S-ar putea să vă placă și

- Mobile Africa - 2012Document48 paginiMobile Africa - 2012Tsiggos AlexandrosÎncă nu există evaluări

- Benefits of E-Payment SystemNEWDocument43 paginiBenefits of E-Payment SystemNEWDeepu MssÎncă nu există evaluări

- FINAL DRAFT - Phil E-Commerce Roadmap 2016-2020Document29 paginiFINAL DRAFT - Phil E-Commerce Roadmap 2016-2020Jenny BascunaÎncă nu există evaluări

- Impact of Mobile Money Services On Thegrowth of Smes in BotswanaDocument17 paginiImpact of Mobile Money Services On Thegrowth of Smes in BotswanaDonna MulasiÎncă nu există evaluări

- The Payment SystemDocument19 paginiThe Payment SystemLoredana IrinaÎncă nu există evaluări

- Sfatm Chapter 2Document16 paginiSfatm Chapter 2api-233324921Încă nu există evaluări

- Mobiles For Development - Plan 2009Document48 paginiMobiles For Development - Plan 2009techchangeÎncă nu există evaluări

- Payment Systems in India: Reserve Bank of IndiaDocument16 paginiPayment Systems in India: Reserve Bank of IndiaRahul BadaniÎncă nu există evaluări

- Mobile Money: Matthew N. O. Sadiku, Sarhan M. Musa, and Osama M. MusaDocument4 paginiMobile Money: Matthew N. O. Sadiku, Sarhan M. Musa, and Osama M. MusaEditor IjasreÎncă nu există evaluări

- Mobilink-Network Partial List of PartnersDocument5 paginiMobilink-Network Partial List of PartnersEksdiÎncă nu există evaluări

- AcknowledgementDocument38 paginiAcknowledgementSk PandiÎncă nu există evaluări

- Women and Cyber CrimesDocument9 paginiWomen and Cyber Crimessowmya kÎncă nu există evaluări

- Literature Review - Online ProcessingDocument20 paginiLiterature Review - Online ProcessingSimi StancuÎncă nu există evaluări

- Mobile Payment Systems SeminarDocument26 paginiMobile Payment Systems Seminarkrishnaganth kichaaÎncă nu există evaluări

- ThreatMetrix Cybercrime Defender PlatformDocument3 paginiThreatMetrix Cybercrime Defender PlatformJoshua McAfeeÎncă nu există evaluări

- Mentor: Bless Herera Agapito Cyber Security: ObjectivesDocument2 paginiMentor: Bless Herera Agapito Cyber Security: ObjectivesMelo fi6Încă nu există evaluări

- Internet CrimesDocument17 paginiInternet Crimesfalcon21152115Încă nu există evaluări

- Bitcoin and Cryptocurrency Regulation in The PhilippinesDocument9 paginiBitcoin and Cryptocurrency Regulation in The PhilippinesAnonymous Q0KzFR2iÎncă nu există evaluări

- Payment System Oversight FrameworkDocument16 paginiPayment System Oversight FrameworkNarayanPrajapatiÎncă nu există evaluări

- The Effectiveness of Electronic Payment Transaction On Online Purchasing in Caloocan CityDocument8 paginiThe Effectiveness of Electronic Payment Transaction On Online Purchasing in Caloocan CityLediram Rheyn JulianÎncă nu există evaluări

- Cyber Crime FullDocument24 paginiCyber Crime FullDevendra Ponia100% (1)

- Impact of E-BankingDocument6 paginiImpact of E-Bankingaryaa_statÎncă nu există evaluări

- Can Cybersecurity Framework Implementation Transform From Standard To Innovative?Document30 paginiCan Cybersecurity Framework Implementation Transform From Standard To Innovative?Pratik BhaleraoÎncă nu există evaluări

- Submitted To Submitted byDocument20 paginiSubmitted To Submitted bypreetgodan100% (2)

- Mobile Wallets Key Drivers and Deterrents of Consumers Intention To AdoptDocument30 paginiMobile Wallets Key Drivers and Deterrents of Consumers Intention To AdoptSimon ShresthaÎncă nu există evaluări

- Mobile Banking PPT Pravin and GroupDocument17 paginiMobile Banking PPT Pravin and GroupPravin Shimpi100% (1)

