S-ar putea să vă placă și

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document46 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document46 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document62 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document62 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document89 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Operational Risk ManagementDocument27 paginiOperational Risk ManagementdouglasÎncă nu există evaluări

- 03 G3 Annexure B - OR Self Assessment TemplateDocument8 pagini03 G3 Annexure B - OR Self Assessment TemplateTejendrasinh GohilÎncă nu există evaluări

- Risk Based Internal Audit in BanksDocument10 paginiRisk Based Internal Audit in Banksnadim.rashid9849Încă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document73 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- R53 Global BaselIII v1 1Document16 paginiR53 Global BaselIII v1 1douglasÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document39 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Financial Stability and Crises: Microprudential and Macroprudential PolicyDocument32 paginiFinancial Stability and Crises: Microprudential and Macroprudential PolicyАртём ПчелинцевÎncă nu există evaluări

- Revisions Ops Risk 202011 PDFDocument23 paginiRevisions Ops Risk 202011 PDFsh_chandraÎncă nu există evaluări

- 1.RISK CompediumDocument95 pagini1.RISK CompediumyogeshthakkerÎncă nu există evaluări

- Ind L3 Title and Syllabus v1Document4 paginiInd L3 Title and Syllabus v1endro suendroÎncă nu există evaluări

- 12 - Chapter 6 PDFDocument16 pagini12 - Chapter 6 PDFAkhil SablokÎncă nu există evaluări

- 12 - Chapter 6Document16 pagini12 - Chapter 6Akhil SablokÎncă nu există evaluări

- 1031201330300PM Session 1 ICAAP and SREP JustinDocument31 pagini1031201330300PM Session 1 ICAAP and SREP Justinsathya_41095Încă nu există evaluări

- Operational RiskDocument25 paginiOperational RiskAngela ChuaÎncă nu există evaluări

- E 3 21 Key RiskDocument11 paginiE 3 21 Key RiskBang NapiÎncă nu există evaluări

- Bcbcs Standards On IrrbbDocument23 paginiBcbcs Standards On IrrbbMarko SudaÎncă nu există evaluări

- Principles For The Management of Credit RiskDocument10 paginiPrinciples For The Management of Credit RiskYaxye AbdulkariinÎncă nu există evaluări

- Credit Risk ManagementDocument33 paginiCredit Risk ManagementKalidas SundararamanÎncă nu există evaluări

- Key Features of Basel IDocument16 paginiKey Features of Basel IAltaf Hasan KhanÎncă nu există evaluări

- Basel II and Risk MGMTDocument6 paginiBasel II and Risk MGMTSagar ShahÎncă nu există evaluări

- bcbs292 PDFDocument61 paginibcbs292 PDFguindaniÎncă nu există evaluări

- Bcbs 29 ADocument39 paginiBcbs 29 ATapiwa MudzimuregaÎncă nu există evaluări

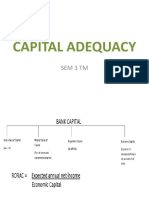

- Capital Adequacy: Sem 3 TMDocument45 paginiCapital Adequacy: Sem 3 TMahsan habibÎncă nu există evaluări

- Bank Risk Management Quang and ChistopherDocument19 paginiBank Risk Management Quang and ChistopherCJÎncă nu există evaluări

- Risk Management & Basel Ii: By: Kajal Gupta Deepanshu Sapra Sanchit BhasinDocument11 paginiRisk Management & Basel Ii: By: Kajal Gupta Deepanshu Sapra Sanchit Bhasinsanchit bhasinÎncă nu există evaluări

- The Critical Challenge Facing Banks and Regulators Under Basel II: Improving Risk Management Through Implementation of Pillar 2Document16 paginiThe Critical Challenge Facing Banks and Regulators Under Basel II: Improving Risk Management Through Implementation of Pillar 2Hassan MphandeÎncă nu există evaluări

- Asset Liability Management in BanksDocument55 paginiAsset Liability Management in BanksHiral Soni100% (1)

