S-ar putea să vă placă și

- Cambridge International As and A Level Business Studies Revision GuideDocument217 paginiCambridge International As and A Level Business Studies Revision GuideAlyan Hanif92% (12)

- Mystmt - 2022 11 09Document5 paginiMystmt - 2022 11 09sylvia100% (2)

- Excel Solutions To CasesDocument32 paginiExcel Solutions To Cases박지훈Încă nu există evaluări

- Gyro N Mag Compass TestDocument3 paginiGyro N Mag Compass TestMahami M ProsperÎncă nu există evaluări

- ProjectreportonexploringexpresscargoDocument43 paginiProjectreportonexploringexpresscargosanzitÎncă nu există evaluări

- What Does Mean Objectives, Why Is So Important To Define... How Could You Categorize The Objectives?Document3 paginiWhat Does Mean Objectives, Why Is So Important To Define... How Could You Categorize The Objectives?Ruth E BernuyÎncă nu există evaluări

- Management Concepts - The Four Functions of ManagementDocument6 paginiManagement Concepts - The Four Functions of Managementpleasantjunk6152100% (1)

- Management and Human ResourcesDocument20 paginiManagement and Human Resourcesdiamond princessesÎncă nu există evaluări

- Goals & Objectives PDFDocument3 paginiGoals & Objectives PDFAbhishek AgarwalÎncă nu există evaluări

- The What and Why: of PlanningDocument7 paginiThe What and Why: of PlanningHạnh Anh Ngô NguyễnÎncă nu există evaluări

- The Nature and Levels of Planning and TypesDocument20 paginiThe Nature and Levels of Planning and TypesLala Ckee100% (1)

- 8 Lo 2Document4 pagini8 Lo 2Sinta DewiÎncă nu există evaluări

- Lesson 3 - BFDocument50 paginiLesson 3 - BFPhill SamonteÎncă nu există evaluări

- Unit 2 CC 1Document25 paginiUnit 2 CC 1Kamlesh AgrawalÎncă nu există evaluări

- Planning Class 12 NotesDocument20 paginiPlanning Class 12 NotesRenu GujralÎncă nu există evaluări

- Chapter 8-1Document19 paginiChapter 8-1AsMa BaigÎncă nu există evaluări

- Topic 3 FINANCIAL PLANNING AND FORECASTINGDocument4 paginiTopic 3 FINANCIAL PLANNING AND FORECASTINGFORCHIA MAE CUTARÎncă nu există evaluări

- Vision, Mission, Objectives ...Document5 paginiVision, Mission, Objectives ...elsha ayeleÎncă nu există evaluări

- Foundation of Planning: Chapter No. 07Document24 paginiFoundation of Planning: Chapter No. 07Hasnain1991Încă nu există evaluări

- Planning ComponentsDocument4 paginiPlanning ComponentsEcal MbunaÎncă nu există evaluări

- Teak WoodDocument10 paginiTeak WoodFransy AlbertoÎncă nu există evaluări

- Business FinanceDocument51 paginiBusiness FinanceMary Joyce Camille ParasÎncă nu există evaluări

- Handout in Essentials of ManagementDocument7 paginiHandout in Essentials of ManagementsamcaridoÎncă nu există evaluări

- Types of Strategic PlanningDocument2 paginiTypes of Strategic Planning06675354dÎncă nu există evaluări

- Management: Chapter 7: Foundations of PlanningDocument65 paginiManagement: Chapter 7: Foundations of PlanningalptokerÎncă nu există evaluări

- Assignment 1 B.ed Code 8605Document12 paginiAssignment 1 B.ed Code 8605Atif RehmanÎncă nu există evaluări

- Chapter 6 - Goals and ObjectivesDocument5 paginiChapter 6 - Goals and ObjectivesJUN GERONAÎncă nu există evaluări