- The Significance of Computer Forensic Analysis To Law Enforcement ProfessionalsDocument4 paginiThe Significance of Computer Forensic Analysis To Law Enforcement ProfessionalsmuyenzoÎncă nu există evaluări

- Dispute Resolution Information Technology Principles Good PracticeDocument29 paginiDispute Resolution Information Technology Principles Good PracticekkÎncă nu există evaluări

- Application of E-Commerce in BankingDocument14 paginiApplication of E-Commerce in Bankingswetanim86% (7)

- P2P-Paid: A Peer-to-Peer Wireless Payment SystemDocument10 paginiP2P-Paid: A Peer-to-Peer Wireless Payment SystemValdi Adrian AbrarÎncă nu există evaluări

- Seminar On Automated Teller MachineDocument15 paginiSeminar On Automated Teller MachineSaad AliÎncă nu există evaluări

- Seapac Philippines Case StudyDocument21 paginiSeapac Philippines Case StudyMark CentenoÎncă nu există evaluări

- UpiDocument14 paginiUpiVegetaÎncă nu există evaluări

- ExpressPay DetailsDocument5 paginiExpressPay DetailsSai PastranaÎncă nu există evaluări

- Cashless Transaction: Modes, Advantages and Disadvantages: January 2017Document5 paginiCashless Transaction: Modes, Advantages and Disadvantages: January 2017Razzelli AnneÎncă nu există evaluări

- Cashless Payment: A Behaviourial Change To Economic GrowthDocument10 paginiCashless Payment: A Behaviourial Change To Economic Growthtasnim100% (2)

- Cyber CrieDocument16 paginiCyber CrieKunal JunejaÎncă nu există evaluări

- Consumer ProtectionDocument14 paginiConsumer ProtectionSabeen Ijaz AhmedÎncă nu există evaluări

- Paytm NewDocument12 paginiPaytm NewPriya Naveen0% (1)

- Bank Using Your NetDocument50 paginiBank Using Your NetKarla BordonesÎncă nu există evaluări

- Research - Paper On Asset MisappropriationDocument17 paginiResearch - Paper On Asset Misappropriationdelhi delhi100% (1)

- Cyber Laws and Ethics, Digital Signature and E-RecordsDocument29 paginiCyber Laws and Ethics, Digital Signature and E-RecordsAnkush Kumar YedeÎncă nu există evaluări

- Using E-Wallet For Business Process Development: Challenges and Prospects in MalaysiaDocument23 paginiUsing E-Wallet For Business Process Development: Challenges and Prospects in MalaysiaMd. Mahmudul AlamÎncă nu există evaluări

- Seminar AtmDocument16 paginiSeminar AtmJasmeet SandhuÎncă nu există evaluări

- E WalletDocument15 paginiE WalletManoj Kumar Paras100% (1)

- An Overview of The Regulatory Framework of FinTech in Nigeria - Fin Tech - Nigeria PDFDocument9 paginiAn Overview of The Regulatory Framework of FinTech in Nigeria - Fin Tech - Nigeria PDFAjiboye TooniÎncă nu există evaluări

- Legal and Ethical Issues of EcommerceDocument15 paginiLegal and Ethical Issues of EcommerceRavi JindalÎncă nu există evaluări

- Money LaunderingDocument24 paginiMoney Launderingmaniv02Încă nu există evaluări

- Nil Act No.2031Document10 paginiNil Act No.2031KarlaColina100% (1)

- Internet Payment & BankingDocument30 paginiInternet Payment & BankingPreeti RanaÎncă nu există evaluări

- Organized Crime Investigation: Topic No. 3 Types of Transnational Crimes: Cyber CrimesDocument42 paginiOrganized Crime Investigation: Topic No. 3 Types of Transnational Crimes: Cyber CrimesdanÎncă nu există evaluări

- Mobile Banking in BangladeshDocument31 paginiMobile Banking in BangladeshCoral AhmedÎncă nu există evaluări

- Automated System in BankingDocument67 paginiAutomated System in BankingRaj RamÎncă nu există evaluări

- 'PPT EcomDocument16 pagini'PPT EcomAYUSHI CHADHAÎncă nu există evaluări

- Tecnology in BankingDocument6 paginiTecnology in BankingShakthi RaghaviÎncă nu există evaluări