- Guidelines ICAAP Guidelines 2012 Updated July 2013Document24 paginiGuidelines ICAAP Guidelines 2012 Updated July 2013Amit DahalÎncă nu există evaluări

- Risk Based SupervisionDocument22 paginiRisk Based Supervisionsakshi819863200Încă nu există evaluări

- Framework: Basle Committee On Banking SupervisionDocument31 paginiFramework: Basle Committee On Banking SupervisionMāhmõūd ĀhmēdÎncă nu există evaluări

- CH 7 Operational Risk and Resiliency AnswersDocument340 paginiCH 7 Operational Risk and Resiliency AnswersTushar Mehndiratta100% (1)

- Operational Risk Management Guidelines RBIDocument65 paginiOperational Risk Management Guidelines RBINirjhar DuttaÎncă nu există evaluări

- RISK-BASED SUPERVISION VS CAMELS RATING SYSTEMDocument2 paginiRISK-BASED SUPERVISION VS CAMELS RATING SYSTEMiyervsr100% (2)

- Final Report - JigarDocument37 paginiFinal Report - Jigarmr.avdheshsharmaÎncă nu există evaluări

- SSM Assetqualityreviewmanual201806 enDocument295 paginiSSM Assetqualityreviewmanual201806 ensubmarinoaguadulceÎncă nu există evaluări

- Best Practie in OpriskDocument23 paginiBest Practie in OpriskThilakPathirageÎncă nu există evaluări

- Risk-based internal audit guidanceDocument7 paginiRisk-based internal audit guidanceMubeen MirzaÎncă nu există evaluări

- Operational Risk MGT TrainingDocument84 paginiOperational Risk MGT TrainingAB Zed100% (1)

- Syllabus Risk Reporting and Analysis (Analisis Dan Pelaporan Risiko) ECAM801251 EVEN SEMESTER 2021/2022 No. LecturerDocument5 paginiSyllabus Risk Reporting and Analysis (Analisis Dan Pelaporan Risiko) ECAM801251 EVEN SEMESTER 2021/2022 No. LecturerAisyah Nadiatul HikmahÎncă nu există evaluări

- Operational Risk ChallengesDocument8 paginiOperational Risk ChallengesKeith WardenÎncă nu există evaluări

- Adobe Scan Oct 24, 2022Document14 paginiAdobe Scan Oct 24, 2022Emmanuel PenullarÎncă nu există evaluări

- Basel II Capital Accord SlidesDocument25 paginiBasel II Capital Accord SlidesAamir RazaÎncă nu există evaluări

- BaselII Opl Risk WPDocument24 paginiBaselII Opl Risk WPmedaniagaÎncă nu există evaluări

- Draft - V3 - Compliance AwarenessDocument15 paginiDraft - V3 - Compliance AwarenessSYED MURTAZAÎncă nu există evaluări

- Operational Risk and Its Impact On The Fund & Investment Management Industry An Insurance PerspectiveDocument20 paginiOperational Risk and Its Impact On The Fund & Investment Management Industry An Insurance PerspectiveAnkita PoteÎncă nu există evaluări

- Yaseen Anwar: Operational Risk Management in Pakistan - Issues and ChallengesDocument4 paginiYaseen Anwar: Operational Risk Management in Pakistan - Issues and Challengesjojee2k6Încă nu există evaluări

- CH 7 Operational Risk and Resiliency WXMNNSNXEODocument178 paginiCH 7 Operational Risk and Resiliency WXMNNSNXEOTushar MehndirattaÎncă nu există evaluări

- Auditing IFRS 9: A Quick Guide To The GPPC's July 2017 PaperDocument7 paginiAuditing IFRS 9: A Quick Guide To The GPPC's July 2017 Papershank nÎncă nu există evaluări

- Risk Management in BankingDocument56 paginiRisk Management in Bankingthulli06Încă nu există evaluări

- Basel III A PrimerDocument28 paginiBasel III A PrimerRajeev Kumar SinghÎncă nu există evaluări

- Spfaib Pbi 1 6 1999Document69 paginiSpfaib Pbi 1 6 1999Djoko NugrohoÎncă nu există evaluări

