S-ar putea să vă placă și

- Chapter 1 PRICING STRATEGY & TACTICSDocument14 paginiChapter 1 PRICING STRATEGY & TACTICSSankary Caroll100% (1)

- Bergerac Systems: The Challenge of Backward IntegrationDocument8 paginiBergerac Systems: The Challenge of Backward IntegrationSujith KumarÎncă nu există evaluări

- Economic Environment Question Paper To Be Sent To SirDocument6 paginiEconomic Environment Question Paper To Be Sent To SirK.N. RajuÎncă nu există evaluări

- I. Macroeconomics and Economic PolicyDocument49 paginiI. Macroeconomics and Economic Policyuntuk sosmedÎncă nu există evaluări

- KawaiDocument29 paginiKawaiMehdi SamÎncă nu există evaluări

- "Billionares": and They Were Not Happy About ItDocument36 pagini"Billionares": and They Were Not Happy About Itkhanriyaz23941560Încă nu există evaluări

- Introduction To Economic Fluctuations: Chapter 10 of Edition, by N. Gregory MankiwDocument27 paginiIntroduction To Economic Fluctuations: Chapter 10 of Edition, by N. Gregory MankiwUsman FaruqueÎncă nu există evaluări

- MacroDocument10 paginiMacrothareendaÎncă nu există evaluări

- Project MaterialDocument26 paginiProject MaterialpinakindpatelÎncă nu există evaluări

- Base Metals - A Global PerspectiveDocument26 paginiBase Metals - A Global Perspectivechandoo.upadhyayÎncă nu există evaluări

- Nikkei Average 1989-2008Document15 paginiNikkei Average 1989-2008api-26172897Încă nu există evaluări

- Fundamental Analysis SeminarDocument51 paginiFundamental Analysis SeminarEugene DalanginÎncă nu există evaluări

- The Economic Foundations of Imperialism: Guglielmo Carchedi and Michael Roberts HM London November 2019Document28 paginiThe Economic Foundations of Imperialism: Guglielmo Carchedi and Michael Roberts HM London November 2019MrWaratahsÎncă nu există evaluări

- Macro Chap1Document32 paginiMacro Chap1alemu ayeneÎncă nu există evaluări

- Great DepressionDocument26 paginiGreat DepressionHoda FakourÎncă nu există evaluări

- Chap 18Document32 paginiChap 18Queen CatastropheÎncă nu există evaluări

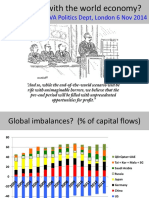

- Schwartz UVa London Alumni (Nov14)Document24 paginiSchwartz UVa London Alumni (Nov14)luigi.pasta5845Încă nu există evaluări

- Mankiw9e Chap01 PDFDocument13 paginiMankiw9e Chap01 PDFCyrus SaadatÎncă nu există evaluări

- 大萧条:历史与经验Document54 pagini大萧条:历史与经验吴宙航Încă nu există evaluări

- The Retail Industry: in Developed Country Three Fourth of The Retail Trade Is Done by Organized SectorDocument28 paginiThe Retail Industry: in Developed Country Three Fourth of The Retail Trade Is Done by Organized SectorThuTaNaingÎncă nu există evaluări

- 06 19 May QA QC ProceduresDocument14 pagini06 19 May QA QC ProceduresMakhfud EdyÎncă nu există evaluări

- The Retail Industry: in Developed Country Three-Fourth of The Retail Trade Is Done by Organized SectorDocument28 paginiThe Retail Industry: in Developed Country Three-Fourth of The Retail Trade Is Done by Organized SectorRohit PrasadÎncă nu există evaluări

- 5 - François Massart, Consultant Pour Les Fonds de Pension SDocument3 pagini5 - François Massart, Consultant Pour Les Fonds de Pension SpensiontalkÎncă nu există evaluări

- U Patnaik What Lies Behind The Food Crisis in India and The Global SouthDocument26 paginiU Patnaik What Lies Behind The Food Crisis in India and The Global SouthAnqur1984Încă nu există evaluări

- Poblacion FuturaDocument2 paginiPoblacion FuturaLisbeth YagualÎncă nu există evaluări

- Sokkelaret 2017 Engelsk PresentasjonDocument25 paginiSokkelaret 2017 Engelsk PresentasjonHải Thân NgọcÎncă nu există evaluări

- Slides1 - The Science of MacroDocument17 paginiSlides1 - The Science of Macroalia trikiÎncă nu există evaluări

