S-ar putea să vă placă și

- Fundamentals of AccountingDocument39 paginiFundamentals of AccountingJosie Sanchez83% (40)

- Pas 7 Cash Flow StatementsDocument7 paginiPas 7 Cash Flow StatementsRechelleÎncă nu există evaluări

- Fundamentals of Accountancy Business and Management 1 PDFDocument164 paginiFundamentals of Accountancy Business and Management 1 PDFKate Parana67% (3)

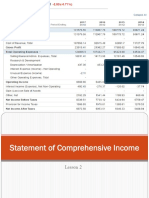

- Lesson 2 Statement of Comprehensive IncomeDocument23 paginiLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- Lesson 1 Text As Connected DiscourseDocument94 paginiLesson 1 Text As Connected DiscourseAdelyn Dizon50% (2)

- 2016 Jan 1 Cash Computer Equipment Lok, Capital: General Journal Date ParticularsDocument25 pagini2016 Jan 1 Cash Computer Equipment Lok, Capital: General Journal Date ParticularsMoon Binn100% (2)

- Fundamentals of ABM 1 & 2: Accounting ExercisesDocument22 paginiFundamentals of ABM 1 & 2: Accounting ExercisesRezel Funtilar100% (2)

- Fundamentals of Accountancy, Business and Management - 1 - ABM-11 - Q3 - W5 - Module-5-V3 (Ready For Printing)Document26 paginiFundamentals of Accountancy, Business and Management - 1 - ABM-11 - Q3 - W5 - Module-5-V3 (Ready For Printing)Glaiza Dalayoan Flores86% (14)

- Sampa Video Solution - Harvard Case SolutionDocument10 paginiSampa Video Solution - Harvard Case SolutionkanabaramitÎncă nu există evaluări

- Fundamentals of Accountancy, Business, and Management 2: ExpectationDocument131 paginiFundamentals of Accountancy, Business, and Management 2: ExpectationAngela Garcia100% (1)

- Auditing Fixed Assets and Capital Work in ProgressDocument23 paginiAuditing Fixed Assets and Capital Work in ProgressMM_AKSI87% (15)

- Module in Fabm 1: Department of Education Schools Division of Pasay CityDocument6 paginiModule in Fabm 1: Department of Education Schools Division of Pasay CityAngelica Mae SuñasÎncă nu există evaluări

- FABM1 Q4 Module 6 Preparing of Reversing EntriesDocument14 paginiFABM1 Q4 Module 6 Preparing of Reversing Entriesrio100% (1)

- 2016 14 PPT Acctg1 Adjusting EntriesDocument20 pagini2016 14 PPT Acctg1 Adjusting Entriesash wu100% (3)

- Types of Account Titles UsedDocument48 paginiTypes of Account Titles UsedKrung KrungÎncă nu există evaluări

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionDe la EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionÎncă nu există evaluări

- Fundamentals of Accountancy, Business, and Management 1: 2. Journal EntriesDocument15 paginiFundamentals of Accountancy, Business, and Management 1: 2. Journal EntriesVanessa Lou Torejas67% (3)

- CB Module 1Document63 paginiCB Module 1Jen Faye Orpilla100% (5)

- Accounting Concepts and PrinciplesDocument23 paginiAccounting Concepts and Principlesmark turbanada100% (1)

- FABM2 Module 04 (Q1-W5)Document5 paginiFABM2 Module 04 (Q1-W5)Christian Zebua100% (1)

- Fabm2 SLK Week 1 SFPDocument17 paginiFabm2 SLK Week 1 SFPMylene Santiago100% (3)

- FABM 1 - C1 - NatureOfAccountingDocument24 paginiFABM 1 - C1 - NatureOfAccountingApril Mae Villaceran100% (2)

- Fundamentals of Accountancy, Business and Management - 1 - ABM-11 - Q3 - W4 - Module-4-V3 (Ready For Printing)Document22 paginiFundamentals of Accountancy, Business and Management - 1 - ABM-11 - Q3 - W4 - Module-4-V3 (Ready For Printing)Glaiza Dalayoan Flores100% (9)

- Lesson 2 Patterns of DevelopmentDocument19 paginiLesson 2 Patterns of DevelopmentAdelyn Dizon100% (1)

- Fabm1 Module 7Document26 paginiFabm1 Module 7Randy Magbudhi100% (10)

- 07 FABM1 Module2 - Lesson1 ApplicationDocument2 pagini07 FABM1 Module2 - Lesson1 ApplicationAtasha Nicole G. Bahande100% (6)

- CFO Finance Director Controller in Los Angeles CA Resume Keith RowlandDocument2 paginiCFO Finance Director Controller in Los Angeles CA Resume Keith RowlandKeithRowlandÎncă nu există evaluări

- FABM 2 - Lesson1 5Document78 paginiFABM 2 - Lesson1 5Sis HopÎncă nu există evaluări

- Mr. Labandero Journalizing Posting and Unadjusted Trial Balance ASSIGNMENT KEYDocument8 paginiMr. Labandero Journalizing Posting and Unadjusted Trial Balance ASSIGNMENT KEYMiguel Nieves67% (6)

