S-ar putea să vă placă și

- Octane Service StationDocument8 paginiOctane Service StationKalyan Kumar83% (6)

- New Frontiers Case Study Analysis orDocument15 paginiNew Frontiers Case Study Analysis orKaushik Mandal90% (10)

- Sneaker 2013Document13 paginiSneaker 2013Hirosha Vejian100% (2)

- Assignment - Group 6 - Case Analysis (Investment Analysis and Lockheed Tristar)Document6 paginiAssignment - Group 6 - Case Analysis (Investment Analysis and Lockheed Tristar)Rajat Gupta100% (4)

- Maynard Company (A) : EXHIBIT 1 Account BalancesDocument2 paginiMaynard Company (A) : EXHIBIT 1 Account Balancesriya lakhotiaÎncă nu există evaluări

- Boulevard Sandwiches, Inc. (A) : FAPC Assignment Group 7Document7 paginiBoulevard Sandwiches, Inc. (A) : FAPC Assignment Group 7Akshay100% (1)

- Management Accounting - I (Section A, B &H) Term I (2021-22)Document3 paginiManagement Accounting - I (Section A, B &H) Term I (2021-22)saurabhÎncă nu există evaluări

- Chemalite SolutionHBSDocument10 paginiChemalite SolutionHBSManoj Singh0% (1)

- Symphony Orchestra Case StudyDocument3 paginiSymphony Orchestra Case StudyBrandon ElkinsÎncă nu există evaluări

- Lockheed Case SolutionDocument3 paginiLockheed Case SolutionKashish SrivastavaÎncă nu există evaluări

- Lockeed 5 StarDocument6 paginiLockeed 5 StarAjay SinghÎncă nu există evaluări

- Investment Analysis and Tri Star Lockheed - FULL FINALDocument8 paginiInvestment Analysis and Tri Star Lockheed - FULL FINALCheytan Thakar100% (3)

- Problem CH 11 Alfi Dan Yessy AKT 18-MDocument4 paginiProblem CH 11 Alfi Dan Yessy AKT 18-MAna Kristiana100% (1)

- NEW Contract To Sell PAG IBIGDocument2 paginiNEW Contract To Sell PAG IBIGMj JavellanaÎncă nu există evaluări

- Lockheed Tristar Case Study 11020241041Document19 paginiLockheed Tristar Case Study 11020241041R Harika Reddy100% (7)

- Chapter 12: Corporate Valuation and Financial Planning: Page 1Document33 paginiChapter 12: Corporate Valuation and Financial Planning: Page 1nouraÎncă nu există evaluări

- Case 01a Growing Pains SolutionDocument7 paginiCase 01a Growing Pains Solution01dynamic33% (3)

- Case 3 Auto AssemblyDocument3 paginiCase 3 Auto Assemblyuzumakhinaruto100% (1)

- Lockheed Tristar ProjectDocument1 paginăLockheed Tristar ProjectDurgaprasad VelamalaÎncă nu există evaluări

- Problem Sets Finacc Chapter 9Document19 paginiProblem Sets Finacc Chapter 9Reg LagartejaÎncă nu există evaluări

- A-CAT Corp. MRP SolnDocument13 paginiA-CAT Corp. MRP SolnAbhishta SharmaÎncă nu există evaluări

- Lilac Flour Mills: Managerial Accounting and Control - IIDocument9 paginiLilac Flour Mills: Managerial Accounting and Control - IISoni Kumari50% (4)

- Accounting Case AnalysisDocument11 paginiAccounting Case Analysissuresh sivadasan0% (1)

- Technology Startup GuideDocument86 paginiTechnology Startup GuidecrinkletizzÎncă nu există evaluări

- Case 4-4 Octane SS - PurwaningrumDocument5 paginiCase 4-4 Octane SS - PurwaningrumPurwaningrum Gunantoko50% (4)

- AkuntansiDocument3 paginiAkuntansier4sallÎncă nu există evaluări

- Chema LiteDocument8 paginiChema LiteHàMềmÎncă nu există evaluări

- Case Study 4 3 Copies ExpressDocument7 paginiCase Study 4 3 Copies Expressamitsemt100% (2)

