S-ar putea să vă placă și

- GST IntroductionDocument42 paginiGST IntroductionAnant singhÎncă nu există evaluări

- Types of Supply GSTDocument46 paginiTypes of Supply GSTRajatKumarÎncă nu există evaluări

- Executive Supplement GSTDocument84 paginiExecutive Supplement GSThkakani1Încă nu există evaluări

- Ghanshyam 1813 PPT Public FinanceDocument64 paginiGhanshyam 1813 PPT Public FinanceShivansh JhaÎncă nu există evaluări

- Heartiest Welcome To All Bachelor of Commerce Students, Scottish Church College, KolkataDocument33 paginiHeartiest Welcome To All Bachelor of Commerce Students, Scottish Church College, KolkataBaymaXÎncă nu există evaluări

- GST and Tally ERP 9: A Comparative StudyDocument52 paginiGST and Tally ERP 9: A Comparative StudyCandy CrushÎncă nu există evaluări

- GST Oct 17Document23 paginiGST Oct 17himanÎncă nu există evaluări

- Goods and Service Tax (GST)Document19 paginiGoods and Service Tax (GST)Saurabh Kumar SharmaÎncă nu există evaluări

- GST - Answer 2Document9 paginiGST - Answer 2Tarun SolankiÎncă nu există evaluări

- Overview GSTDocument56 paginiOverview GSTrahulÎncă nu există evaluări

- GST - 1 FinalDocument21 paginiGST - 1 FinalswatitankasaliÎncă nu există evaluări

- GST Certificate CourseDocument4 paginiGST Certificate Coursebmbabu27Încă nu există evaluări

- GST in BankingDocument23 paginiGST in BankingNareshaasatÎncă nu există evaluări

- 17.01.2020, 2. S.V.Kasi Visweswara Rao Sir, Joint Commissioner (ST), Introduction and Evolution of Indirect Taxation in IndiaDocument30 pagini17.01.2020, 2. S.V.Kasi Visweswara Rao Sir, Joint Commissioner (ST), Introduction and Evolution of Indirect Taxation in IndiaMANAN KOTHARIÎncă nu există evaluări

- GST Overview Rachana 1Document31 paginiGST Overview Rachana 1Path A Way AheadÎncă nu există evaluări

- Composition Scheme SEC 10 - GST PDFDocument20 paginiComposition Scheme SEC 10 - GST PDFTushar SinghÎncă nu există evaluări

- Presentation On GST by Himanshu and KrishnaDocument21 paginiPresentation On GST by Himanshu and KrishnahimanshuÎncă nu există evaluări

- Indirect Taxation: 40MBAFM403Document23 paginiIndirect Taxation: 40MBAFM403Divya SÎncă nu există evaluări

- GST 2018 Full Solved PaperDocument15 paginiGST 2018 Full Solved PaperKomala100% (1)

- Goods and Services Tax (GST) in India: Ca R.K.BhallaDocument27 paginiGoods and Services Tax (GST) in India: Ca R.K.BhallaAditya V v s r kÎncă nu există evaluări

- GST PPT June19Document65 paginiGST PPT June19yash bhushanÎncă nu există evaluări

- GST OverviewDocument41 paginiGST OverviewNalin KÎncă nu există evaluări

- Gst Inter CA Q&A BookDocument177 paginiGst Inter CA Q&A BookHetal BeraÎncă nu există evaluări

- Chapter 1 Introduction To GSTDocument5 paginiChapter 1 Introduction To GSTabhay javiyaÎncă nu există evaluări

- GST Goods & Service TaxDocument36 paginiGST Goods & Service Taxhahire100% (2)

- GST Implementation in India ReportDocument10 paginiGST Implementation in India ReportShreya VermaÎncă nu există evaluări

- Composition Scheme Sec. 10: Ques-1 What Is Composition Levy Under GST?Document12 paginiComposition Scheme Sec. 10: Ques-1 What Is Composition Levy Under GST?Tapan BarikÎncă nu există evaluări

- GST Refund Under Tax Laws: An Analysis: Hidayatullah National Law University Raipur (C.G.)Document20 paginiGST Refund Under Tax Laws: An Analysis: Hidayatullah National Law University Raipur (C.G.)Atul VermaÎncă nu există evaluări

- Chapter 1: Introduction To GST 1.1 Basics of GST 1.1.1 What Is GST?Document13 paginiChapter 1: Introduction To GST 1.1 Basics of GST 1.1.1 What Is GST?Ashutosh papelÎncă nu există evaluări