- GRADE 11 - Reading and Writing Claim, Fact, ValueDocument45 paginiGRADE 11 - Reading and Writing Claim, Fact, ValueZarah Kay79% (85)

- Journal and LedgersDocument3 paginiJournal and LedgersRhea Ramirez55% (11)

- FABM FS and Closing EntriesDocument18 paginiFABM FS and Closing EntriesMarchyrella Uoiea Olin Jovenir100% (1)

- Chart of Accounts 666: Fundamentals of Accountancy, Business and Management 1 (FABM 1)Document12 paginiChart of Accounts 666: Fundamentals of Accountancy, Business and Management 1 (FABM 1)Angelica ParasÎncă nu există evaluări

- Fundamentals of Accountancy, Business and Management 1Document16 paginiFundamentals of Accountancy, Business and Management 1Gladzangel Loricabv83% (6)

- Fundamentals of ABM 1Document164 paginiFundamentals of ABM 1Marissa Dulay - Sitanos67% (15)

- Internship Report MCB Bank LTDDocument100 paginiInternship Report MCB Bank LTDSajidp78663% (16)

- Adjusting EntriesDocument7 paginiAdjusting EntriesJanine MalinaoÎncă nu există evaluări

- Selecting and Organizing InformationDocument23 paginiSelecting and Organizing InformationAdelyn DizonÎncă nu există evaluări

- OS PS GayatriM Singapore 30th March2020Document2 paginiOS PS GayatriM Singapore 30th March2020abhinash biswal0% (1)

- Fundamentals of Accountancy, Business and Management - 1 - ABM-11 - Q3 - W3 - Module-3-V3 (Ready For Printing)Document21 paginiFundamentals of Accountancy, Business and Management - 1 - ABM-11 - Q3 - W3 - Module-3-V3 (Ready For Printing)Glaiza Dalayoan Flores76% (17)

- Journalizing TransactionsDocument24 paginiJournalizing TransactionsManuel Panotes Reantazo50% (2)

- Learning Activity Sheets in Fundamental of Accountancy, Business, and Management 1Document27 paginiLearning Activity Sheets in Fundamental of Accountancy, Business, and Management 1Rheyjhen Cadawas40% (5)

- Bank Recon.Document8 paginiBank Recon.Freya Evangeline100% (3)

- 1.2 Accounting Concepts and PrinciplesDocument4 pagini1.2 Accounting Concepts and PrinciplesVillamor NiezÎncă nu există evaluări

- Accounting PrincipleDocument24 paginiAccounting PrincipleAlma Dimaranan-Acuña83% (6)

- FABM-1 Summary ExaminationDocument7 paginiFABM-1 Summary ExaminationSheldon Bazinga67% (3)

- Republic of The Philippines Department of Education Region Vii, Central Visayas Division of Cebu Province Self-Learning Home Task (SLHT)Document20 paginiRepublic of The Philippines Department of Education Region Vii, Central Visayas Division of Cebu Province Self-Learning Home Task (SLHT)Joseph Entera100% (2)

- Lesson 9.4 Adjusting EntriesDocument36 paginiLesson 9.4 Adjusting EntriesDanica Medina50% (2)

- Fabm2: Quarter 1 Week 5 Module 5Document18 paginiFabm2: Quarter 1 Week 5 Module 5Micah GÎncă nu există evaluări

- Module 7Document8 paginiModule 7Charissa Jamis ChingwaÎncă nu există evaluări

- Week 7-8Document8 paginiWeek 7-8Kim Albero Cubel0% (1)

- Drill ABMDocument1 paginăDrill ABMGeorge Gonzales78% (23)

- What's MoreDocument5 paginiWhat's MoreJade Payba50% (2)

- Debit AccountancyDocument33 paginiDebit AccountancyJuancho Miguel0% (1)

- Fabm Analysis and Interpretation of Financial Statements 1Document4 paginiFabm Analysis and Interpretation of Financial Statements 1Mylen Noel Elgincolin Manlapaz67% (6)

- Abm General and Special JournalDocument63 paginiAbm General and Special JournalEstelle Gammad33% (3)

- Abm Abm Abm AbmDocument27 paginiAbm Abm Abm AbmNoaj Palon100% (1)

- Lesson 3: Books of Accounts: Module No. 3: Intensifying Accounting Knowledge Through The Accounting Equation, Types ofDocument13 paginiLesson 3: Books of Accounts: Module No. 3: Intensifying Accounting Knowledge Through The Accounting Equation, Types ofPonsica RomeoÎncă nu există evaluări

- Qualitative FormatDocument45 paginiQualitative FormatRachellyn Limentang100% (1)

- FABM2 Module 06 (Q1-W7)Document8 paginiFABM2 Module 06 (Q1-W7)Christian Zebua75% (4)

- BM Las q1 w5 8 FinalDocument35 paginiBM Las q1 w5 8 FinalKatrina BinayÎncă nu există evaluări

- Business Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Firm (Part 1)Document35 paginiBusiness Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Firm (Part 1)Ponsica Romeo50% (2)

