S-ar putea să vă placă și

- 2016 14 PPT Acctg1 Adjusting EntriesDocument20 pagini2016 14 PPT Acctg1 Adjusting Entriesash wu100% (3)

- MerchandisingDocument20 paginiMerchandisingDave PeraltaÎncă nu există evaluări

- Tesda Perpetual GuidelinesDocument12 paginiTesda Perpetual GuidelinesMichael Angelo Laguna Dela FuenteÎncă nu există evaluări

- PERPETUAL INVENTORY SYSTEM - Practice SetDocument25 paginiPERPETUAL INVENTORY SYSTEM - Practice SetJAY100% (2)

- Accounting Cycle of A Merchandising BusinessDocument21 paginiAccounting Cycle of A Merchandising Businesszedrick edenÎncă nu există evaluări

- BARRETO DISTRIBUTORSHIP - StudentDocument18 paginiBARRETO DISTRIBUTORSHIP - StudentEstefaniaÎncă nu există evaluări

- General Journal: Date Account Titles and Explanation Ref Debit CreditDocument17 paginiGeneral Journal: Date Account Titles and Explanation Ref Debit CreditPrecious NosaÎncă nu există evaluări

- Name of Examinee: - : Prepare The FollowingDocument15 paginiName of Examinee: - : Prepare The FollowingNoel CarpioÎncă nu există evaluări

- Problem Solving: Merchandising Problem (Periodic Inventory System)Document1 paginăProblem Solving: Merchandising Problem (Periodic Inventory System)Vincent Madrid100% (6)

- Perpetual Transactions: Journal EntriesDocument71 paginiPerpetual Transactions: Journal EntriesRona Mae AnteroÎncă nu există evaluări

- Sem Plang Merchandising Periodic Problem With AnswersDocument21 paginiSem Plang Merchandising Periodic Problem With Answerscole sprouse100% (1)

- Acc 102 PeriodicDocument16 paginiAcc 102 Periodicgerald shepy100% (1)

- Nature of A Merchandising Business: Lesson 1. Intro To MerchandisingDocument14 paginiNature of A Merchandising Business: Lesson 1. Intro To Merchandisingsophia100% (1)

- Merchandising Perpetual Inv Sys Coco Computer StoreDocument18 paginiMerchandising Perpetual Inv Sys Coco Computer StoreMadelyn Espiritu100% (4)

- ACTIVITY 6 JournalizingDocument1 paginăACTIVITY 6 JournalizingJay-ar Castillo Watin Jr.50% (4)

- Tiga Laba Laundry Shop General Journal For The Month of January 2020 Date Particulars P R Debit Credi TDocument5 paginiTiga Laba Laundry Shop General Journal For The Month of January 2020 Date Particulars P R Debit Credi TMaureen FloresÎncă nu există evaluări

- Mam Karina Template Periodic 1Document21 paginiMam Karina Template Periodic 1Claudine bea NavarreteÎncă nu există evaluări

- Acctg 1Document3 paginiAcctg 1HoneyzelOmandamPonceÎncă nu există evaluări

- Journalizing The Transactions in A Merchandising Business: Quarter 2 - Week 4Document26 paginiJournalizing The Transactions in A Merchandising Business: Quarter 2 - Week 4Marchyrella Uoiea Olin Jovenir100% (4)

- FAR Chapter4 FinalDocument43 paginiFAR Chapter4 FinalPATRICIA COLINAÎncă nu există evaluări

- Case Problem Hanievon MerchandisingDocument20 paginiCase Problem Hanievon MerchandisingPrincessjane Largo100% (1)

- Lesson 16: Accounting Practice SetDocument47 paginiLesson 16: Accounting Practice SetMai Ruiz100% (1)

- Activity/Assignment #2 - Financial Models - Comparative DataDocument5 paginiActivity/Assignment #2 - Financial Models - Comparative DataNazzer NacuspagÎncă nu există evaluări

- Recording Merchandising TransactionsDocument4 paginiRecording Merchandising Transactionsacidreign50% (2)

- Accounting Problems and Exercises4 Accounting Cycle IllustrationDocument1 paginăAccounting Problems and Exercises4 Accounting Cycle IllustrationMario Agoncillo50% (2)

- Periodic Inventory System Journal EntriesDocument16 paginiPeriodic Inventory System Journal EntriesAnonymous 2k0o6az6l50% (2)

- VAT On Merchandise Purchased and SoldDocument5 paginiVAT On Merchandise Purchased and SoldBernadette Solis100% (1)

