S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Assignment 1Document5 paginiAssignment 1Prince WamiqÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Assignment 5 BDocument1 paginăAssignment 5 BPrince WamiqÎncă nu există evaluări

- Week 2Document33 paginiWeek 2Prince WamiqÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Week 7Document38 paginiWeek 7Prince WamiqÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Capital Structure Honda Motors Indus Motors - Amount in MillionsDocument3 paginiCapital Structure Honda Motors Indus Motors - Amount in MillionsPrince WamiqÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- 3.3 Population Target 3.4 Sample Size 3.5 VariablesDocument51 pagini3.3 Population Target 3.4 Sample Size 3.5 VariablesPrince WamiqÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Financial Regulation in UKDocument7 paginiFinancial Regulation in UKPrince WamiqÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Honda Atlas Cars AnalysisDocument14 paginiHonda Atlas Cars AnalysisPrince WamiqÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- C18Document74 paginiC18Prince WamiqÎncă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Treasury Management: Week-12, Capital Structure and Company ValuationDocument52 paginiTreasury Management: Week-12, Capital Structure and Company ValuationPrince WamiqÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Basel II and Stress Testing: Week - 11Document19 paginiBasel II and Stress Testing: Week - 11Prince WamiqÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- WTQ CriteriaDocument1 paginăWTQ CriteriaPrince WamiqÎncă nu există evaluări

- Your Opinion CountsDocument2 paginiYour Opinion CountsPrince WamiqÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Assignment #1 Applied Financial EconomicsDocument1 paginăAssignment #1 Applied Financial EconomicsPrince WamiqÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Kotler Summary PDFDocument238 paginiKotler Summary PDFOmar Hasan100% (3)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- CF AnalysisDocument7 paginiCF AnalysisPrince WamiqÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Book 1Document3 paginiBook 1Prince WamiqÎncă nu există evaluări

- Riset PendidikanDocument27 paginiRiset PendidikanwinentoÎncă nu există evaluări

- Hand SanitizerDocument2 paginiHand SanitizerPrince WamiqÎncă nu există evaluări

- Cource Plan Principles of MarketingDocument10 paginiCource Plan Principles of MarketingPrince WamiqÎncă nu există evaluări

- Matl at 1644Document4 paginiMatl at 1644Prince WamiqÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- BSC IIreg 2011Document6 paginiBSC IIreg 2011Prince WamiqÎncă nu există evaluări

- List of Non-Scheduled Urban Co-Operative Banks Sr. No. Bank Name RO NameDocument102 paginiList of Non-Scheduled Urban Co-Operative Banks Sr. No. Bank Name RO NameSusanÎncă nu există evaluări

- Access Levels in Visa Clarity: Member Project Requestor: Least One User Set-Up As A Member Approver. If Not, ThenDocument10 paginiAccess Levels in Visa Clarity: Member Project Requestor: Least One User Set-Up As A Member Approver. If Not, ThenEmi BaditoiuÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- 2023 Jul 20 - PersonalDocument2 pagini2023 Jul 20 - PersonalCammÎncă nu există evaluări

- Simple and Compound InterestDocument24 paginiSimple and Compound InterestJunrie Mark SumalpongÎncă nu există evaluări

- CBP Circular No. 905Document6 paginiCBP Circular No. 905Daniel Danjur Daguman86% (7)

- Chanda KochharDocument39 paginiChanda KochharviveknayeeÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (120)

- A Study On The Usage of E-Payment System and Its in Uence To Digital Financial Inclusion in Coimbatore District, Tamil NaduDocument11 paginiA Study On The Usage of E-Payment System and Its in Uence To Digital Financial Inclusion in Coimbatore District, Tamil NaduResearch SolutionsÎncă nu există evaluări

- Company ProfileDocument5 paginiCompany ProfileNahed MattarÎncă nu există evaluări

- Philippine Financial SystemDocument14 paginiPhilippine Financial SystemMarie Sheryl FernandezÎncă nu există evaluări

- TD Bank StatementDocument1 paginăTD Bank StatementBaba d100% (2)

- Customer Request and Complaint Form: Please Tick Relevant Request Service Request NumberDocument1 paginăCustomer Request and Complaint Form: Please Tick Relevant Request Service Request NumberDesikanÎncă nu există evaluări

- Account StatementDocument12 paginiAccount StatementGlobal StudioÎncă nu există evaluări

- Letter To All Member Banks of SLBC (UP)Document1 paginăLetter To All Member Banks of SLBC (UP)dadan vishwakarmaÎncă nu există evaluări

- Assignment On Micro FinanceDocument28 paginiAssignment On Micro FinancePriti ManeÎncă nu există evaluări

- Instruction Sheet - GIC-19100468Document5 paginiInstruction Sheet - GIC-19100468Ashraf ShaikhÎncă nu există evaluări

- Working Capital ManagementDocument55 paginiWorking Capital ManagementSamina Ashrabi UpomaÎncă nu există evaluări

- IMF Membership & Sovereign Bonds DataDocument11 paginiIMF Membership & Sovereign Bonds DataZach OselandÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Time Value of MoneyDocument40 paginiTime Value of MoneyAhmedmughalÎncă nu există evaluări

- Tche 303 - Money and Banking Tutorial 9: CurrencyDocument4 paginiTche 303 - Money and Banking Tutorial 9: CurrencyNguyen VyÎncă nu există evaluări

- Gratika Report Pemakaian (All) TeccDocument9 paginiGratika Report Pemakaian (All) Teccipphunk19Încă nu există evaluări

- PBB Bank StatementDocument4 paginiPBB Bank Statementzhi xia100% (1)

- AnnuitiesDocument68 paginiAnnuitiesnimra khaliqÎncă nu există evaluări

- Conference Call Transcript: 2021 Investor Engagement ForumDocument25 paginiConference Call Transcript: 2021 Investor Engagement ForumTvrtko TvrtkoÎncă nu există evaluări

- Swaps - Interest Rate and Currency PDFDocument64 paginiSwaps - Interest Rate and Currency PDFKarishma MittalÎncă nu există evaluări

- Exam Schedule Winter 2018Document1 paginăExam Schedule Winter 2018Muneeb ShahidÎncă nu există evaluări

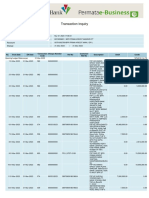

- Permata 1 B9-310323Document2 paginiPermata 1 B9-310323Novi Farah SharfinaÎncă nu există evaluări

- MSB ATM GuidanceDocument3 paginiMSB ATM GuidanceJay CaplanÎncă nu există evaluări

- Jnri Credit 127 Corporation: Promissory NoteDocument3 paginiJnri Credit 127 Corporation: Promissory NoteEra gasperÎncă nu există evaluări

- 37192Document3 pagini37192ARPITHA APPUÎncă nu există evaluări

- January 2022 ExampunditDocument240 paginiJanuary 2022 ExampunditIshang SharmaÎncă nu există evaluări