- Performance Task JournalizingDocument1 paginăPerformance Task Journalizinganna paula esguerra50% (10)

- 13 Accounting Cycle of A Service Business 2Document28 pagini13 Accounting Cycle of A Service Business 2Ashley Judd Mallonga Beran60% (5)

- Topic: Accounting Cycle of A Service BusinessDocument5 paginiTopic: Accounting Cycle of A Service BusinessJohn Rey BusimeÎncă nu există evaluări

- Module 3Document47 paginiModule 3Harrold HarryÎncă nu există evaluări

- 2QUIZ3 - With AnswerDocument1 pagină2QUIZ3 - With AnswerMarilyn Nelmida Tamayo100% (1)

- Forms of Business Organization HighlightDocument8 paginiForms of Business Organization Highlightks505eÎncă nu există evaluări

- Module 4 PDFDocument5 paginiModule 4 PDFCharissa Jamis ChingwaÎncă nu există evaluări

- Accounting Concepts and PrinciplesDocument26 paginiAccounting Concepts and PrinciplesWindelyn Iligan100% (2)

- Textual EvidenceDocument17 paginiTextual EvidenceAdelyn DizonÎncă nu există evaluări

- Department of Education: Modules For Summer Class Remediation For Reading and WritingDocument5 paginiDepartment of Education: Modules For Summer Class Remediation For Reading and WritingAdelyn DizonÎncă nu există evaluări

- Accounting EquationDocument38 paginiAccounting EquationAdelyn DizonÎncă nu există evaluări

- PowerpointDocument39 paginiPowerpointAdelyn DizonÎncă nu există evaluări

- Inventories: Ind-As 2Document10 paginiInventories: Ind-As 2ambarishÎncă nu există evaluări

- Share Based Payments by Ca PS BeniwalDocument16 paginiShare Based Payments by Ca PS Beniwalhrudaya boys100% (1)

- AMFI Question & AnswerDocument67 paginiAMFI Question & AnswerVirag67% (3)

- The Goldman Sachs Group - Financial Analysis AssignmentDocument4 paginiThe Goldman Sachs Group - Financial Analysis AssignmentJeremy RichuÎncă nu există evaluări

- Module 6 Chapter 8 Output VAT Zero Rated SalesDocument5 paginiModule 6 Chapter 8 Output VAT Zero Rated SalesChris SumandeÎncă nu există evaluări

- Customer LedgerDocument1 paginăCustomer LedgerDhillaÎncă nu există evaluări

- Maraston Marble Corporation Is Considering A Merger With The ConDocument1 paginăMaraston Marble Corporation Is Considering A Merger With The ConAmit Pandey0% (1)

- CAPM and RatiosDocument5 paginiCAPM and Ratiospankaj chandnaÎncă nu există evaluări

- Quiz 3 Adjusting Entries Sec BDocument3 paginiQuiz 3 Adjusting Entries Sec BHome PhoneÎncă nu există evaluări

- IAS 12 - Income TaxesDocument55 paginiIAS 12 - Income Taxesrafid aliÎncă nu există evaluări

- Investment Decision: Unit IiiDocument50 paginiInvestment Decision: Unit IiiFara HameedÎncă nu există evaluări

- Difference Between Partnership and CorporationDocument1 paginăDifference Between Partnership and CorporationDanica Mei DeguzmanÎncă nu există evaluări

- NEE Stock Price Forecasts-3Document16 paginiNEE Stock Price Forecasts-3arjuÎncă nu există evaluări

- 12sm Accountancy Eng 2021 22Document512 pagini12sm Accountancy Eng 2021 22Piyush ChhajerÎncă nu există evaluări

- Financial Management 2 Assignment 1: Dividend Policy at FPL GroupDocument9 paginiFinancial Management 2 Assignment 1: Dividend Policy at FPL GroupDiv_nÎncă nu există evaluări

- Dr. Domingo Clinic Chart of Accounts: Account Numbers Account Titles Current AssetsDocument2 paginiDr. Domingo Clinic Chart of Accounts: Account Numbers Account Titles Current AssetsmariaÎncă nu există evaluări

- Using The Gordon Dividend Model. Compare The Cost of Equity Computed On The BasisDocument2 paginiUsing The Gordon Dividend Model. Compare The Cost of Equity Computed On The BasisONASHI DEVNANI BBAÎncă nu există evaluări

- Sampa Video Case SolutionDocument10 paginiSampa Video Case SolutionrahulsinhadpsÎncă nu există evaluări

- Assignment#2Document3 paginiAssignment#2Wuhao KoÎncă nu există evaluări

- Sail Pay RevisionDocument4 paginiSail Pay Revisionhimanshu2010swÎncă nu există evaluări

- Aud Prob Compilation 1Document31 paginiAud Prob Compilation 1Chammy TeyÎncă nu există evaluări

- 07.ind As 102Document35 pagini07.ind As 102Pranjul AgrawalÎncă nu există evaluări

- Gap FillingDocument2 paginiGap FillingÁnh LyÎncă nu există evaluări

- Dandot 2008 AnnualDocument39 paginiDandot 2008 AnnualMuhammad haseebÎncă nu există evaluări