- NCIII Key To Correction PERPETUAL INVENTORY SYSTEMDocument12 paginiNCIII Key To Correction PERPETUAL INVENTORY SYSTEMŁei Silvestre100% (1)

- Problem Solving: Merchandising Problem (Perpetual Inventory System)Document1 paginăProblem Solving: Merchandising Problem (Perpetual Inventory System)Vincent Madrid83% (6)

- Practice Problems On Special JournalsDocument24 paginiPractice Problems On Special JournalsJenny Boo50% (2)

- Closing EntriesDocument4 paginiClosing Entriesapi-299265916Încă nu există evaluări

- Thor General Merchandise ProblemDocument3 paginiThor General Merchandise ProblemEdmundo Otañes GasatanÎncă nu există evaluări

- Accounting Practice SetDocument111 paginiAccounting Practice SetMantes, Mellinia M.50% (2)

- FABM2 - Statement of Financial PositionDocument36 paginiFABM2 - Statement of Financial PositionVron Blatz100% (6)

- Act3 StatDocument33 paginiAct3 StatAllecks Juel Luchana0% (1)

- Problem Special JournalsDocument6 paginiProblem Special JournalsCarmi Fecero100% (2)

- PERPETUAL INVENTORY System TransactionDocument1 paginăPERPETUAL INVENTORY System TransactionJayMorales100% (2)

- Acctg Closing Entries, Post Closing Trial Balance and Reversing EntriesDocument21 paginiAcctg Closing Entries, Post Closing Trial Balance and Reversing EntriesDaisy Marie A. Rosel100% (1)

- The Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingDocument12 paginiThe Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingKim Patrick Victoria100% (1)

- Santa Rosa Campus City of Santa Rosa, Laguna: Polytechnic University of The PhilippinesDocument19 paginiSanta Rosa Campus City of Santa Rosa, Laguna: Polytechnic University of The PhilippinesareumÎncă nu există evaluări

- MerchandisingDocument11 paginiMerchandisingAIRA NHAIRE MECATE100% (1)

- Assignment November11 KylaAccountingDocument2 paginiAssignment November11 KylaAccountingADRIANO, Glecy C.Încă nu există evaluări

- Perpetual Inventory SystemDocument5 paginiPerpetual Inventory SystemRey ArudÎncă nu există evaluări

- 77 FDocument3 pagini77 FJohn CalvinÎncă nu există evaluări

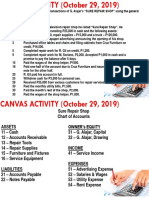

- Canvas Activity - Journalizing - Oct - 29 PDFDocument2 paginiCanvas Activity - Journalizing - Oct - 29 PDFJian Francisco100% (2)

- NameDocument17 paginiNameMARY GRACE VARGAS100% (1)

- JOB SHEET Prepare Journal EntryDocument9 paginiJOB SHEET Prepare Journal EntryIL Mare100% (1)

- Accounting For Sole Proprietorship Problem1-5Document8 paginiAccounting For Sole Proprietorship Problem1-5Rocel Domingo100% (1)

- Journal Entries in Merchandising OperationsDocument4 paginiJournal Entries in Merchandising OperationsArrabela PalmaÎncă nu există evaluări

- Merchandising FinalsDocument3 paginiMerchandising FinalsROB101512100% (1)

- Special Journals Accounting)Document15 paginiSpecial Journals Accounting)Ardialyn100% (3)

- Accounting Theory ReviewerDocument4 paginiAccounting Theory ReviewerAlbert Sean LocsinÎncă nu există evaluări

- Basic Financial Accounting and Reporting: Ishmael Y. Reyes, CPADocument32 paginiBasic Financial Accounting and Reporting: Ishmael Y. Reyes, CPAMicaela EncinasÎncă nu există evaluări

- Merchandising BusinessDocument11 paginiMerchandising BusinessABM-AKRISTINE DELA CRUZÎncă nu există evaluări

- Adjusting Entries For StudentsDocument57 paginiAdjusting Entries For Studentsselvia egayÎncă nu există evaluări

- PerpetualDocument13 paginiPerpetualEcho ClarosÎncă nu există evaluări

- Drill ABMDocument1 paginăDrill ABMGeorge Gonzales78% (23)

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionDe la EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionÎncă nu există evaluări

- VertudezDocument4 paginiVertudezralph yapÎncă nu există evaluări

- Impacts of Use of Data Analytics Performance Consulting ActivitiesDocument11 paginiImpacts of Use of Data Analytics Performance Consulting ActivitiesRhea SimoneÎncă nu există evaluări

