S-ar putea să vă placă și

- Lesson 8 BtaxDocument4 paginiLesson 8 Btaxdin matanguihanÎncă nu există evaluări

- Tax 2 Sec 113Document2 paginiTax 2 Sec 113Aron LoboÎncă nu există evaluări

- Intel Technology Philippines, Inc. vs. CommissionerDocument30 paginiIntel Technology Philippines, Inc. vs. Commissionervince005Încă nu există evaluări

- Draft RR Registration EOPT - For Public ConsultationDocument18 paginiDraft RR Registration EOPT - For Public ConsultationGennelyn OdulioÎncă nu există evaluări

- Kepco v. CIRDocument2 paginiKepco v. CIRDhan SamsonÎncă nu există evaluări

- AT&T Communications Services Phils. Inc. v. CIRDocument8 paginiAT&T Communications Services Phils. Inc. v. CIRAnonymous 8liWSgmIÎncă nu există evaluări

- Authoritative Guide On Real Estate Transfer TaxesDocument37 paginiAuthoritative Guide On Real Estate Transfer TaxesJames ReyesÎncă nu există evaluări

- Intel Technology Phils. Inc. vs. CIR GR No. 166732 - April 27, 2007 FactsDocument5 paginiIntel Technology Phils. Inc. vs. CIR GR No. 166732 - April 27, 2007 FactsCHow GatchallanÎncă nu există evaluări

- Revenue Regulations No. 16-05Document6 paginiRevenue Regulations No. 16-05Danzki BadiqueÎncă nu există evaluări

- Kepco vs. CirDocument2 paginiKepco vs. CirCaroline A. LegaspinoÎncă nu există evaluări

- Tax DigestDocument11 paginiTax DigestSarah Jane Fabricante BehigaÎncă nu există evaluări

- P&G Vs CIR - Vat RulingDocument7 paginiP&G Vs CIR - Vat Rulingcaren kay b. adolfoÎncă nu există evaluări

- Eatern Telecom v. CIR DigestDocument4 paginiEatern Telecom v. CIR DigestKristineSherikaChyÎncă nu există evaluări

- AT - T COMMUNICATIONS SERVICES PHILIPPINES, INC., Vs CIR G.R. No. 182364 August 3, 2010Document4 paginiAT - T COMMUNICATIONS SERVICES PHILIPPINES, INC., Vs CIR G.R. No. 182364 August 3, 2010Francise Mae Montilla MordenoÎncă nu există evaluări

- This Study Resource Was: January 31, 2011.)Document4 paginiThis Study Resource Was: January 31, 2011.)Josephine CastilloÎncă nu există evaluări

- SILICON PHILIPPINES, INC., (Formerly INTEL PHILIPPINES MANUFACTURING, INC.) vs. COMMISSIONER OF INTERNAL REVENUEDocument4 paginiSILICON PHILIPPINES, INC., (Formerly INTEL PHILIPPINES MANUFACTURING, INC.) vs. COMMISSIONER OF INTERNAL REVENUETrishaÎncă nu există evaluări

- Rmo 3-2009Document29 paginiRmo 3-2009sheena100% (2)

- 43677RMO 3-2009 - Suspension GroundsDocument29 pagini43677RMO 3-2009 - Suspension GroundsAnonymous OyhbxcjÎncă nu există evaluări

- Kepco v. CIRDocument4 paginiKepco v. CIRWhere Did Macky GallegoÎncă nu există evaluări

- Kepco V Cir (2010)Document2 paginiKepco V Cir (2010)Agatha Bernice MacalaladÎncă nu există evaluări

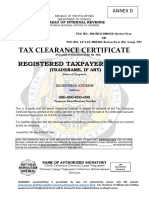

- Annex DDocument1 paginăAnnex DIdan Aguirre67% (3)

- Advisory - ARF (Annual Reg Fee) 2024 - DigestDocument4 paginiAdvisory - ARF (Annual Reg Fee) 2024 - DigestpelgonehÎncă nu există evaluări