- Slow For Micro Payments and Produce High Transaction Costs For Processing Them. Therefore, New Processing Cost, and Widely AcceptableDocument10 paginiSlow For Micro Payments and Produce High Transaction Costs For Processing Them. Therefore, New Processing Cost, and Widely AcceptableAakash RegmiÎncă nu există evaluări

- E-Commerce and Its Application: Unit-IVDocument37 paginiE-Commerce and Its Application: Unit-IVVasa VijayÎncă nu există evaluări

- Unit Iv (Foit)Document48 paginiUnit Iv (Foit)varsha.j2177Încă nu există evaluări

- Unit 3Document23 paginiUnit 3Mahesh NannepaguÎncă nu există evaluări

- Review of Some Online Banks and Visa/Master Cards IssuersDe la EverandReview of Some Online Banks and Visa/Master Cards IssuersÎncă nu există evaluări

- Unix Vs LinuxDocument4 paginiUnix Vs LinuxVijetha bhatÎncă nu există evaluări

- Communication Oriented CommandsDocument16 paginiCommunication Oriented CommandsVijetha bhatÎncă nu există evaluări

- File Oriented Commands in LinuxDocument13 paginiFile Oriented Commands in LinuxVijetha bhatÎncă nu există evaluări

- Process Oriented CommandsDocument13 paginiProcess Oriented CommandsVijetha bhatÎncă nu există evaluări

- Linux Commands BasicsDocument11 paginiLinux Commands BasicsVijetha bhatÎncă nu există evaluări

- Introduction To UnixDocument10 paginiIntroduction To UnixVijetha bhatÎncă nu există evaluări

- Linux DirectoryDocument12 paginiLinux DirectoryVijetha bhatÎncă nu există evaluări

- Securing Network Transactions - Pptx/vijetha BhatDocument27 paginiSecuring Network Transactions - Pptx/vijetha BhatVijetha bhatÎncă nu există evaluări

- Protecting The Network Word Doc/vijetha BhatDocument12 paginiProtecting The Network Word Doc/vijetha BhatVijetha bhat100% (1)

- Ethernet&WAN - Pptx/vijethavinayak BhatDocument17 paginiEthernet&WAN - Pptx/vijethavinayak BhatVijetha bhatÎncă nu există evaluări

- Ms Powerpoint 2007.doc/vijethavinayak BhatDocument17 paginiMs Powerpoint 2007.doc/vijethavinayak BhatVijetha bhat100% (2)

- FTP-Email-WWW-HTTP - Pptx/vijetha BhatDocument19 paginiFTP-Email-WWW-HTTP - Pptx/vijetha BhatVijetha bhatÎncă nu există evaluări

- VAN/benefitsof - EDI - Pptx/vijetha BhatDocument17 paginiVAN/benefitsof - EDI - Pptx/vijetha BhatVijetha bhat100% (1)

- Transmission Media: Types of Media Coaxial Cables Presented By:vijetha V BhatDocument20 paginiTransmission Media: Types of Media Coaxial Cables Presented By:vijetha V BhatVijetha bhatÎncă nu există evaluări

- Swachh Bharath Abhiyan/vijetha BhatDocument20 paginiSwachh Bharath Abhiyan/vijetha BhatVijetha bhat100% (2)

- Protecting THE Network: Prepared By:Vijetha V BhatDocument19 paginiProtecting THE Network: Prepared By:Vijetha V BhatVijetha bhatÎncă nu există evaluări

- Security Policy/vijethavinayak - BhatDocument13 paginiSecurity Policy/vijethavinayak - BhatVijetha bhatÎncă nu există evaluări

- Payment Options: Aesm - Instructions For Online Test Payment and Seat BookingDocument8 paginiPayment Options: Aesm - Instructions For Online Test Payment and Seat BookingSombir AhlawatÎncă nu există evaluări

- 53RD Personal Bank StatementDocument3 pagini53RD Personal Bank StatementKelvin Dominic50% (2)

- E BankingDocument27 paginiE BankingHimanshu KansalÎncă nu există evaluări

- 1579221808448drMLsyEUj3DzHZPx PDFDocument13 pagini1579221808448drMLsyEUj3DzHZPx PDFVuddemarri SivaprasadÎncă nu există evaluări

