S-ar putea să vă placă și

- Hotel Master Critical PathDocument14 paginiHotel Master Critical Pathtaola80% (25)

- SAP Intercompany Sales Process Flow & ConfiguationDocument18 paginiSAP Intercompany Sales Process Flow & Configuationsurajit biswas67% (3)

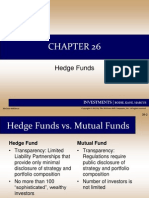

- Chap 026sddDocument33 paginiChap 026sddsatishiitrÎncă nu există evaluări

- Chapter 11 An Introduction To Derivative Markets and SecuritiesDocument29 paginiChapter 11 An Introduction To Derivative Markets and SecuritiesAbraha Girmay Gebru100% (1)

- BFC5935 - Tutorial 10 SolutionsDocument8 paginiBFC5935 - Tutorial 10 SolutionsAlex YisnÎncă nu există evaluări

- WK 4 Emh Tutorial Questions and Solutions PDFDocument5 paginiWK 4 Emh Tutorial Questions and Solutions PDFIlko KacarskiÎncă nu există evaluări

- 02 Oct 2013 Fact SheetDocument1 pagină02 Oct 2013 Fact SheetfaisaladeemÎncă nu există evaluări

- Grile Si RaspunsuriDocument5 paginiGrile Si RaspunsuriCristina ŞtefanÎncă nu există evaluări

- Guide to Contract Pricing: Cost and Price Analysis for Contractors, Subcontractors, and Government AgenciesDe la EverandGuide to Contract Pricing: Cost and Price Analysis for Contractors, Subcontractors, and Government AgenciesÎncă nu există evaluări

- Cost Accounting Research PaperDocument8 paginiCost Accounting Research PaperRoseBing0% (1)

- Haryana Development and Regulation of Urban Areas Act, 1975 PDFDocument45 paginiHaryana Development and Regulation of Urban Areas Act, 1975 PDFLatest Laws TeamÎncă nu există evaluări

- Capstone Project Final Report - PatanjaliDocument60 paginiCapstone Project Final Report - PatanjaliSharvarish Nandanwar0% (1)

- Chapter 3 Fundamentals of Organization StructureDocument21 paginiChapter 3 Fundamentals of Organization StructureKaye Adriana GoÎncă nu există evaluări

- Chapter 17 - Equity Portfolio Management StrategiesDocument35 paginiChapter 17 - Equity Portfolio Management Strategieshajra1989100% (9)

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument23 paginiInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownAS RajuÎncă nu există evaluări

- Investment Analysis and Portfolio Management: Lecture Presentation SoftwareDocument42 paginiInvestment Analysis and Portfolio Management: Lecture Presentation SoftwareAkash SinghÎncă nu există evaluări

- PP25Document53 paginiPP25Tareq RafiÎncă nu există evaluări

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument84 paginiInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownRabia YasmeenÎncă nu există evaluări

- MI Chapter 1 Reilly N BrownDocument39 paginiMI Chapter 1 Reilly N BrownRiRi ChanÎncă nu există evaluări

- Ch18 of Reilly & BrownDocument52 paginiCh18 of Reilly & Brownsubodhagarwal22Încă nu există evaluări

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument29 paginiInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. Brownk.shaikhÎncă nu există evaluări

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument115 paginiInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownKatrina Vianca Decapia100% (1)

- Investment Analysis and Portfolio ManagementDocument33 paginiInvestment Analysis and Portfolio ManagementUqaila Mirza0% (1)

- Investment Analysis and Portfolio Management: Lecture Presentation SoftwareDocument77 paginiInvestment Analysis and Portfolio Management: Lecture Presentation SoftwarekhandakeralihossainÎncă nu există evaluări

- GDB3023 Module2 PDFDocument30 paginiGDB3023 Module2 PDFAisar AmireeÎncă nu există evaluări

- Ch16Investment Analysis and Portfolio ManagementDocument24 paginiCh16Investment Analysis and Portfolio ManagementprasanthmctÎncă nu există evaluări

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument78 paginiInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownNoreenakhtar100% (1)

- Chapter 21 Introduction To Derivative MarketsDocument31 paginiChapter 21 Introduction To Derivative MarketsSarika Thakur100% (1)

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument23 paginiInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownVha AnggrainiÎncă nu există evaluări

- M07 MishkinEakins3427056 08 FMI C07Document58 paginiM07 MishkinEakins3427056 08 FMI C07Declan ShuitÎncă nu există evaluări