- History of taxation in India and key advantages of GSTDocument161 paginiHistory of taxation in India and key advantages of GSTAnurag KandariÎncă nu există evaluări

- Goods & Service TaxDocument4 paginiGoods & Service TaxAkshay ModakÎncă nu există evaluări

- What Is GST? Definition of Goods & Services TaxDocument9 paginiWhat Is GST? Definition of Goods & Services Taxzarfarie aron100% (1)

- Introduction To GSTDocument33 paginiIntroduction To GSTRohit Rajesh RathiÎncă nu există evaluări

- GST notes: Key concepts and benefitsDocument15 paginiGST notes: Key concepts and benefitsswetha shree chavan mÎncă nu există evaluări

- Salient Features: 1. Concept of SupplyDocument9 paginiSalient Features: 1. Concept of SupplyAnu DheepthiÎncă nu există evaluări

- Notes - Indirect TaxesDocument18 paginiNotes - Indirect TaxesSajan N ThomasÎncă nu există evaluări

- GST registration rules and proceduresDocument10 paginiGST registration rules and proceduresPooja MauryaÎncă nu există evaluări

- Direct Tax Vs Indirect TaxDocument44 paginiDirect Tax Vs Indirect TaxShuchi BhatiaÎncă nu există evaluări

- Direct Tax Vs Indirect TaxDocument44 paginiDirect Tax Vs Indirect TaxShuchi BhatiaÎncă nu există evaluări

- GST Unit 4Document48 paginiGST Unit 4SANSKRITI YADAV 22DM236Încă nu există evaluări

- 1) Explain GST and Its BenefitsDocument14 pagini1) Explain GST and Its BenefitsRohit VishwakarmaÎncă nu există evaluări

- 2 How GST WorksDocument17 pagini2 How GST WorkspriyaÎncă nu există evaluări

- GST FrameworkDocument21 paginiGST FrameworkExecutive EngineerÎncă nu există evaluări

- Understanding GST: Benefits, Registration Process & Electronic Credit LedgerDocument8 paginiUnderstanding GST: Benefits, Registration Process & Electronic Credit LedgerFlemin GeorgeÎncă nu există evaluări

- Overview of GST - PPT For GACDocument57 paginiOverview of GST - PPT For GACRonak DesaiÎncă nu există evaluări

- Goods and Service Tax BBA 309 Unit 1: Prepared & Presented by Ms. Shanu Jain Assistant Professor, DME Management SchoolDocument30 paginiGoods and Service Tax BBA 309 Unit 1: Prepared & Presented by Ms. Shanu Jain Assistant Professor, DME Management SchoolNikhil KumarÎncă nu există evaluări

- GST TheoryDocument147 paginiGST TheoryNeha SharmaÎncă nu există evaluări

- Composition SchemeDocument4 paginiComposition Schemecloudstorage567Încă nu există evaluări

- Complete GST QB by CA Pranav ChandakDocument210 paginiComplete GST QB by CA Pranav ChandakNishanth NishanthÎncă nu există evaluări

- GST BasicsDocument56 paginiGST BasicsrahulÎncă nu există evaluări

- VAT - MCQ Test Questions by Mahbub SirDocument16 paginiVAT - MCQ Test Questions by Mahbub SirAysha Alam100% (1)

- GST Merged (End Sem)Document346 paginiGST Merged (End Sem)kajal goyalÎncă nu există evaluări

- Goods & Services Tax - GST: Amar ShawDocument15 paginiGoods & Services Tax - GST: Amar ShawChetan KaushikÎncă nu există evaluări

- Goods Severvice Tax Costom Duty 1Document51 paginiGoods Severvice Tax Costom Duty 1sonal20020705Încă nu există evaluări

- Sem 4 Project (Impact of GST On Restaurants) 1Document46 paginiSem 4 Project (Impact of GST On Restaurants) 1Priyanka Satam100% (1)

- UNIT II GSTDocument19 paginiUNIT II GSTAbhi NandanaÎncă nu există evaluări

- Cma Inter GR 1 Financial Accounting Ebook June 2021 OnwardsDocument358 paginiCma Inter GR 1 Financial Accounting Ebook June 2021 OnwardsSarath KumarÎncă nu există evaluări

- VAT vs GST: Key Differences Between Value Added Tax and Goods and Services TaxDocument7 paginiVAT vs GST: Key Differences Between Value Added Tax and Goods and Services TaxArundhuti RoyÎncă nu există evaluări