- Tambunting v. CIRDocument4 paginiTambunting v. CIRlouis jansenÎncă nu există evaluări

- Value Added TaxDocument2 paginiValue Added TaxBon BonsÎncă nu există evaluări

- Eastern Telecommunications Philippines v. CIRDocument1 paginăEastern Telecommunications Philippines v. CIRMarcella Maria KaraanÎncă nu există evaluări

- BIR Ruling 133-13Document2 paginiBIR Ruling 133-13Kyra DiolaÎncă nu există evaluări

- TAX-1402 (Compliance Requirements)Document2 paginiTAX-1402 (Compliance Requirements)Hilo MethodÎncă nu există evaluări

- Petitioner Vs Vs Respondent: Second DivisionDocument5 paginiPetitioner Vs Vs Respondent: Second DivisionCamshtÎncă nu există evaluări

- TAX-304 (VAT Compliance Requirements)Document5 paginiTAX-304 (VAT Compliance Requirements)Edith DalidaÎncă nu există evaluări

- Microsoft Philippines V CIR-fullDocument3 paginiMicrosoft Philippines V CIR-fullLucky JavellanaÎncă nu există evaluări

- Vat DigestsDocument10 paginiVat DigestsTrishaÎncă nu există evaluări

- CIR vs. Manila Mining CorporationDocument25 paginiCIR vs. Manila Mining CorporationAronJamesÎncă nu există evaluări

- BIR Form 2550M - Monthly Value-Added Tax Declaration Guidelines and InstructionsDocument1 paginăBIR Form 2550M - Monthly Value-Added Tax Declaration Guidelines and InstructionsdreaÎncă nu există evaluări

- BIR Form 2550M - Monthly Value-Added Tax Declaration Guidelines and InstructionsDocument1 paginăBIR Form 2550M - Monthly Value-Added Tax Declaration Guidelines and InstructionsdreaÎncă nu există evaluări

- Eastern Telecommunications PhilippinesDocument3 paginiEastern Telecommunications PhilippinesTheodore0176Încă nu există evaluări

- Capital Gains TaxDocument3 paginiCapital Gains TaxAJ Santos100% (2)

- Silicon Philippines v. CIR: DOCTRINE/S: All Told, The NonDocument3 paginiSilicon Philippines v. CIR: DOCTRINE/S: All Told, The NonDaLe AparejadoÎncă nu există evaluări

- Compliance Requirements SEC. 113. Invoicing and Accounting Requirements For VAT-Registered Persons.Document4 paginiCompliance Requirements SEC. 113. Invoicing and Accounting Requirements For VAT-Registered Persons.shakiraÎncă nu există evaluări

- Chapter 22Document25 paginiChapter 22Rachel Pepito BaladjayÎncă nu există evaluări

- CIR Vs Manila Mining CorpDocument27 paginiCIR Vs Manila Mining CorpJessÎncă nu există evaluări

- H. Tambunting Pawnshop, Inc. vs. CIRDocument15 paginiH. Tambunting Pawnshop, Inc. vs. CIRPhulagyn CañedoÎncă nu există evaluări

- 2550Q InstructionsDocument1 pagină2550Q InstructionsMay RamosÎncă nu există evaluări

- Republic of Philippines Court of Tax Appeals Quezon Second DivisionDocument26 paginiRepublic of Philippines Court of Tax Appeals Quezon Second DivisionKimberly MayÎncă nu există evaluări

- Administrative Provisions TRAIN LAWDocument5 paginiAdministrative Provisions TRAIN LAWKuhe DelosÎncă nu există evaluări

- STATCON - JRA Phils vs. CIRDocument3 paginiSTATCON - JRA Phils vs. CIRdianne rebutarÎncă nu există evaluări

- Business-Tax VAT FAQsDocument11 paginiBusiness-Tax VAT FAQsBryan VidalÎncă nu există evaluări

- VAT, Other Percentage Tax, Excise Tax and Documentary Stamp TaxDocument5 paginiVAT, Other Percentage Tax, Excise Tax and Documentary Stamp TaxJune Romeo ObiasÎncă nu există evaluări

