sonaÎncă nu există evaluări

- Morning Session: F.S English F.S EnglishDocument4 paginiMorning Session: F.S English F.S EnglishsonaÎncă nu există evaluări

- Arbitration and ConciliationDocument7 paginiArbitration and ConciliationsonaÎncă nu există evaluări

- Risk and ReturnDocument9 paginiRisk and ReturnsonaÎncă nu există evaluări

- Bond ValuationDocument20 paginiBond Valuationsona25% (4)

- Fs Question BankDocument2 paginiFs Question BanksonaÎncă nu există evaluări

- QB - BCM 403 - Regulatory Framework For Companies-Bcom IV-sp-16Document2 paginiQB - BCM 403 - Regulatory Framework For Companies-Bcom IV-sp-16sonaÎncă nu există evaluări

- Entrepreneurship and Small Business Question Bank-Mid Term Exam - Mo15Document1 paginăEntrepreneurship and Small Business Question Bank-Mid Term Exam - Mo15sonaÎncă nu există evaluări

- Legal Aspects of Management Question Bank-Mid Term Exam - Mo15Document2 paginiLegal Aspects of Management Question Bank-Mid Term Exam - Mo15sonaÎncă nu există evaluări

- Monetary Policy and Foreign Exchange RatesDocument61 paginiMonetary Policy and Foreign Exchange RatessonaÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Liquidity ManagementDocument57 paginiLiquidity ManagementShanmuka SreenivasÎncă nu există evaluări

- 86d7fd13-a6d8-461f-9c4c-a5c1ab5ec0ffDocument2 pagini86d7fd13-a6d8-461f-9c4c-a5c1ab5ec0ffnavid kamrava100% (1)

- Nominal v. Real Interest Rates: Macro Topic 4.2Document2 paginiNominal v. Real Interest Rates: Macro Topic 4.2Preksha Borar50% (2)

- Loan Statetement BalajiDocument2 paginiLoan Statetement BalajiSubramanyam JonnaÎncă nu există evaluări

- Banking Sector in IndiaDocument13 paginiBanking Sector in IndiaSamreen Sabiha KaziÎncă nu există evaluări

- Ifsc Codes SbiDocument32 paginiIfsc Codes SbiapjbalamuruganÎncă nu există evaluări

- VENARE Nuvali Sample Computations PromoDocument7 paginiVENARE Nuvali Sample Computations PromoJP ReyesÎncă nu există evaluări

- Dispute FormDocument1 paginăDispute Formadarsh2dayÎncă nu există evaluări

- q2 w8 Business and Consumer LoansDocument20 paginiq2 w8 Business and Consumer Loanshikkiro hikkiÎncă nu există evaluări

- Mini Dissertaion-Research Methods-Group 3Document58 paginiMini Dissertaion-Research Methods-Group 3Najaah RujuballyÎncă nu există evaluări

- Daily Invoice Sales Report20190829Document6 paginiDaily Invoice Sales Report20190829Penchal SaiÎncă nu există evaluări

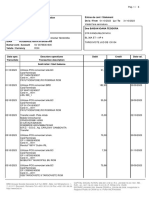

- View SoaDocument6 paginiView SoaJypy Torrejos100% (1)

- What Is Pera AgadDocument5 paginiWhat Is Pera AgadJEFREY JAY CLAUSÎncă nu există evaluări

- TicketsDocument2 paginiTicketsB.K.Sivaraj rajÎncă nu există evaluări

- Report On Dutch Bangla Bank & Ratio AnalysisDocument32 paginiReport On Dutch Bangla Bank & Ratio Analysisolidurrahman33% (3)

- Nominal and Effective Interest RatesDocument3 paginiNominal and Effective Interest RatesMùhammad TàhaÎncă nu există evaluări

- 1LINK Technical Document - Data Element Definitions and Message Format v5.7Document135 pagini1LINK Technical Document - Data Element Definitions and Message Format v5.7hamza rana100% (3)

- Anaalytics FirmsDocument6 paginiAnaalytics FirmsAmit RanaÎncă nu există evaluări

- Regulators and Financial Institutions PDFDocument26 paginiRegulators and Financial Institutions PDFTarun singhÎncă nu există evaluări

- Funds Transfer Form - For Wholesale Banking Customers Only: Debit Account DetailsDocument1 paginăFunds Transfer Form - For Wholesale Banking Customers Only: Debit Account Detailsdon EzeÎncă nu există evaluări

- Fincail Amrkets Analysis For Goverment OfficcialsDocument8 paginiFincail Amrkets Analysis For Goverment OfficcialsmarcoÎncă nu există evaluări

- Teachers Attendance SheetDocument32 paginiTeachers Attendance Sheetpankaj sainiÎncă nu există evaluări

- SV39786361600 2023 10Document6 paginiSV39786361600 2023 10ioanateodorabaisanÎncă nu există evaluări

- R12 Suppliers BankDocument2 paginiR12 Suppliers BankAnton HalimÎncă nu există evaluări

- Affidavit - Credit Card DebtDocument1 paginăAffidavit - Credit Card Debt:Nikolaj: Færch.100% (1)

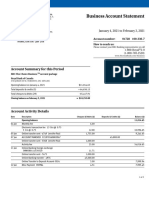

- Business Account Statement: Account Summary For This PeriodDocument2 paginiBusiness Account Statement: Account Summary For This PeriodBrian TalentoÎncă nu există evaluări

- Reading and Use of English-Paper 1-Part5-H-5Document2 paginiReading and Use of English-Paper 1-Part5-H-5Punky Brewster0% (1)

- Statement 11 2023Document3 paginiStatement 11 2023gurdeepdeep136Încă nu există evaluări

- Approved Money Transfer - Western UnionDocument2 paginiApproved Money Transfer - Western Unionhoquangdanh100% (2)

- PDFDocument2 paginiPDFcesar del rosario100% (2)