- Case Study 4 - 3 Copies ExpressDocument8 paginiCase Study 4 - 3 Copies ExpressJZ0% (1)

- Strategic Finance Assignment No 1-Q2-5, B Q2-34 (T.V.O.M) (Solution)Document6 paginiStrategic Finance Assignment No 1-Q2-5, B Q2-34 (T.V.O.M) (Solution)Zahid UsmanÎncă nu există evaluări

- OR Case Study Analysis: - by Aditya Karam (04), Gurjinder Singh (10), Deepti Sana (40), Kaushik Mandal (41), Pankaj BajajDocument15 paginiOR Case Study Analysis: - by Aditya Karam (04), Gurjinder Singh (10), Deepti Sana (40), Kaushik Mandal (41), Pankaj BajajMaria MercadoÎncă nu există evaluări

- Assignment Iii Mansa Building Case Study: Submitted by Group IVDocument14 paginiAssignment Iii Mansa Building Case Study: Submitted by Group IVHeena TejwaniÎncă nu există evaluări

- Exam 2 - PS Answer KeyDocument3 paginiExam 2 - PS Answer KeyAndres AgatoÎncă nu există evaluări

- Case Analysis Rosemont Hill Health Center V3 PDFDocument8 paginiCase Analysis Rosemont Hill Health Center V3 PDFPoorvi SinghalÎncă nu există evaluări

- Chapter 04 Process Costing and Hybrid Product-Costing SystemsDocument21 paginiChapter 04 Process Costing and Hybrid Product-Costing SystemsJc AdanÎncă nu există evaluări

- Solman 12 Second EdDocument23 paginiSolman 12 Second Edferozesheriff50% (2)

- Case of Joneja Bright Steels: The Cash Discount DecisionDocument10 paginiCase of Joneja Bright Steels: The Cash Discount DecisionRHEAÎncă nu există evaluări

- Case Summary WalthamDocument2 paginiCase Summary WalthamAnurag ChatarkarÎncă nu există evaluări

- Amaranth AdvisorsDocument15 paginiAmaranth AdvisorsRani ZahrÎncă nu există evaluări

- Chapter 5 ProblemsDocument7 paginiChapter 5 Problemsanu balakrishnanÎncă nu există evaluări

- Investment Analysis - Lockheed Tri-StarDocument2 paginiInvestment Analysis - Lockheed Tri-Staraclink88100% (1)

- MacDocument4 paginiMacalwar_shi262068100% (1)

- Modern Pharma SolnDocument3 paginiModern Pharma SolnSakshiÎncă nu există evaluări

- Abc QuizDocument24 paginiAbc QuizJhunnel LangubanÎncă nu există evaluări

- Chap 017Document33 paginiChap 017Anthony MaloneÎncă nu există evaluări

- A. Loan Processing Operation: 87.50%: UtilizationDocument36 paginiA. Loan Processing Operation: 87.50%: UtilizationQueenie Marie CastilloÎncă nu există evaluări

- Precision Worldwide, Inc. - Section B - Group 9Document3 paginiPrecision Worldwide, Inc. - Section B - Group 9Varun Baxi100% (4)

- Millichem Solution XDocument6 paginiMillichem Solution XMuhammad JunaidÎncă nu există evaluări

- ASSIGNMENT On Investment Analysis and Lockheed Tristar: SUBMITTED TO: Dr. Debaditya Mohanty Submitted byDocument7 paginiASSIGNMENT On Investment Analysis and Lockheed Tristar: SUBMITTED TO: Dr. Debaditya Mohanty Submitted byAbhisek SarkarÎncă nu există evaluări

- Lockheed Tristar Case AnalysisDocument9 paginiLockheed Tristar Case AnalysispranavÎncă nu există evaluări

- Investment Analysis and Lockheed Tri Star ADocument9 paginiInvestment Analysis and Lockheed Tri Star AEshesh GuptaÎncă nu există evaluări

- Solution To R Haque Associates ProblemDocument8 paginiSolution To R Haque Associates ProblemHasanÎncă nu există evaluări