- RR 16-2005Document9 paginiRR 16-2005mblopez1Încă nu există evaluări

- BarterDocument2 paginiBarterRester NonatoÎncă nu există evaluări

- 2000-OT June 2006 (Back)Document1 pagină2000-OT June 2006 (Back)Jeric BlasurcaÎncă nu există evaluări

- Zero-Rated SalesDocument3 paginiZero-Rated SalesAlvin Lozares CasajeÎncă nu există evaluări

- JRA Philippines v. CIRDocument8 paginiJRA Philippines v. CIRCuayo JuicoÎncă nu există evaluări

- San Roque Vs CirDocument28 paginiSan Roque Vs CirJAMÎncă nu există evaluări

- Tax BarqsDocument6 paginiTax BarqsGiee De GuzmanÎncă nu există evaluări

- Western Mindanao Power Corporation V CIRDocument4 paginiWestern Mindanao Power Corporation V CIRTintin CoÎncă nu există evaluări

- 2015 11 01 VAT Guidance On Invoices Sales Receipts Credit Notes and Debit NotesDocument26 pagini2015 11 01 VAT Guidance On Invoices Sales Receipts Credit Notes and Debit NotesRoseÎncă nu există evaluări

- Guidelines and Instructions For BIR Form No. 1707-A Annual Capital Gains Tax ReturnDocument1 paginăGuidelines and Instructions For BIR Form No. 1707-A Annual Capital Gains Tax ReturnKylie sheena MendezÎncă nu există evaluări

- 10 Silicon Philippines Inc. v. CIRDocument20 pagini10 Silicon Philippines Inc. v. CIRAnonymous 8liWSgmIÎncă nu există evaluări

- BIR Form 1707Document3 paginiBIR Form 1707catherine joy sangilÎncă nu există evaluări

- Crypto Taxation in USA: A Comprehensive Guide to Navigating Digital Assets and TaxationDe la EverandCrypto Taxation in USA: A Comprehensive Guide to Navigating Digital Assets and TaxationÎncă nu există evaluări

- TAX RefundDocument6 paginiTAX RefundRoselyn NaronÎncă nu există evaluări

- Saudia vs. Rebesencio Case DigestDocument2 paginiSaudia vs. Rebesencio Case DigestRoselyn Naron100% (2)

- Frivaldo v. Comelec 257 SCRA 727 (1996) Final DigestDocument2 paginiFrivaldo v. Comelec 257 SCRA 727 (1996) Final DigestRoselyn NaronÎncă nu există evaluări

- Oposa vs. Factoran - DigestDocument2 paginiOposa vs. Factoran - DigestRoselyn NaronÎncă nu există evaluări

- Legaspi v. CSC G.R. No. L-72119, 29 May 1987 - Digest - FinalDocument1 paginăLegaspi v. CSC G.R. No. L-72119, 29 May 1987 - Digest - FinalRoselyn Naron100% (1)

- Legaspi vs. Ministry of Finance DigestDocument2 paginiLegaspi vs. Ministry of Finance DigestRoselyn NaronÎncă nu există evaluări

- SAGUISAG V. OCHOA, GR. 212426, 1.12.16v2Document5 paginiSAGUISAG V. OCHOA, GR. 212426, 1.12.16v2Roselyn NaronÎncă nu există evaluări

- Saudia v. Rebesencio, Gr.198587, Jan 14, 2015Document2 paginiSaudia v. Rebesencio, Gr.198587, Jan 14, 2015Roselyn NaronÎncă nu există evaluări

- Vda. de Ape v. CADocument2 paginiVda. de Ape v. CAJustineÎncă nu există evaluări

- Final Report FiberGlass FansDocument52 paginiFinal Report FiberGlass FansRaza AliÎncă nu există evaluări

- Chap 2 Basic Cost Management Concepts and Accounting For Mass Customization OperationsDocument15 paginiChap 2 Basic Cost Management Concepts and Accounting For Mass Customization OperationsMarklorenz SumpayÎncă nu există evaluări