- Performance Management Framework & HR Perspective: Research Ajit SawantDocument29 paginiPerformance Management Framework & HR Perspective: Research Ajit SawantVicky SurtiÎncă nu există evaluări

- Smu Mba Mpob ProjectDocument10 paginiSmu Mba Mpob ProjectjobinÎncă nu există evaluări

- Study Article by Don HofstrandDocument6 paginiStudy Article by Don HofstrandMuhammad AfzalÎncă nu există evaluări

- Fundamentals of Planning: Sekolah Tinngi Ilmu Ekonomi Muhammadiyah BandungDocument8 paginiFundamentals of Planning: Sekolah Tinngi Ilmu Ekonomi Muhammadiyah BandungSuryakant DakshÎncă nu există evaluări

- Lesson No. 3 - Organizational PlanningDocument36 paginiLesson No. 3 - Organizational Planningjun junÎncă nu există evaluări

- Chapter No..5Document30 paginiChapter No..5yousuf AhmedÎncă nu există evaluări

- Mob Chapter 2Document14 paginiMob Chapter 2alena persadÎncă nu există evaluări

- Unit 3 BMDocument42 paginiUnit 3 BMAayamÎncă nu există evaluări

- A ManagerDocument4 paginiA ManagervishnukpÎncă nu există evaluări

- Chapter 2. PlanningDocument17 paginiChapter 2. PlanningAsm Saifur RahmanÎncă nu există evaluări

- LM Notes 4Document7 paginiLM Notes 4Michy MichÎncă nu există evaluări

- Explain The Characteristics of Annual Objectives: John A Pearce II & Richard B. Robinson, JRDocument3 paginiExplain The Characteristics of Annual Objectives: John A Pearce II & Richard B. Robinson, JRAlemayehu Demeke100% (1)

- PlanDocument12 paginiPlansajjadÎncă nu există evaluări

- Business FinanceDocument13 paginiBusiness FinancenattoykoÎncă nu există evaluări

- 4th Lecture PlanningDocument24 pagini4th Lecture PlanningHajra FarooqÎncă nu există evaluări

- 1658245108UNIT 2 Strategic PlanningDocument13 pagini1658245108UNIT 2 Strategic PlanningAnthony MwangiÎncă nu există evaluări

- Unit - 5 Public AdministrationDocument16 paginiUnit - 5 Public AdministrationashusinghÎncă nu există evaluări

- ORGANIZATION AND MANAGEMENT Not FinalDocument67 paginiORGANIZATION AND MANAGEMENT Not Finalmerlita rivadeneraÎncă nu există evaluări

- AssignmentDocument20 paginiAssignmentBetinol RachelÎncă nu există evaluări

- Mgemod 2Document103 paginiMgemod 2Meenakshy PanickerÎncă nu există evaluări

- Planning and OrganizationDocument15 paginiPlanning and OrganizationGemechis JiregnaÎncă nu există evaluări

- Organizational AnalysisDocument6 paginiOrganizational AnalysisEJ LagatÎncă nu există evaluări

- Learning Competencies: Business FinanceDocument6 paginiLearning Competencies: Business FinancehiÎncă nu există evaluări

- Planning To Plan: Strategic Plans Are Designed With The Entire Organization in Mind and Begin With AnDocument5 paginiPlanning To Plan: Strategic Plans Are Designed With The Entire Organization in Mind and Begin With Anjoan quiamcoÎncă nu există evaluări

- Management Theory Chapter 3Document42 paginiManagement Theory Chapter 3AddiÎncă nu există evaluări

- Creating A Mission StatementDocument6 paginiCreating A Mission Statementram_babu_59Încă nu există evaluări

- Planning: Meaning, Types and Advantages Meaning of PlanningDocument7 paginiPlanning: Meaning, Types and Advantages Meaning of PlanningabrarÎncă nu există evaluări

- Business PlanningDocument46 paginiBusiness PlanningamiahÎncă nu există evaluări

- Management Final NoteDocument49 paginiManagement Final NoteManvi BaglaÎncă nu există evaluări

