S-ar putea să vă placă și

- Revised PAS 19Document2 paginiRevised PAS 19jjmcjjmc12345Încă nu există evaluări

- Ifrs 7Document5 paginiIfrs 7alkhaqiÎncă nu există evaluări

- Copy Individual Income TaxDocument10 paginiCopy Individual Income TaxMari Louis Noriell MejiaÎncă nu există evaluări

- Order To CashDocument3 paginiOrder To CashPrashanth ChidambaramÎncă nu există evaluări

- Short-Term Finance and PlanningDocument27 paginiShort-Term Finance and PlanningMiftahul Agusta100% (1)

- Income Tax Guide UgandaDocument13 paginiIncome Tax Guide UgandaMoses LubangakeneÎncă nu există evaluări

- C1Document19 paginiC1Analys JulianÎncă nu există evaluări

- Mas Test Bank SolutionDocument14 paginiMas Test Bank SolutionLyzaÎncă nu există evaluări

- Overview of Financial ManagementDocument187 paginiOverview of Financial ManagementashrawÎncă nu există evaluări

- Ias-40 - Investment PropertyDocument16 paginiIas-40 - Investment PropertyPue Das100% (2)

- Advance Chapter 1Document16 paginiAdvance Chapter 1abel habtamuÎncă nu există evaluări

- Ias 20 Accounting For Government Grants and Disclosure of Government Assistance SummaryDocument5 paginiIas 20 Accounting For Government Grants and Disclosure of Government Assistance SummaryKenncyÎncă nu există evaluări

- Chapter-Six Accounting For General, Special Revenue and Capital Project FundsDocument31 paginiChapter-Six Accounting For General, Special Revenue and Capital Project FundsMany Girma100% (1)

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument38 paginiPrepared by Coby Harmon University of California, Santa Barbara Westmont Collegee s tÎncă nu există evaluări

- Module 1B - PFRS For Medium Entities NotesDocument25 paginiModule 1B - PFRS For Medium Entities NotesLee SuarezÎncă nu există evaluări

- Insurance Contracts ExplainedDocument32 paginiInsurance Contracts ExplainedWingFatt KhooÎncă nu există evaluări

- Provide A Summary of Understanding of The Following For The Leasing IndustryDocument5 paginiProvide A Summary of Understanding of The Following For The Leasing IndustryMarielle P. GarciaÎncă nu există evaluări

- Chapter Three: Valuation of Financial Instruments & Cost of CapitalDocument68 paginiChapter Three: Valuation of Financial Instruments & Cost of CapitalAbrahamÎncă nu există evaluări

- Chapter 4 Joint Arrengement and Public SectorDocument58 paginiChapter 4 Joint Arrengement and Public SectorLakachew Getasew100% (2)

- Module IV: MUS Sampling - Factory Equipment Additions: RequirementsDocument2 paginiModule IV: MUS Sampling - Factory Equipment Additions: RequirementsMukh UbaidillahÎncă nu există evaluări

- Role of Auditor With-In A Company: AuditDocument6 paginiRole of Auditor With-In A Company: AuditUniq ManjuÎncă nu există evaluări

- Consolidated Financial Statements ExplainedDocument77 paginiConsolidated Financial Statements ExplainedMisganaw DebasÎncă nu există evaluări

- An Independent Correspondent Member ofDocument10 paginiAn Independent Correspondent Member ofRizwanChowdhury100% (1)

- Introduction To Business CombinationDocument15 paginiIntroduction To Business CombinationDELFIN, LORENA D.Încă nu există evaluări

- Ifrs 5 Assets Held For Sale and Discontinued OperationsDocument45 paginiIfrs 5 Assets Held For Sale and Discontinued OperationstinashekuzangaÎncă nu există evaluări

- Revenue From Contracts With Customers at or Before The Date: Reasons For Issuing IFRS 16Document15 paginiRevenue From Contracts With Customers at or Before The Date: Reasons For Issuing IFRS 16omoyegunÎncă nu există evaluări

- Calculating Depreciation and Average Rate of Return for Equipment InvestmentDocument9 paginiCalculating Depreciation and Average Rate of Return for Equipment Investmentpeter mulilaÎncă nu există evaluări

- IFRS 10 Consolidation RRDocument43 paginiIFRS 10 Consolidation RRYared HussenÎncă nu există evaluări

- PUBLIC FINANCE AND TAXATION- BCOM ACC, FIN & BBADocument13 paginiPUBLIC FINANCE AND TAXATION- BCOM ACC, FIN & BBAMaster KihimbwaÎncă nu există evaluări