- 18 GSTDocument1.042 pagini18 GSTSwetaÎncă nu există evaluări

- Money Market EcoDocument13 paginiMoney Market EcoLakshmi NairÎncă nu există evaluări

- Aggregate Demand and Supply Models ExplainedDocument37 paginiAggregate Demand and Supply Models ExplainedLakshmi NairÎncă nu există evaluări

- MRPDocument2 paginiMRPLakshmi NairÎncă nu există evaluări

- Registration - PersonsDocument14 paginiRegistration - PersonsLakshmi NairÎncă nu există evaluări

- OM Course Handout - 2021-Sec B and FDocument9 paginiOM Course Handout - 2021-Sec B and FLakshmi NairÎncă nu există evaluări

- Practice Problem On Factor AnalysisDocument3 paginiPractice Problem On Factor AnalysisLakshmi NairÎncă nu există evaluări

- Marketing Project TopicsDocument8 paginiMarketing Project TopicsLakshmi NairÎncă nu există evaluări

- A Study About Out of Home Advertising PDFDocument7 paginiA Study About Out of Home Advertising PDFLakshmi NairÎncă nu există evaluări

- Branding and Packaging Project Class 12 Marketing (783)Document57 paginiBranding and Packaging Project Class 12 Marketing (783)lovellmenezes67% (9)

- Factor Analysis ExerciseDocument1 paginăFactor Analysis ExerciseLakshmi NairÎncă nu există evaluări

- FM-2 Course Handout 2019-20Document6 paginiFM-2 Course Handout 2019-20Lakshmi NairÎncă nu există evaluări

- Logistics Regression TV ViewingDocument2 paginiLogistics Regression TV ViewingLakshmi NairÎncă nu există evaluări

- Financial ManagementDocument132 paginiFinancial ManagementHemant SolankiÎncă nu există evaluări

- End-Term Paper Financial Management - 2 Set - A: SolutionDocument7 paginiEnd-Term Paper Financial Management - 2 Set - A: SolutionLakshmi NairÎncă nu există evaluări

- Tax - IntroductionDocument7 paginiTax - IntroductionLakshmi NairÎncă nu există evaluări

- 3-4. Measuring National Output IncomeDocument45 pagini3-4. Measuring National Output IncomeApoorva MishraÎncă nu există evaluări

- HRM-End SemDocument9 paginiHRM-End SemLakshmi NairÎncă nu există evaluări

- Datta Sir's Notes PDFDocument25 paginiDatta Sir's Notes PDFLakshmi NairÎncă nu există evaluări

- Two Special LP Models Solving Transportation and Assignment ProblemsDocument12 paginiTwo Special LP Models Solving Transportation and Assignment ProblemsJennybabe PetaÎncă nu există evaluări

- MODI VAM methods transportation problems tutorialDocument10 paginiMODI VAM methods transportation problems tutorialVivek KumarÎncă nu există evaluări

- Answers To The Respective Questions Are Given Below inDocument7 paginiAnswers To The Respective Questions Are Given Below inLakshmi NairÎncă nu există evaluări

- Linear Regression ExerciseDocument2 paginiLinear Regression ExerciseLakshmi NairÎncă nu există evaluări

- Answers To The Respective Questions Are Given Below inDocument7 paginiAnswers To The Respective Questions Are Given Below inLakshmi NairÎncă nu există evaluări

- Pharmaceutical IndustryDocument26 paginiPharmaceutical IndustryLakshmi NairÎncă nu există evaluări

- SEBI Circular On UPIDocument40 paginiSEBI Circular On UPISohamRoyÎncă nu există evaluări

- Ipo IssuesDocument22 paginiIpo Issuesvkgopu100% (1)

- IPO Grading Guide - Factors, Process & How Grades Help InvestorsDocument4 paginiIPO Grading Guide - Factors, Process & How Grades Help InvestorsSachin SharmaÎncă nu există evaluări

- FM-2 Course Handout 2019-20Document6 paginiFM-2 Course Handout 2019-20Lakshmi NairÎncă nu există evaluări

- Figure - International Capital MarketsDocument1 paginăFigure - International Capital MarketsLakshmi NairÎncă nu există evaluări

- Filling, Assessment and AuditDocument38 paginiFilling, Assessment and AuditLakshmi NairÎncă nu există evaluări

- Laroche Landscaping Has Collected The Following Data For The December PDFDocument1 paginăLaroche Landscaping Has Collected The Following Data For The December PDFhassan taimourÎncă nu există evaluări