- Chapter 2 The Asset Allocation DecisionDocument54 paginiChapter 2 The Asset Allocation Decisiontjsami100% (1)

- Financial Services without Borders: How to Succeed in Professional Financial ServicesDe la EverandFinancial Services without Borders: How to Succeed in Professional Financial ServicesÎncă nu există evaluări

- Tender Process and Evaluation Scieki Wind Park - EnglishDocument6 paginiTender Process and Evaluation Scieki Wind Park - EnglishvelarajanÎncă nu există evaluări

- Chapter 21 - Introduction To Derivative MarketsDocument31 paginiChapter 21 - Introduction To Derivative MarketsSaad KhanÎncă nu există evaluări

- Ch05 Investment Analysis and Portfolio MGT MDocument77 paginiCh05 Investment Analysis and Portfolio MGT MJenilyn VergaraÎncă nu există evaluări

- CH 16 e 9 Country Risk AnalysisDocument16 paginiCH 16 e 9 Country Risk AnalysisanashussainÎncă nu există evaluări

- 7B Analysis of Oil and Gas DisclosuresDocument17 pagini7B Analysis of Oil and Gas DisclosuresAmit Kumar SinghÎncă nu există evaluări

- Ans Foundation of Financial Market and Institution Third Edition by Frank JDocument169 paginiAns Foundation of Financial Market and Institution Third Edition by Frank Japi-26027438Încă nu există evaluări

- Chapter 12Document31 paginiChapter 12Dayittohin JahidÎncă nu există evaluări

- Portfolio Management Process (Condensed)Document17 paginiPortfolio Management Process (Condensed)sadamÎncă nu există evaluări

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument24 paginiInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownAarushi SharmaÎncă nu există evaluări

- Financial Statements & Analysis, The Day Before ExamDocument10 paginiFinancial Statements & Analysis, The Day Before Examsukumar59Încă nu există evaluări

- Financial Crisis PPT FMS 1Document48 paginiFinancial Crisis PPT FMS 1Vikas JaiswalÎncă nu există evaluări

- Capital Market Theory: An OverviewDocument38 paginiCapital Market Theory: An OverviewdevinamisraÎncă nu există evaluări

- Measuring Exposure To Exchange Rate FluctuationsDocument38 paginiMeasuring Exposure To Exchange Rate FluctuationsImroz MahmudÎncă nu există evaluări

- Understanding Capital MarketsDocument15 paginiUnderstanding Capital MarketsSakthirama VadiveluÎncă nu există evaluări

- Equity ValuationDocument38 paginiEquity ValuationkedianareshÎncă nu există evaluări

- Portfolio Management: Lecturer: Th.S. Le Phuoc Thanh (NCS)Document47 paginiPortfolio Management: Lecturer: Th.S. Le Phuoc Thanh (NCS)Eli ZabethÎncă nu există evaluări

- Portfolio ManagementDocument40 paginiPortfolio ManagementSayaliRewaleÎncă nu există evaluări

- Futures and ForwardsDocument14 paginiFutures and ForwardsLeo JohnÎncă nu există evaluări

- Fabozzi Bmas7 Ch23 ImDocument37 paginiFabozzi Bmas7 Ch23 ImSandeep SidanaÎncă nu există evaluări

- Fabozzi Chapter09Document21 paginiFabozzi Chapter09coffeedanceÎncă nu există evaluări

- International Financial ManagementDocument23 paginiInternational Financial Managementsureshmooha100% (1)

- Review Questions - Week 21 - Debt FinancingDocument25 paginiReview Questions - Week 21 - Debt FinancingSuren GiriÎncă nu există evaluări

- PP07final MarkowitzOptimizationDocument62 paginiPP07final MarkowitzOptimizationnadeem.aftab1177Încă nu există evaluări

- Does Exchange Rate Influence Nation's Gross Domestic Product ARDL ApproachDocument9 paginiDoes Exchange Rate Influence Nation's Gross Domestic Product ARDL ApproachInternational Journal of Innovative Science and Research TechnologyÎncă nu există evaluări

- PP20-Bond Portfolio Management (V1)Document21 paginiPP20-Bond Portfolio Management (V1)kegnataÎncă nu există evaluări

- BKM 10e Chap003 SM SelectedDocument6 paginiBKM 10e Chap003 SM SelectedahmedÎncă nu există evaluări