- Unit-2 Planning & Decision Making PlanningDocument33 paginiUnit-2 Planning & Decision Making PlanningParkhi AgarwalÎncă nu există evaluări

- BPSM Notes of Unit 1Document6 paginiBPSM Notes of Unit 1Arpita DevÎncă nu există evaluări

- Assignment of Management Principles and Practices - FT 101CDocument9 paginiAssignment of Management Principles and Practices - FT 101CVarunKeshariÎncă nu există evaluări

- Unit3 Ba XiiDocument22 paginiUnit3 Ba XiimisganabbbbbbbbbbÎncă nu există evaluări

- Organization and ManagementDocument15 paginiOrganization and Managementacuna.alexÎncă nu există evaluări

- Management of BusinessDocument25 paginiManagement of Businesstemar atkinsonÎncă nu există evaluări

- Goals and Objectives -: how to tell if YOU + the Organization are on the right trackDe la EverandGoals and Objectives -: how to tell if YOU + the Organization are on the right trackÎncă nu există evaluări

- Smart Goals: Everything You Need to Know About Setting S.M.A.R.T GoalsDe la EverandSmart Goals: Everything You Need to Know About Setting S.M.A.R.T GoalsEvaluare: 4 din 5 stele4/5 (1)

- SMART Criteria: Become more successful by setting better goalsDe la EverandSMART Criteria: Become more successful by setting better goalsEvaluare: 5 din 5 stele5/5 (3)

- Definition of Terms: Appendix IDocument3 paginiDefinition of Terms: Appendix IMahami M ProsperÎncă nu există evaluări

- 945 - Pilot On Board - Working TogetherDocument29 pagini945 - Pilot On Board - Working TogetherMahami M ProsperÎncă nu există evaluări

- Gyro Compass: Basic PrinciplesDocument11 paginiGyro Compass: Basic PrinciplesMahami M ProsperÎncă nu există evaluări

- Synergy Exam DetailsDocument3 paginiSynergy Exam DetailsMahami M ProsperÎncă nu există evaluări

- 0792 - Prevention and Reaction To Oil Spills - OPA 90Document23 pagini0792 - Prevention and Reaction To Oil Spills - OPA 90Mahami M ProsperÎncă nu există evaluări

- Schulte Group1Document3 paginiSchulte Group1Mahami M ProsperÎncă nu există evaluări

- AmplitudesDocument7 paginiAmplitudesMahami M ProsperÎncă nu există evaluări

- P01 - PB Crew Application Form 01 Apr 18 Non FILDocument4 paginiP01 - PB Crew Application Form 01 Apr 18 Non FILMahami M Prosper0% (1)

- Luminous Range DiagramDocument1 paginăLuminous Range DiagramMahami M ProsperÎncă nu există evaluări

- Ship Education Test Liquefied Gas TankersDocument11 paginiShip Education Test Liquefied Gas TankersMahami M ProsperÎncă nu există evaluări

- Basic Fire FightingDocument23 paginiBasic Fire FightingMahami M ProsperÎncă nu există evaluări

- Ka3 2 MARITIMECOMMUNICATIONSIDENTIFYINGCURRENTANDDocument9 paginiKa3 2 MARITIMECOMMUNICATIONSIDENTIFYINGCURRENTANDMahami M ProsperÎncă nu există evaluări

- Music Lesson by SlidesgoDocument38 paginiMusic Lesson by SlidesgoMahami M ProsperÎncă nu există evaluări

- McMurdo Group Marine Products PresentationDocument21 paginiMcMurdo Group Marine Products PresentationMahami M ProsperÎncă nu există evaluări

- METDocument2 paginiMETMahami M ProsperÎncă nu există evaluări

- Ron Rice 4 27 10Document37 paginiRon Rice 4 27 10Mahami M ProsperÎncă nu există evaluări