- 11 4.3 Risk ManagementDocument5 pagini11 4.3 Risk Managementambarish.brbnmplÎncă nu există evaluări

- 4 - Annexure IIDocument14 pagini4 - Annexure IIDeepika KapilÎncă nu există evaluări

- Qust - Ans - Operational and Integrated Risk ManagementDocument348 paginiQust - Ans - Operational and Integrated Risk ManagementBlack MambaÎncă nu există evaluări

- Paper QuilingDocument8 paginiPaper Quilingendro suendroÎncă nu există evaluări

- Hosts UmbrellaDocument1 paginăHosts UmbrellaFabsor SoralÎncă nu există evaluări

- Lampiran ADocument2 paginiLampiran Aendro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document61 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Harga Hair Tonic 20009Document1 paginăHarga Hair Tonic 20009endro suendroÎncă nu există evaluări

- Warranty Card-English, Thai, IndonesianDocument1 paginăWarranty Card-English, Thai, IndonesianRyan SyahMemethÎncă nu există evaluări

- Basic Quilling Instructions: Page 1 of 2: Rolls: ScrollsDocument1 paginăBasic Quilling Instructions: Page 1 of 2: Rolls: Scrollsendro suendroÎncă nu există evaluări

- Lampiran 1 - SE Manajemen Risiko - Pedoman Penerapan - EnglDocument55 paginiLampiran 1 - SE Manajemen Risiko - Pedoman Penerapan - Englendro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document73 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Ind L3 Ch9 v3 - IndonesiaDocument61 paginiInd L3 Ch9 v3 - Indonesiaendro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document89 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document50 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- An Introduction To The Use of Statistics in The Measurement of Financial RiskDocument6 paginiAn Introduction To The Use of Statistics in The Measurement of Financial Riskendro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document61 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document61 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

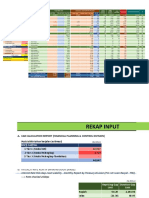

- Capital Allocation Input For 2015 (CNS)Document107 paginiCapital Allocation Input For 2015 (CNS)endro suendroÎncă nu există evaluări

- O15 Prototype Ver 10.03blank - TRSDocument107 paginiO15 Prototype Ver 10.03blank - TRSendro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document50 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document35 paginiIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroÎncă nu există evaluări

- Ind L3 Ch9 v3 - IndonesiaDocument61 paginiInd L3 Ch9 v3 - Indonesiaendro suendroÎncă nu există evaluări

- O15 Prototype Ver 10.03blank - TRSDocument107 paginiO15 Prototype Ver 10.03blank - TRSendro suendroÎncă nu există evaluări

- O15 Prototype Ver 10.03blank - TRSDocument107 paginiO15 Prototype Ver 10.03blank - TRSendro suendroÎncă nu există evaluări

- Ind L3 Title and Syllabus v1Document4 paginiInd L3 Title and Syllabus v1endro suendroÎncă nu există evaluări

- Fire Safety Notification - Karnataka High Court - July 2011Document5 paginiFire Safety Notification - Karnataka High Court - July 2011charu_april100% (1)

- NISM Series IIIA Book SummaryDocument44 paginiNISM Series IIIA Book Summarybhavani sankar areÎncă nu există evaluări

- Russindo HSE Plan and Implementation ScheduleDocument14 paginiRussindo HSE Plan and Implementation ScheduleJusmanizah ZizaÎncă nu există evaluări

- AtionaleDocument7 paginiAtionalearciblueÎncă nu există evaluări

- Code of Commerce Transportation ProvisionsDocument6 paginiCode of Commerce Transportation ProvisionsJon Michael AustriaÎncă nu există evaluări

- Public Procurement Order revised to boost Make in IndiaDocument8 paginiPublic Procurement Order revised to boost Make in IndiaSatheshÎncă nu există evaluări

- Act 231 Highway Authority Malaysia Incorporation Act 1980Document22 paginiAct 231 Highway Authority Malaysia Incorporation Act 1980Adam Haida & CoÎncă nu există evaluări