- Tutorial4 - Sol - New UpdateDocument13 paginiTutorial4 - Sol - New UpdateHa NguyenÎncă nu există evaluări

- 423 BOD & Budget ForecastDocument19 pagini423 BOD & Budget ForecastshariqwaheedÎncă nu există evaluări

- May 2015 Q3Document3 paginiMay 2015 Q3Chahak BhallaÎncă nu există evaluări

- Ent300 - Business Plan - CashDocument2 paginiEnt300 - Business Plan - CashNUR SYAZREEN MOHD JURAINAÎncă nu există evaluări

- Answer - D, E, F, GDocument4 paginiAnswer - D, E, F, GAkash SharmaÎncă nu există evaluări

- Solutions To Chapter 9 ProblemsDocument37 paginiSolutions To Chapter 9 ProblemsMorning KalalÎncă nu există evaluări

- Payroll SummaryDocument3 paginiPayroll Summarynicole.upperÎncă nu există evaluări

- Hola-Kola: Section: E05 Group Number: G04 Name of ParticipantsDocument7 paginiHola-Kola: Section: E05 Group Number: G04 Name of ParticipantsSuvinay SethÎncă nu există evaluări

- Description PT Casio (Induk) PT Kenko (Anak)Document4 paginiDescription PT Casio (Induk) PT Kenko (Anak)OLIVIA CHRISTINAÎncă nu există evaluări

- Tarea 9.1 Problemas Evaluación Proyectos 1 Loera CoronadoDocument12 paginiTarea 9.1 Problemas Evaluación Proyectos 1 Loera CoronadoBrandon LoeraÎncă nu există evaluări

- Chapter 18Document14 paginiChapter 18arwa_mukadam03Încă nu există evaluări

- Chapter 15Document11 paginiChapter 15arwa_mukadam03100% (1)

- Yellowstone National ParkDocument8 paginiYellowstone National Parkarwa_mukadam03Încă nu există evaluări

- Chapter 2 PDFDocument9 paginiChapter 2 PDFarwa_mukadam03Încă nu există evaluări

- CashFlow Exercise NoansDocument5 paginiCashFlow Exercise Noansarwa_mukadam03Încă nu există evaluări

- Finance Management-Week 10Document4 paginiFinance Management-Week 10arwa_mukadam03Încă nu există evaluări

- Finance Management-Week 9Document4 paginiFinance Management-Week 9arwa_mukadam03Încă nu există evaluări

- Finance Management HW Week 4Document7 paginiFinance Management HW Week 4arwa_mukadam03100% (1)

- Finance Management SolutionsDocument10 paginiFinance Management Solutionsarwa_mukadam03Încă nu există evaluări

- Finance Management-Week 8Document12 paginiFinance Management-Week 8arwa_mukadam03Încă nu există evaluări

- Finance Management HW Week 5Document8 paginiFinance Management HW Week 5arwa_mukadam03Încă nu există evaluări

- Week 3-HWDocument19 paginiWeek 3-HWarwa_mukadam03Încă nu există evaluări

- Finance Management - HW-Week 2Document5 paginiFinance Management - HW-Week 2arwa_mukadam03Încă nu există evaluări

- ICICI Transaction SlipDocument1 paginăICICI Transaction Sliparwa_mukadam03Încă nu există evaluări

- Homemade Pizza SandwichDocument2 paginiHomemade Pizza Sandwicharwa_mukadam03Încă nu există evaluări

- Surrender To A Sheikh-OverviewDocument1 paginăSurrender To A Sheikh-Overviewarwa_mukadam03Încă nu există evaluări

- Prince of ScandalDocument1 paginăPrince of Scandalarwa_mukadam03Încă nu există evaluări

- Paneer Chilly RecepieDocument1 paginăPaneer Chilly Recepiearwa_mukadam03Încă nu există evaluări

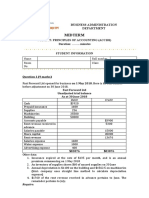

- Midterm: Hoa Lac Subject: Principles of Accounting (Acc101) Duration: .. Minutes Student InformationDocument2 paginiMidterm: Hoa Lac Subject: Principles of Accounting (Acc101) Duration: .. Minutes Student InformationNguyen Ngoc Minh Chau (K15 HL)Încă nu există evaluări