- Profit and Loss AccountDocument15 paginiProfit and Loss AccountLogesh Waran100% (1)

- Share-Based Compensation: Learning ObjectivesDocument48 paginiShare-Based Compensation: Learning ObjectivesJola MairaloÎncă nu există evaluări

- Limited Liability Company and S Corporation Business Form ComparisonDocument6 paginiLimited Liability Company and S Corporation Business Form ComparisonpukeaÎncă nu există evaluări

- Isre 2400Document21 paginiIsre 2400naveedawan321Încă nu există evaluări

- Introduction To Taxation: (Taxes, Tax Laws and Tax Administration) by Daryl T. Evardone, CPADocument35 paginiIntroduction To Taxation: (Taxes, Tax Laws and Tax Administration) by Daryl T. Evardone, CPAKyla Marie HubieraÎncă nu există evaluări

- Case 2Document4 paginiCase 2Chris WongÎncă nu există evaluări

- ISA - 315 Understanding The Entity & Its Environment & Assessing The Risks of Material MisstatementDocument13 paginiISA - 315 Understanding The Entity & Its Environment & Assessing The Risks of Material MisstatementsajedulÎncă nu există evaluări

- Basic Parts of An Insurance ContractDocument9 paginiBasic Parts of An Insurance Contractpankajgupta100% (4)

- Accounting For PartnershipDocument3 paginiAccounting For PartnershipafifahÎncă nu există evaluări

- BUSE Company Law Notes 1Document111 paginiBUSE Company Law Notes 1Phebieon Mukwenha100% (1)

- Financial Accounting: Weygandt KimmelDocument47 paginiFinancial Accounting: Weygandt KimmelTham NguyenÎncă nu există evaluări

- Pas 20, 23Document32 paginiPas 20, 23Angela WaganÎncă nu există evaluări

- Risk Management Process and TechniquesDocument27 paginiRisk Management Process and TechniquesWonde BiruÎncă nu există evaluări

- Accounting For Leases: Deegan, Financial Accounting, 8eDocument54 paginiAccounting For Leases: Deegan, Financial Accounting, 8eErlanÎncă nu există evaluări

- FM CH 1natureoffinancialmanagement 120704104928 Phpapp01 PDFDocument28 paginiFM CH 1natureoffinancialmanagement 120704104928 Phpapp01 PDFvasantharao100% (1)

- Galvor Company Case: Group 1Document10 paginiGalvor Company Case: Group 1asramasaja100% (1)

- Calculate Terminal Cash FlowDocument9 paginiCalculate Terminal Cash FlowKazzandraEngallaPaduaÎncă nu există evaluări

- Chapter 4Document30 paginiChapter 4Siti AishahÎncă nu există evaluări

- Property, Plant and Equipment: By:-Yohannes Negatu (Acca, Dipifr)Document37 paginiProperty, Plant and Equipment: By:-Yohannes Negatu (Acca, Dipifr)Eshetie Mekonene AmareÎncă nu există evaluări

- IFRS 4 Insurance ContractsDocument5 paginiIFRS 4 Insurance Contractstikki0219Încă nu există evaluări

- Code of Ethics for CPAs in the PhilippinesDocument24 paginiCode of Ethics for CPAs in the PhilippinesQueenie QuisidoÎncă nu există evaluări

- Earned leave rules for government servantsDocument6 paginiEarned leave rules for government servantsm a zubairÎncă nu există evaluări

- Capital Structure PlanningDocument25 paginiCapital Structure PlanningSumit MahajanÎncă nu există evaluări

- Ch.2 PGDocument12 paginiCh.2 PGkasimÎncă nu există evaluări

- ACC205 Seminar 2 StudentDocument35 paginiACC205 Seminar 2 StudentDa Na ChngÎncă nu există evaluări

- 2.1. Property Plant and Equipment IAS 16Document7 pagini2.1. Property Plant and Equipment IAS 16Priya Satheesh100% (1)

- Financial Feasibility Study ChaptersDocument52 paginiFinancial Feasibility Study ChaptersDing RarugalÎncă nu există evaluări

- Ias 19-Employee BenefitsDocument3 paginiIas 19-Employee Benefitsbeth alviolaÎncă nu există evaluări

- SBR - Chapter 5Document6 paginiSBR - Chapter 5Jason KumarÎncă nu există evaluări

- Ias 19 Employee BenefitsDocument43 paginiIas 19 Employee BenefitsHasan Ali BokhariÎncă nu există evaluări