- Answers To End of Chapter Questions and Applications: 3. Imperfect MarketsDocument2 paginiAnswers To End of Chapter Questions and Applications: 3. Imperfect Marketssuhayb_1988Încă nu există evaluări

- PDF - Investment Policy Statement ReviewDocument12 paginiPDF - Investment Policy Statement Reviewmungufeni amosÎncă nu există evaluări

- Econ 132 Problems For Chapter 1-3, and 5Document5 paginiEcon 132 Problems For Chapter 1-3, and 5jononfireÎncă nu există evaluări

- Tut2Sol - Tutorial ONE Tut2Sol - Tutorial ONEDocument6 paginiTut2Sol - Tutorial ONE Tut2Sol - Tutorial ONETrần Trung KiênÎncă nu există evaluări

- BFW 3331 T6 AnswersDocument6 paginiBFW 3331 T6 AnswersDylanchong91Încă nu există evaluări

- SQMP ManualDocument81 paginiSQMP ManualAnkita DwivediÎncă nu există evaluări

- Robert A. Schwartz, John Aidan Byrne, Antoinette Colaninno - Call Auction TradingDocument178 paginiRobert A. Schwartz, John Aidan Byrne, Antoinette Colaninno - Call Auction Tradingpepelmarchas100% (1)

- The High Probability Trading Strategy SummaryDocument2 paginiThe High Probability Trading Strategy SummaryJulius Mark Carinhay TolitolÎncă nu există evaluări

- Presentation On HUL Wal-MartDocument31 paginiPresentation On HUL Wal-MartAmit GuptaÎncă nu există evaluări

- AftaDocument6 paginiAftanurnoliÎncă nu există evaluări

- PolicyBazaar and KuveraDocument18 paginiPolicyBazaar and KuveraBendi YashwanthÎncă nu există evaluări

- Employment Law For BusinessDocument18 paginiEmployment Law For Businesssocimedia300Încă nu există evaluări

- Fifth Semester Commerce Costing (CBCS - 2017 Onwards) : Sub. Code 7BCO5C2Document10 paginiFifth Semester Commerce Costing (CBCS - 2017 Onwards) : Sub. Code 7BCO5C2VELAVAN ARUNADEVIÎncă nu există evaluări

- FM-CPA-001 Corrective Preventif Action Request Rev.02Document2 paginiFM-CPA-001 Corrective Preventif Action Request Rev.02Emy SumartiniÎncă nu există evaluări

- Comparation of Audit ApproachDocument1 paginăComparation of Audit Approachrio HENRYÎncă nu există evaluări

- Diversity and Inclusion in The WorkplaceDocument6 paginiDiversity and Inclusion in The WorkplaceNiMan ShresŤha100% (1)

- ETL Testing White PaperDocument8 paginiETL Testing White PaperKancharlaÎncă nu există evaluări

- Syllabus Opim5770 Spring2015Document2 paginiSyllabus Opim5770 Spring2015amcucÎncă nu există evaluări

- Organizational Strategy - Apple Case StudyDocument31 paginiOrganizational Strategy - Apple Case StudyJamesÎncă nu există evaluări

- International Ch3Document16 paginiInternational Ch3felekebirhanu7Încă nu există evaluări

- Jitendra Prasad: Finance & Accounts ProfessionalDocument2 paginiJitendra Prasad: Finance & Accounts ProfessionalshannabyÎncă nu există evaluări

- Manpower Planning FormDocument1 paginăManpower Planning FormMohammad Abd Alrahim ShaarÎncă nu există evaluări

- Key TermsDocument10 paginiKey Termscuteserese roseÎncă nu există evaluări

- Biological AssetsDocument2 paginiBiological AssetsdorpianabsaÎncă nu există evaluări

- C03 Krugman 12e AccessibleDocument92 paginiC03 Krugman 12e Accessiblesong neeÎncă nu există evaluări

- Struktur Organisasi GZ Kuta-BaliDocument1 paginăStruktur Organisasi GZ Kuta-BalioxiÎncă nu există evaluări

- Dissertation On Commercial BanksDocument4 paginiDissertation On Commercial BanksNeedHelpWithPaperSingapore100% (1)

- Early Career Masters ProgrammesDocument20 paginiEarly Career Masters ProgrammesAnonymous dNcT0IRVÎncă nu există evaluări

- KPIT - Campus Hiring - Management FreshersDocument7 paginiKPIT - Campus Hiring - Management FreshersSwati MishraÎncă nu există evaluări