- Slides Topic1Document76 paginiSlides Topic1QUYNH NGUYENÎncă nu există evaluări

- ch01 2Document21 paginich01 2Jigar PatelÎncă nu există evaluări

- Ie DataDocument73 paginiIe Datamkkaran90Încă nu există evaluări

- GDP Growth GDP Growth Per Capita Annual %: Assignment 1Document1 paginăGDP Growth GDP Growth Per Capita Annual %: Assignment 1Adnan AqibÎncă nu există evaluări

- Strategies For Writing Overall Trends: Simple Overall Trend DescriptionsDocument5 paginiStrategies For Writing Overall Trends: Simple Overall Trend DescriptionsCat Valentine :vÎncă nu există evaluări

- Brazil Economic ReportDocument217 paginiBrazil Economic Reportaemoraes86Încă nu există evaluări

- 2013 ACP New Panama CanalDocument87 pagini2013 ACP New Panama CanalaimÎncă nu există evaluări

- A Better Investment Climate and Foreign Direct Investment: Uri Dadush, Director, Development Prospects Group andDocument20 paginiA Better Investment Climate and Foreign Direct Investment: Uri Dadush, Director, Development Prospects Group andminhtuanngoÎncă nu există evaluări

- Market AnalysisDocument12 paginiMarket Analysisilasakaa internationalÎncă nu există evaluări

- Group 4Document39 paginiGroup 4Ritika SinghÎncă nu există evaluări

- Value Creation of Leveraged Buyouts in The United KingdomDocument34 paginiValue Creation of Leveraged Buyouts in The United KingdomCanlor LopesÎncă nu există evaluări

- Lecture 3 - Portfolio Theory PDFDocument41 paginiLecture 3 - Portfolio Theory PDFAryan PandeyÎncă nu există evaluări

- Ie DataDocument111 paginiIe Datapraneet singhÎncă nu există evaluări

- Chapter 1 MakroDocument25 paginiChapter 1 MakroAndi Kansha AthayaÎncă nu există evaluări

- The Rate of Profit in Germany 1870-1913: A Reply To Duménil&LévyDocument17 paginiThe Rate of Profit in Germany 1870-1913: A Reply To Duménil&LévyPABLOÎncă nu există evaluări

- Lecture Slides Chap01-1Document27 paginiLecture Slides Chap01-122000492Încă nu există evaluări

- Figure 20.7: Dividend Yields On S& P 500 - 1960 To 1994: Chart1Document11 paginiFigure 20.7: Dividend Yields On S& P 500 - 1960 To 1994: Chart1Jharol CFÎncă nu există evaluări

- Ie DataDocument111 paginiIe DatadtbaseÎncă nu există evaluări

- Price To EarningsDocument111 paginiPrice To EarningsRuhany AragaoÎncă nu există evaluări

- Data Interpretation - 1Document6 paginiData Interpretation - 1Sahil AroraÎncă nu există evaluări

- North South University: Economic Conditions of Bangladesh During 1972-2019Document16 paginiNorth South University: Economic Conditions of Bangladesh During 1972-2019Shoaib AhmedÎncă nu există evaluări

- 1) Stock Market Capitalization As Percent of GDPDocument3 pagini1) Stock Market Capitalization As Percent of GDPprofweb designerÎncă nu există evaluări

- Chapter 17Document23 paginiChapter 17Bhavya SarawgiÎncă nu există evaluări

- Recent Stock Market Developments in The Euro AreaDocument3 paginiRecent Stock Market Developments in The Euro AreaaldhibahÎncă nu există evaluări

- Figure 20.7: Dividend Yields On S& P 500 - 1960 To 1994: Chart1Document11 paginiFigure 20.7: Dividend Yields On S& P 500 - 1960 To 1994: Chart1Ben BieberÎncă nu există evaluări

- IntroDocument29 paginiIntroraymondnaawuÎncă nu există evaluări

- Venture Capital Journal Presentation For Iron Capital PartnersDocument8 paginiVenture Capital Journal Presentation For Iron Capital PartnersVCJournal0% (1)

- CN SSA Boosting Productivity (27 Mar 2017)Document36 paginiCN SSA Boosting Productivity (27 Mar 2017)Chinzara ZivÎncă nu există evaluări

- ITA - Tin Market Outlook James Willoughby June - 22 PDFDocument12 paginiITA - Tin Market Outlook James Willoughby June - 22 PDFRodrigo RodrigoÎncă nu există evaluări

- Manufacturing SectorDocument21 paginiManufacturing SectorVictoria SalazarÎncă nu există evaluări

- Essentially - What Does Concrete Sustainability MeanDocument78 paginiEssentially - What Does Concrete Sustainability MeanLuis Alberto Galvez ParedesÎncă nu există evaluări

- Vidya Mandir Independent Pu College First TestDocument2 paginiVidya Mandir Independent Pu College First TestBlahjÎncă nu există evaluări