- Employee Benefits AccountingDocument18 paginiEmployee Benefits AccountingDesiree GalletoÎncă nu există evaluări

- Working Capital ManagementDocument16 paginiWorking Capital ManagementjcshahÎncă nu există evaluări

- Managerial AccountingMid Term Examination (1) - CONSULTADocument7 paginiManagerial AccountingMid Term Examination (1) - CONSULTAMay Ramos100% (1)

- IIMMDocument24 paginiIIMMarun1974Încă nu există evaluări

- ARTO Bank Report: Development, Shareholders, DividendsDocument3 paginiARTO Bank Report: Development, Shareholders, DividendsAfterneathÎncă nu există evaluări

- PayslipDocument1 paginăPayslipChristine Aev OlasaÎncă nu există evaluări

- Group Assignment - Questions - RevisedDocument6 paginiGroup Assignment - Questions - Revised31231023949Încă nu există evaluări

- WhiteMonk HEG Equity Research ReportDocument15 paginiWhiteMonk HEG Equity Research ReportGirish Ramachandra100% (1)

- Financial ManagementDocument254 paginiFinancial Managementkimringine50% (2)

- CFO Guide to Debt Management and Treasury FunctionsDocument6 paginiCFO Guide to Debt Management and Treasury FunctionsRobinson MojicaÎncă nu există evaluări

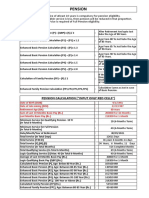

- Pension and Other Retirement BenifitsDocument8 paginiPension and Other Retirement BenifitsVikas GuptaÎncă nu există evaluări

- 03 MA2 LRP AnswersDocument34 pagini03 MA2 LRP AnswersKopanang LeokanaÎncă nu există evaluări

- CH 09 SMDocument54 paginiCH 09 SMapi-234680678100% (2)

- Chapter 3 Predetermined OvDocument98 paginiChapter 3 Predetermined OvErin CruzÎncă nu există evaluări

- Buying and Selling: and Net Profit/LossDocument19 paginiBuying and Selling: and Net Profit/LossMarc Graham NacuaÎncă nu există evaluări

- Fundamental Equity Analysis - QMS Advisors HDAX FlexIndex 110Document227 paginiFundamental Equity Analysis - QMS Advisors HDAX FlexIndex 110Q.M.S Advisors LLCÎncă nu există evaluări

- Cash Discount: What Is A Cash Discount? Definition of Cash DiscountDocument12 paginiCash Discount: What Is A Cash Discount? Definition of Cash DiscountHumanityÎncă nu există evaluări

- Petty Cash Policy GuideDocument3 paginiPetty Cash Policy GuideHimanshijain100% (3)

- A Project On Analysis of Ulips in IndiaDocument78 paginiA Project On Analysis of Ulips in IndiaNadeem NadduÎncă nu există evaluări

- Course Folder Fall 2022Document26 paginiCourse Folder Fall 2022Areeba QureshiÎncă nu există evaluări

- Mock-2, Sec-ADocument19 paginiMock-2, Sec-AmmranaduÎncă nu există evaluări

- Corporate Governance IntroductionDocument34 paginiCorporate Governance IntroductionIndira Thayil100% (2)

- Accounting Equation and Effects of Business TransactionsDocument13 paginiAccounting Equation and Effects of Business TransactionsHà My NguyễnÎncă nu există evaluări

- CH 14Document77 paginiCH 14hartinahÎncă nu există evaluări

- Accounting For The IphoneDocument9 paginiAccounting For The IphoneFatihahZainalLim100% (1)

- Section - A: Statutory Update: Part - I: Direct Tax LawsDocument47 paginiSection - A: Statutory Update: Part - I: Direct Tax LawsmdfkjadsjkÎncă nu există evaluări

- Your College Budget AssignmentDocument8 paginiYour College Budget Assignmentlatorrem6457100% (1)

- PRS Econ CH13 9eDocument40 paginiPRS Econ CH13 9eDamla HacıÎncă nu există evaluări

- Chapter-2 - Dividend DecisionsDocument54 paginiChapter-2 - Dividend DecisionsRaunak YadavÎncă nu există evaluări

- Chapter Five: The Financial Statements of Banks and Their Principal CompetitorsDocument35 paginiChapter Five: The Financial Statements of Banks and Their Principal Competitorsعبدالله ماجد المطارنه100% (1)

- Current liability problems and solutionsDocument5 paginiCurrent liability problems and solutionsNoSepasi FebriyaniÎncă nu există evaluări