- Service MarketingDocument34 paginiService Marketingnisha100% (3)

- Porters Five Force ModelDocument4 paginiPorters Five Force Modelnaveen sunguluru50% (2)

- Industrial FormDocument3 paginiIndustrial FormMasood Alam FarooquiÎncă nu există evaluări

- KSC 3 CHDocument82 paginiKSC 3 CHchaitradeepÎncă nu există evaluări

- Module 8 - Inventories Part IIDocument14 paginiModule 8 - Inventories Part IIMark Christian BrlÎncă nu există evaluări

- Revenue Recognition - IFRS 15Document15 paginiRevenue Recognition - IFRS 15techna8Încă nu există evaluări

- Supply Chain Management at Wal-Mart: Submitted By:-Group 10Document11 paginiSupply Chain Management at Wal-Mart: Submitted By:-Group 10XanBrunoÎncă nu există evaluări

- MamalateoDocument12 paginiMamalateoKim Orven M. SolonÎncă nu există evaluări

- Sales Order Form 2019Document1 paginăSales Order Form 2019Muhammad IqbalÎncă nu există evaluări

- FILIPINO Deed of Absolute Sale, Acknowledgment Receipt and SPADocument7 paginiFILIPINO Deed of Absolute Sale, Acknowledgment Receipt and SPAJecky Delos ReyesÎncă nu există evaluări

- This Study Resource Was: Strategic Management (MGT489)Document7 paginiThis Study Resource Was: Strategic Management (MGT489)RehabUddinÎncă nu există evaluări

- Offline Marketing SimplifiedDocument54 paginiOffline Marketing SimplifiedRita AsimÎncă nu există evaluări

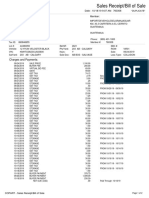

- Bill of Sale: Ve Hi Cle An D Sel Ler Inf Orma Ti OnDocument1 paginăBill of Sale: Ve Hi Cle An D Sel Ler Inf Orma Ti OnWarren NgÎncă nu există evaluări

- RetailingDocument8 paginiRetailingSharoz KhurshidÎncă nu există evaluări

- LinkedIn Templates by Brynne Tillman 1Document10 paginiLinkedIn Templates by Brynne Tillman 1Kannan Srinivasan100% (1)

- Admin Vs OperationalDocument2 paginiAdmin Vs OperationalGlen LunaÎncă nu există evaluări

- GiordanoDocument5 paginiGiordanoApple TanÎncă nu există evaluări

- Accounting Revision Notes and Assessment TasksDocument148 paginiAccounting Revision Notes and Assessment TasksJemmarOse EstacioÎncă nu există evaluări

- Teknik Telemarketing Cold CallDocument38 paginiTeknik Telemarketing Cold CallPrince-Rico Evrino100% (4)

- Manila Mandarin Hotels Vs CommissionerDocument2 paginiManila Mandarin Hotels Vs CommissionerEryl Yu100% (1)

- Glossary Entrepreneurship Development: V+TeamDocument8 paginiGlossary Entrepreneurship Development: V+TeamCorey PageÎncă nu există evaluări

- Chapter 5 The Five Generic ... StrategiesDocument20 paginiChapter 5 The Five Generic ... Strategieschelinti100% (1)

- Wizcraft CreditsDocument74 paginiWizcraft Creditsc_manceeÎncă nu există evaluări

- 166716594Document2 pagini166716594Jose El JaguarÎncă nu există evaluări

- Marginal Break EvenDocument39 paginiMarginal Break EvenNamrata NeopaneyÎncă nu există evaluări

- Graphic Design Taschen Magazine 2006Document92 paginiGraphic Design Taschen Magazine 2006foodcops86% (7)

- Nhid Ykwt: Aman LodgeDocument7 paginiNhid Ykwt: Aman LodgeravisayyesÎncă nu există evaluări