- Building Permission Guidelines PDFDocument3 paginiBuilding Permission Guidelines PDFramanaidu1Încă nu există evaluări

- Standard Employment ContractDocument6 paginiStandard Employment ContractsaratuuÎncă nu există evaluări

- Disclosure Practices of Banking CompaniesDocument9 paginiDisclosure Practices of Banking CompaniesYashika DamodarÎncă nu există evaluări

- CASH ADVANCES AND REIMBURSEMENTSDocument4 paginiCASH ADVANCES AND REIMBURSEMENTSSuranga Fernando100% (1)

- NB-CPR 15-639r1 Sampling in Systems 1 and 1+ PDFDocument7 paginiNB-CPR 15-639r1 Sampling in Systems 1 and 1+ PDFmingulÎncă nu există evaluări

- U;k;ky; 'kqYd Hkqxrku ds fy, QzSfa dax e'khu izkf/kdj.kDocument11 paginiU;k;ky; 'kqYd Hkqxrku ds fy, QzSfa dax e'khu izkf/kdj.kRajiv ShambhuÎncă nu există evaluări

- 2-Ppt Corporate Governance-Cg DefinitionDocument14 pagini2-Ppt Corporate Governance-Cg DefinitionMahmudur RahmanÎncă nu există evaluări

- Comparision of Condition of ContractDocument23 paginiComparision of Condition of ContractamanuelÎncă nu există evaluări

- Begun and Held in Metro Manila, On Monday, The Twenty-Fourth Day of July, Two Thousand SeventeenDocument15 paginiBegun and Held in Metro Manila, On Monday, The Twenty-Fourth Day of July, Two Thousand SeventeenApril Elenor JucoÎncă nu există evaluări

- Commercial Sand Permit FormDocument5 paginiCommercial Sand Permit FormRonbert Alindogan RamosÎncă nu există evaluări

- Osmania University HYDERABAD - 500 007: Course For The Academic Year 2010-2011. The Inspection Committee Will BeDocument6 paginiOsmania University HYDERABAD - 500 007: Course For The Academic Year 2010-2011. The Inspection Committee Will BepinkpompÎncă nu există evaluări

- Development Agreement 9:18:18Document72 paginiDevelopment Agreement 9:18:18al_crespoÎncă nu există evaluări

- LHD 241 CameDocument17 paginiLHD 241 CameManisha Yuuki100% (1)

- Star Health PolicyDocument5 paginiStar Health PolicyTripathy RadhakrishnaÎncă nu există evaluări

- As 1085.1-2002 Railway Track Material Steel RailsDocument7 paginiAs 1085.1-2002 Railway Track Material Steel RailsSAI Global - APAC100% (1)

- Kik Female Agreement PDFDocument2 paginiKik Female Agreement PDFAnonymous Gn3KWqBzZ9Încă nu există evaluări

- Note On The Asset Management IndustryDocument16 paginiNote On The Asset Management IndustryBenj DanaoÎncă nu există evaluări

- CONTEX CORPORATION, Petitioner, vs. HON. Commissioner OF Internal REVENUE, RespondentDocument36 paginiCONTEX CORPORATION, Petitioner, vs. HON. Commissioner OF Internal REVENUE, RespondentHi Law SchoolÎncă nu există evaluări

- Quality Management Plan-MacksamsDocument12 paginiQuality Management Plan-Macksamssahanun yakubu100% (1)

- Turkish InsuranceDocument5 paginiTurkish InsuranceIqro GlentarÎncă nu există evaluări

- Commutation of PensionDocument4 paginiCommutation of Pensionhimadri_bhattacharjeÎncă nu există evaluări

- ReadingM6 EU and Comparative Company Law Vytautas Magnus University Kaunas 102018Document23 paginiReadingM6 EU and Comparative Company Law Vytautas Magnus University Kaunas 102018Tadas AnužasÎncă nu există evaluări

- ANU MBA CV TemplateDocument2 paginiANU MBA CV TemplateJohn PhÎncă nu există evaluări