- Ri Kon 6689Document2 paginiRi Kon 6689Chetan VaishnavÎncă nu există evaluări

- Cambridge International General Certificate of Secondary EducationDocument24 paginiCambridge International General Certificate of Secondary EducationbensonÎncă nu există evaluări

- 954 Opening, Relocation and Closure of Branch or Sub Branch OfficesDocument6 pagini954 Opening, Relocation and Closure of Branch or Sub Branch OfficesAddisu Mengist ZÎncă nu există evaluări

- Badla (Stock Trading)Document2 paginiBadla (Stock Trading)BOBBY212Încă nu există evaluări

- Harvesting The Business Venture Investment Chapter 14Document20 paginiHarvesting The Business Venture Investment Chapter 14Trang TranÎncă nu există evaluări

- Cma ArttDocument427 paginiCma ArttMUHAMMAD ALIÎncă nu există evaluări

- G.O.MS - No. 218Document5 paginiG.O.MS - No. 218younusbasha143Încă nu există evaluări

- Entrep (Banana Cake Business)Document4 paginiEntrep (Banana Cake Business)Marjhon Maniego MascardoÎncă nu există evaluări

- A Project Report On Customer Perception and Attitude Towards ICICI Prudential Life InsuranceDocument85 paginiA Project Report On Customer Perception and Attitude Towards ICICI Prudential Life InsuranceBabasab Patil (Karrisatte)100% (1)

- Option PDFDocument4 paginiOption PDFjallwynaldrinÎncă nu există evaluări

- Ali Shahid (ACCA Member UK) Accounts - Finance - Audit: Career ObjectiveDocument2 paginiAli Shahid (ACCA Member UK) Accounts - Finance - Audit: Career ObjectiveIshtiaq Azam50% (2)

- Audit 2 - Concept Map For InvestmentsDocument4 paginiAudit 2 - Concept Map For InvestmentsPrecious Recede100% (1)

- Macro Tut 4 - With AnsDocument11 paginiMacro Tut 4 - With AnsNguyen Tra MyÎncă nu există evaluări

- Chapter 3 FMDocument79 paginiChapter 3 FMHananÎncă nu există evaluări

- Bank of the Philippine Islands, Inc. vs. SPS. Norman and Angelina Yu and Tuanson Builders Corporation (G.R. No. 184122, January 20, 2010)Document2 paginiBank of the Philippine Islands, Inc. vs. SPS. Norman and Angelina Yu and Tuanson Builders Corporation (G.R. No. 184122, January 20, 2010)yyruusheeshhahaÎncă nu există evaluări

- Dawit Final ProposalDocument32 paginiDawit Final ProposalGetu Weyessa0% (1)

- Chapter 2 - Intro To ITDocument12 paginiChapter 2 - Intro To ITMakiri Sajili IIÎncă nu există evaluări

- Chapter 01Document10 paginiChapter 01ShantamÎncă nu există evaluări

- Annual Report 2019 - 2020Document130 paginiAnnual Report 2019 - 2020ermiaslulieÎncă nu există evaluări

- UntitledDocument171 paginiUntitledD2NÎncă nu există evaluări

- Accounting Problem 5Document8 paginiAccounting Problem 5Carlo AniÎncă nu există evaluări

- Monthly Banking/ Financial/ Economic Awareness SagaDocument48 paginiMonthly Banking/ Financial/ Economic Awareness SagaSunday MondayÎncă nu există evaluări

- Prova Do 2º Ano Present Continuous 3º BiDocument2 paginiProva Do 2º Ano Present Continuous 3º BiRaphael RodriguesÎncă nu există evaluări

- The Self-Disruptive LeaderDocument1 paginăThe Self-Disruptive LeaderazrulfadjriÎncă nu există evaluări

- Portfolio Management India InfolineDocument93 paginiPortfolio Management India InfolineVasavi Daram0% (1)

- AC - IntAcctg1 Quiz 04 With AnswersDocument2 paginiAC - IntAcctg1 Quiz 04 With AnswersSherri Bonquin100% (1)