- Plastic Money IntroDocument70 paginiPlastic Money IntroParm Sidhu100% (13)

- Bank of Maldives: Head Office, Boduthakurufaanu Magu MaleDocument22 paginiBank of Maldives: Head Office, Boduthakurufaanu Magu MalemikeÎncă nu există evaluări

- Debit Mandate Form NACH / ECS / DIRECT DEBIT: Mthly Qtly H-Yrly Yrly As & When PresentedDocument1 paginăDebit Mandate Form NACH / ECS / DIRECT DEBIT: Mthly Qtly H-Yrly Yrly As & When PresentedRajesh KumarÎncă nu există evaluări

- 63 Moons Announces Gen-Next Innovations On ODIN (Company Update)Document2 pagini63 Moons Announces Gen-Next Innovations On ODIN (Company Update)Shyam SunderÎncă nu există evaluări

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument1 paginăStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAdnan sonyÎncă nu există evaluări

- NARUTO Episode 1 - 220Document12 paginiNARUTO Episode 1 - 220Namikaze Minato33% (3)

- Wells Fargo Combined Statement of AccountsDocument6 paginiWells Fargo Combined Statement of AccountsAurica TrifanÎncă nu există evaluări

- Excel TaskDocument27 paginiExcel TaskMark JonesÎncă nu există evaluări

- eStatementFile Mar2018 PDFDocument3 paginieStatementFile Mar2018 PDFAnonymous MV9YvFxhS2Încă nu există evaluări

- Date of Issue: Account Type:: Particulars Debits Balance Date CreditsDocument2 paginiDate of Issue: Account Type:: Particulars Debits Balance Date CreditsmichaelÎncă nu există evaluări

- Payorder PDFDocument1 paginăPayorder PDFrimon444Încă nu există evaluări

- DHBVNDocument1 paginăDHBVNKunal SharmaÎncă nu există evaluări

- XStxoo 7 AE1 JJYZ5 IDocument2 paginiXStxoo 7 AE1 JJYZ5 Inani santhuÎncă nu există evaluări

- January StatDocument5 paginiJanuary StatSkerdi KumriaÎncă nu există evaluări

- STC-NMB BANK - May 2020 PDFDocument13 paginiSTC-NMB BANK - May 2020 PDFaashish koiralaÎncă nu există evaluări

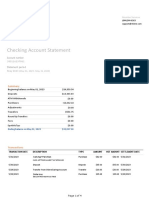

- Checking Account and Debit Card SimulationDocument62 paginiChecking Account and Debit Card SimulationSandra_Zimmerman100% (1)

- Presentation PhonepeDocument7 paginiPresentation PhonepeVineet KumarÎncă nu există evaluări

- Internet Bankingservice of Janata Bank Limited Questionnaire Personal InformationDocument3 paginiInternet Bankingservice of Janata Bank Limited Questionnaire Personal InformationAktarujjaman NasimÎncă nu există evaluări

- Learning Activity 4 / Actividad de Aprendizaje 4 Evidence: Planning My Trip / Evidencia: Organizando Mi ViajeDocument4 paginiLearning Activity 4 / Actividad de Aprendizaje 4 Evidence: Planning My Trip / Evidencia: Organizando Mi ViajeAndres VargasÎncă nu există evaluări

- Geran BSN - Digitalized SystemDocument290 paginiGeran BSN - Digitalized SystemSyahira AzmiÎncă nu există evaluări

- MyTW Bill 475525918821 12 12 2022Document1 paginăMyTW Bill 475525918821 12 12 2022lapenbÎncă nu există evaluări

- Extracted Pages From May-2023Document4 paginiExtracted Pages From May-2023Muhammad UsmanÎncă nu există evaluări

- StatementDocument52 paginiStatementSUSANTA Best VideosÎncă nu există evaluări

- MGVCL New Application Payment ReceiptDocument1 paginăMGVCL New Application Payment ReceiptnysadebtmanagementÎncă nu există evaluări

- Ece 6018 Pli CBSDocument24 paginiEce 6018 Pli CBSNarayanaÎncă nu există evaluări

- Bidvest Bank Sable InternationalDocument4 paginiBidvest Bank Sable InternationalBD MahamudÎncă nu există evaluări