- Clarifying Approaches To HNA HIA HeqA IIA and EqIA - HDA England - 2005Document16 paginiClarifying Approaches To HNA HIA HeqA IIA and EqIA - HDA England - 2005PublicHealthbyDesignÎncă nu există evaluări

- COMMUNICATION TO THE BOARD AND SENIOR MANAGEMENT - Internal AuditingDocument23 paginiCOMMUNICATION TO THE BOARD AND SENIOR MANAGEMENT - Internal AuditingMontilla Bambie100% (1)

- Controller Accounting Manager CPA in Detroit MI Resume Michele MarshDocument1 paginăController Accounting Manager CPA in Detroit MI Resume Michele MarshMicheleMarshÎncă nu există evaluări

- Auditors Report: Financial Result 2005-2006Document11 paginiAuditors Report: Financial Result 2005-2006Hay JirenyaaÎncă nu există evaluări

- As 1 - Disclosure of Accounting PoliciesDocument20 paginiAs 1 - Disclosure of Accounting Policiestaurianniki100% (1)

- Management New Coordinates and ChallengesDocument607 paginiManagement New Coordinates and ChallengesPetronela Georgiana CostinÎncă nu există evaluări

- Wdus Kom Nom 01Document3 paginiWdus Kom Nom 01MacmacBentedos LitonManiegoÎncă nu există evaluări

- Assurance Source Book LinksDocument69 paginiAssurance Source Book LinksfaizthemeÎncă nu există evaluări

- ABL Annual Report-2018Document404 paginiABL Annual Report-2018Usa 2021Încă nu există evaluări

- CWIP PolicyDocument6 paginiCWIP Policyeswaran69Încă nu există evaluări

- CTC Annual Report 2020Document164 paginiCTC Annual Report 2020thugnatureÎncă nu există evaluări

- Microsoft Word - Terms and ConditionsDocument3 paginiMicrosoft Word - Terms and ConditionsIsaac SamuelÎncă nu există evaluări

- EOI, Which Is Not in The Prescribed Pro-Forma, Shall Be Rejected. AnyDocument10 paginiEOI, Which Is Not in The Prescribed Pro-Forma, Shall Be Rejected. AnyHema SahuÎncă nu există evaluări

- v6 BSI Self Assesment Questionnaire 27001Document4 paginiv6 BSI Self Assesment Questionnaire 27001DonÎncă nu există evaluări

- QAIP InternalDocument12 paginiQAIP InternalMaria Rona Silvestre100% (2)

- Companies Act 2016 - TechnicalDocument13 paginiCompanies Act 2016 - TechnicalbukugendangÎncă nu există evaluări

- Standard Costing and Flexible Budget 10Document5 paginiStandard Costing and Flexible Budget 10Lhorene Hope DueñasÎncă nu există evaluări

- The Differentiation of Quality Among Auditors: Evidence From The Not-for-Profit SectorDocument17 paginiThe Differentiation of Quality Among Auditors: Evidence From The Not-for-Profit SectorAndre TaudiryÎncă nu există evaluări

- GN Cement Industry 05022021 RevDocument97 paginiGN Cement Industry 05022021 RevNetaji Dasari100% (1)

- Audit 2 l2 Test of ControlsDocument45 paginiAudit 2 l2 Test of ControlsGen AbulkhairÎncă nu există evaluări

- Caparo Industries V DickmanDocument47 paginiCaparo Industries V DickmanGeni FranzisÎncă nu există evaluări

- Internal Audit Planning and Scheduling Sample FormatDocument3 paginiInternal Audit Planning and Scheduling Sample FormatvfuntanillaÎncă nu există evaluări

- Hino - Annual Report 2015Document118 paginiHino - Annual Report 2015Wasif Pervaiz Dar100% (1)

- Board CommitteesDocument42 paginiBoard CommitteesKhusbuÎncă nu există evaluări

- Answer 2Document4 paginiAnswer 2asdfÎncă nu există evaluări

- T6 QuizDocument14 paginiT6 QuizSikina LoonÎncă nu există evaluări

- f8 IIIDocument366 paginif8 IIIThanh PhạmÎncă nu există evaluări

- ,part 2 (1) GGGDocument52 pagini,part 2 (1) GGGyechueÎncă nu există evaluări

- Case Study-Financial and Business Analysis of Kenya AirwaysDocument41 paginiCase Study-Financial and Business Analysis of Kenya AirwaysM Umar ShabbirÎncă nu există evaluări