- PDFDocument4 paginiPDFAmit vohraÎncă nu există evaluări

- Apple - Income StatementDocument5 paginiApple - Income StatementhappycolourÎncă nu există evaluări

- State Bank of IndiaDocument2 paginiState Bank of Indiakiran gemsÎncă nu există evaluări

- 1571988702732Document33 pagini1571988702732LS GUPTAÎncă nu există evaluări

- Collector v. UstDocument2 paginiCollector v. UstEynab PerezÎncă nu există evaluări

- 5 Days 4 Nights All-Inclusive Package at Hard Rock Hotel Riviera MayaDocument8 pagini5 Days 4 Nights All-Inclusive Package at Hard Rock Hotel Riviera Mayamaclovio ritcherÎncă nu există evaluări

- Tax Invoice: RAJKOT GAS SERVICE (000010176)Document1 paginăTax Invoice: RAJKOT GAS SERVICE (000010176)Rahul ShuklaÎncă nu există evaluări

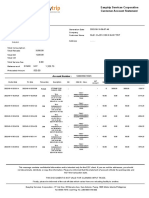

- ESC Customer Account StatementDocument2 paginiESC Customer Account StatementJake CastañedaÎncă nu există evaluări

- Consumer Behaviour in The Credit Card MarketDocument9 paginiConsumer Behaviour in The Credit Card Marketmrabie2004Încă nu există evaluări

- Petty CashDocument6 paginiPetty Cashapi-373043480% (5)

- What Is Tax?Document3 paginiWhat Is Tax?Aque LangtoeÎncă nu există evaluări

- Karim InvoiceDocument1 paginăKarim InvoiceazzedineÎncă nu există evaluări

- 2T20202021 Tuition Fee Rates IARFA FEUDocument24 pagini2T20202021 Tuition Fee Rates IARFA FEUKarina LeoÎncă nu există evaluări

- Accounting For Labor Part 2Document11 paginiAccounting For Labor Part 2Ghillian Mae GuiangÎncă nu există evaluări

- FIBER BILL STATEMENTDocument3 paginiFIBER BILL STATEMENTAnusha GodavarthyÎncă nu există evaluări

- TransNum Sep 14 104127Document1 paginăTransNum Sep 14 1041273sha CEBREUSÎncă nu există evaluări

- HSBC UAE Corporate Tariff and Charges GuideDocument23 paginiHSBC UAE Corporate Tariff and Charges GuideqweeeÎncă nu există evaluări

- Limits On Internet BankingDocument1 paginăLimits On Internet BankingAvinash BillaÎncă nu există evaluări

- Quotation.782 Juniper v2.5 HardwareDocument1 paginăQuotation.782 Juniper v2.5 HardwareFAVE ONEÎncă nu există evaluări

- CHAPTER 13 A - Regular Allowable Itemized DeductionsDocument4 paginiCHAPTER 13 A - Regular Allowable Itemized DeductionsDeviane CalabriaÎncă nu există evaluări

- Navin Fluorine Advanced Sciences LTD - 346 - 22-11-2021Document1 paginăNavin Fluorine Advanced Sciences LTD - 346 - 22-11-2021Pragnesh PrajapatiÎncă nu există evaluări

- Statement of Account As at 16 July 2023: For Adjust Alignment Issue, Didn't RemoveDocument2 paginiStatement of Account As at 16 July 2023: For Adjust Alignment Issue, Didn't RemovekakakkawaiiÎncă nu există evaluări

- MEDC Guidelines For The Obsolete Property Rehabilitation ActDocument2 paginiMEDC Guidelines For The Obsolete Property Rehabilitation ActDillon DavisÎncă nu există evaluări

- Project Report Table of Content: 1004 Financial Planning For Salaried Employee and Strategies For Tax SavingsDocument2 paginiProject Report Table of Content: 1004 Financial Planning For Salaried Employee and Strategies For Tax SavingsSai VarunÎncă nu există evaluări

- Unicredit vs. IngDocument3 paginiUnicredit vs. IngAlina AndrioaeÎncă nu există evaluări

- Invoice 73801387Document1 paginăInvoice 73801387A kumarÎncă nu există evaluări

- Wells Fargo Everyday CheckingDocument4 paginiWells Fargo Everyday Checkingpeter.pucciÎncă nu există evaluări

- W 8BEN E Form 2023Document8 paginiW 8BEN E Form 2023Barbara OliveiraÎncă nu există evaluări

- ITNS 281 TDS/TCS ChallanDocument3 paginiITNS 281 TDS/TCS ChallanC.A. Ankit JainÎncă nu există evaluări