S-ar putea să vă placă și

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Income Tax Case Digest 1. Madrigal v. Rafferty 38 Phil 14 G.R. No. 12287 (1918) Malcolm, JDocument17 paginiIncome Tax Case Digest 1. Madrigal v. Rafferty 38 Phil 14 G.R. No. 12287 (1918) Malcolm, JKarl Marxcuz Reyes100% (1)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Electricity Act and Regulatory FrameDocument75 paginiElectricity Act and Regulatory Frameucb2_ntpcÎncă nu există evaluări

- Model Bills of Quantities - 2005Document387 paginiModel Bills of Quantities - 2005mutuli33% (3)

- Vertex Indirect Tax Accelerator For SAP ERP Implementation GuideDocument53 paginiVertex Indirect Tax Accelerator For SAP ERP Implementation GuideCA Sakshi Goyal75% (4)

- Request For Quotation (RFQ) : Requester Information Tanggal RFQ Batas RFQDocument7 paginiRequest For Quotation (RFQ) : Requester Information Tanggal RFQ Batas RFQAditya KurniawanÎncă nu există evaluări

- DOE/Taguchi ANOVA S/N Ratio Dynamic Characteristics: Plan Experiment/BrainstormDocument4 paginiDOE/Taguchi ANOVA S/N Ratio Dynamic Characteristics: Plan Experiment/Brainstormucb2_ntpcÎncă nu există evaluări

- Busbar ProtectionDocument4 paginiBusbar Protectionucb2_ntpcÎncă nu există evaluări

- Title R.A. 7432 R.A. 9257 R.A. 9994 - ExpandedDocument11 paginiTitle R.A. 7432 R.A. 9257 R.A. 9994 - ExpandedAngel Alejo AcobaÎncă nu există evaluări

- International Business - Pulses Export BPLAN PDFDocument30 paginiInternational Business - Pulses Export BPLAN PDFSangram Jagtap100% (1)

- Open Vs Closed Impeller PDFDocument3 paginiOpen Vs Closed Impeller PDFucb2_ntpcÎncă nu există evaluări

- Final Black BookDocument77 paginiFinal Black BookAnkush UpadhyayÎncă nu există evaluări

- Thyrister DetailsDocument1 paginăThyrister Detailsucb2_ntpcÎncă nu există evaluări

- Harvard Managementor Course Schedule For One Year 2017-18: Level Level MonthDocument1 paginăHarvard Managementor Course Schedule For One Year 2017-18: Level Level Monthucb2_ntpcÎncă nu există evaluări

- SL - No Power Cable Jointing Required/ No As Joints Cable Size 185 SQMM Megger ValveDocument1 paginăSL - No Power Cable Jointing Required/ No As Joints Cable Size 185 SQMM Megger Valveucb2_ntpcÎncă nu există evaluări

- Auto SamplerDocument25 paginiAuto Samplerucb2_ntpcÎncă nu există evaluări

- Honeywell Sensing Position Rangeguide 000709 25 en LowresDocument22 paginiHoneywell Sensing Position Rangeguide 000709 25 en Lowresucb2_ntpcÎncă nu există evaluări

- NonAlignment 2Document7 paginiNonAlignment 2ucb2_ntpcÎncă nu există evaluări

- Emp ListDocument2 paginiEmp Listucb2_ntpcÎncă nu există evaluări

- E Governance 3Document12 paginiE Governance 3ucb2_ntpcÎncă nu există evaluări

- Opinion Polls, Exit Polls and Early Seat Projections: Rajeeva L. KarandikarDocument55 paginiOpinion Polls, Exit Polls and Early Seat Projections: Rajeeva L. Karandikarucb2_ntpcÎncă nu există evaluări

- Excitation CIGREA1 10Document6 paginiExcitation CIGREA1 10ucb2_ntpcÎncă nu există evaluări

- VAT and LOCAL TAXDocument4 paginiVAT and LOCAL TAXUbalda AbuboÎncă nu există evaluări

- Document 2188096 P2PDocument3 paginiDocument 2188096 P2Pmandarjejurikar100% (1)

- SBD 6 2 Local Content FormDocument5 paginiSBD 6 2 Local Content FormVictorÎncă nu există evaluări

- Painting ContractDocument22 paginiPainting Contractagrvinit123Încă nu există evaluări

- Annexures BelDocument5 paginiAnnexures BelManikantavarma MahaliÎncă nu există evaluări

- R12-Tables and ViewsDocument29 paginiR12-Tables and ViewsshikhaÎncă nu există evaluări

- SITXGLC001 Student TemplateDocument68 paginiSITXGLC001 Student TemplateMary Flor Agbayani KyosangshinÎncă nu există evaluări

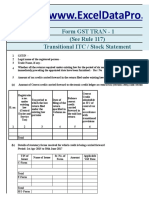

- GST TRAN 1 Return Excel TemplateDocument14 paginiGST TRAN 1 Return Excel TemplateRaju Ranjan KumarÎncă nu există evaluări

- RR 2018 PDFDocument242 paginiRR 2018 PDFJill b.Încă nu există evaluări

- Excel FormulaeDocument205 paginiExcel Formulaek_naseergÎncă nu există evaluări

- Ramiz Report PDFDocument39 paginiRamiz Report PDFMohammad Ramiz ShaikhÎncă nu există evaluări

- Invoice: Invoice Address Delivery AddressDocument5 paginiInvoice: Invoice Address Delivery AddressOnkar PotdarÎncă nu există evaluări

- Gen Principles DigestDocument12 paginiGen Principles DigestCzarina Joy PenaÎncă nu există evaluări

- Information For Items 21 & 22Document3 paginiInformation For Items 21 & 22Kurt Morin CantorÎncă nu există evaluări

- Analisa BEADocument20 paginiAnalisa BEATest AccountÎncă nu există evaluări

- Current - Liabilities - PPTX Filename UTF-8''Current LiabilitiesDocument44 paginiCurrent - Liabilities - PPTX Filename UTF-8''Current LiabilitieskristineÎncă nu există evaluări

- MKMS ManualDocument284 paginiMKMS ManualferratejÎncă nu există evaluări

- Government Gazette ZA Vol 672 No 44659 Legal Notices B Dated 2021-06-04Document160 paginiGovernment Gazette ZA Vol 672 No 44659 Legal Notices B Dated 2021-06-04simphiweÎncă nu există evaluări

- Dextra Court Water Bill For VIVID PDFDocument58 paginiDextra Court Water Bill For VIVID PDFseharÎncă nu există evaluări

- Einvoce - Gepp User ManualDocument29 paginiEinvoce - Gepp User ManualDadang TirthaÎncă nu există evaluări

- Goods & Services Act FinalDocument78 paginiGoods & Services Act FinalParvesh AghiÎncă nu există evaluări

- Impact On IT Sector Related To BudgetDocument2 paginiImpact On IT Sector Related To BudgetAmruta SawantÎncă nu există evaluări

- ReportDocument74 paginiReportar15t0tleÎncă nu există evaluări