- Macroeconomics For ManagersDocument28 paginiMacroeconomics For Managersmajor raveendraÎncă nu există evaluări

- Projection TV Past and Future 2003Document23 paginiProjection TV Past and Future 2003inzanerÎncă nu există evaluări

- Lessons From The Successful InvestorDe la EverandLessons From The Successful InvestorEvaluare: 4.5 din 5 stele4.5/5 (5)

- Asset Rotation: The Demise of Modern Portfolio Theory and the Birth of an Investment RenaissanceDe la EverandAsset Rotation: The Demise of Modern Portfolio Theory and the Birth of an Investment RenaissanceÎncă nu există evaluări

- Total Gadha-Profit and LossDocument14 paginiTotal Gadha-Profit and LossSaket Shahi100% (1)

- Rajagiri College of Management and Applied SciencesDocument39 paginiRajagiri College of Management and Applied SciencesFeny MiriumÎncă nu există evaluări

- 2019 Peterborough Housing Is Fundamental ReportDocument7 pagini2019 Peterborough Housing Is Fundamental ReportPeterborough ExaminerÎncă nu există evaluări

- PurchasingDocument48 paginiPurchasingBinu100% (2)

- Fashion Accessory Cost ComponentsDocument21 paginiFashion Accessory Cost ComponentsKim Laurence Mejia ReyesÎncă nu există evaluări

- Weighted Average Cost of Capital (WACC) GuideDocument5 paginiWeighted Average Cost of Capital (WACC) GuideJahangir KhanÎncă nu există evaluări

- Jose Antonio Herrero, Analysis of LMM Airport PrivatizationDocument22 paginiJose Antonio Herrero, Analysis of LMM Airport PrivatizationdarwinbondgrahamÎncă nu există evaluări

- Statement Dec 2011Document2 paginiStatement Dec 2011Iris KhanashatÎncă nu există evaluări

- Robi Axiata Limited: (As Per Prospectus)Document1 paginăRobi Axiata Limited: (As Per Prospectus)রাফসান হোসেন রাব্বীÎncă nu există evaluări

- Group Assignment. Business MathematicsDocument2 paginiGroup Assignment. Business MathematicsEricKHLeaw100% (1)

- "Fundamental Analysis of Script Under Pharmaceutical Sector"Document82 pagini"Fundamental Analysis of Script Under Pharmaceutical Sector"sg31Încă nu există evaluări

- Managerial Economics & Financial AnalysisDocument21 paginiManagerial Economics & Financial AnalysisVanukuri Gopi ReddyÎncă nu există evaluări

- SuzlonDocument23 paginiSuzlonPuneet GuptaÎncă nu există evaluări

- Chapter 20 - VATDocument14 paginiChapter 20 - VATrottelosÎncă nu există evaluări

- 4 2006 Dec QDocument9 pagini4 2006 Dec Qapi-19836745Încă nu există evaluări

- 3.1 Quantitative Skills Practice QuestionsDocument3 pagini3.1 Quantitative Skills Practice QuestionsRayan SibariÎncă nu există evaluări

- CMI ManagementDirect - BudgetsDocument34 paginiCMI ManagementDirect - BudgetsAnonymous 2AK0KTÎncă nu există evaluări

- CH 07Document4 paginiCH 07Gus JooÎncă nu există evaluări

- Are You About Starting A Car Rental BusinessDocument18 paginiAre You About Starting A Car Rental BusinessSebastian Kabui100% (2)

- Ayana Proposal 1 TOURISM INVESTMENTDocument25 paginiAyana Proposal 1 TOURISM INVESTMENTvillaarbaminch67% (6)

- FIN5203 Midterm Exam 2 FL22 ReviewDocument46 paginiFIN5203 Midterm Exam 2 FL22 Reviewmerly chermonÎncă nu există evaluări

- Airtel Generic StrategiesDocument18 paginiAirtel Generic StrategiesRakesh Skai0% (1)

- Osn Contract 2012 Edition WebDocument34 paginiOsn Contract 2012 Edition WebWon JangÎncă nu există evaluări

- TR39 Volume VDocument221 paginiTR39 Volume VRamphani NunnaÎncă nu există evaluări

- Asian Paints PDFDocument36 paginiAsian Paints PDFPreeti AroraÎncă nu există evaluări

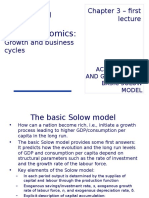

- Introducing Advanced Macroeconomics:: Chapter 3 - FirstDocument23 paginiIntroducing Advanced Macroeconomics:: Chapter 3 - Firstblah blahÎncă nu există evaluări

- Auto Insurance Database Report 2013/2014: January 2017Document254 paginiAuto Insurance Database Report 2013/2014: January 2017ravikumarÎncă nu există evaluări