- Just Us! CafeDocument3 paginiJust Us! CafeAditya WibisanaÎncă nu există evaluări

- Business PlanDocument6 paginiBusiness PlanAshley Joy Delos ReyesÎncă nu există evaluări

- Chapter 15 Data Managment Maturity Assessment - DONE DONE DONEDocument16 paginiChapter 15 Data Managment Maturity Assessment - DONE DONE DONERoche ChenÎncă nu există evaluări

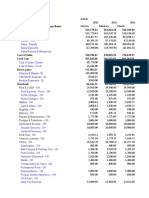

- Case Study Project Income Statement BudgetingDocument186 paginiCase Study Project Income Statement BudgetingKate ChuaÎncă nu există evaluări

- Audit Planning NotesDocument30 paginiAudit Planning NotesTinoManhangaÎncă nu există evaluări

- Licensing ProceduresDocument37 paginiLicensing ProceduresDlamini SiceloÎncă nu există evaluări

- 2 MODUL LogisticsDocument4 pagini2 MODUL LogisticsGiska AdeliaÎncă nu există evaluări

- Chapter 1Document4 paginiChapter 1sadsadsa100% (1)

- RN Profile Foco 2022Document16 paginiRN Profile Foco 2022MANINDER SINGHÎncă nu există evaluări

- Implementing Strategies. Management and Operation IssuesDocument41 paginiImplementing Strategies. Management and Operation IssuesM Owais FaizÎncă nu există evaluări

- Case Study #4:: Defining Standard Projects at Global Green Books PublishingDocument3 paginiCase Study #4:: Defining Standard Projects at Global Green Books PublishingHarsha ReddyÎncă nu există evaluări

- IT OS Part 5Document4 paginiIT OS Part 5Business RecoveryÎncă nu există evaluări

- Istaimy PLC: Chapter 26 Business PurchaseDocument3 paginiIstaimy PLC: Chapter 26 Business PurchaseSir YusufiÎncă nu există evaluări

- Buffer Profile and Buffer Level Determination For Demand Driven MRPDocument3 paginiBuffer Profile and Buffer Level Determination For Demand Driven MRPPrerak GargÎncă nu există evaluări

- AdvertisingDocument35 paginiAdvertisingcrazydubaiÎncă nu există evaluări

- Sebi Guidlines For BuybackDocument46 paginiSebi Guidlines For Buybacksonali bhosaleÎncă nu există evaluări

- How The Johnson and Johnson Brand Does Has Positioned Itself in ConsumerDocument4 paginiHow The Johnson and Johnson Brand Does Has Positioned Itself in ConsumerAreej Choudhry 5348-FMS/BBA/F18Încă nu există evaluări

- Customs Law and ProceduresDocument12 paginiCustoms Law and ProceduresSunilkumar Sunil KumarÎncă nu există evaluări

- Lesson 4-7Document79 paginiLesson 4-7marivic franciscoÎncă nu există evaluări

- Financial Accounting IFRS 3rd Edition Weygandt Solutions Manual DownloadDocument107 paginiFinancial Accounting IFRS 3rd Edition Weygandt Solutions Manual DownloadLigia Jackson100% (25)

- Chapter FiveDocument14 paginiChapter Fivemubarek oumerÎncă nu există evaluări

- Mark LK TW Iii 2019Document60 paginiMark LK TW Iii 2019RafliSitepuÎncă nu există evaluări

- Chapter Two: Company and Marketing Strategy Partnering To Build Customer RelationshipsDocument44 paginiChapter Two: Company and Marketing Strategy Partnering To Build Customer RelationshipsKrisKettyÎncă nu există evaluări

- AFM Important QuestionsDocument2 paginiAFM Important Questionsuma selvarajÎncă nu există evaluări

- Financial Markets and Institutions: 13 EditionDocument35 paginiFinancial Markets and Institutions: 13 EditionTherese Grace PostreroÎncă nu există evaluări

- Perbandingan Metode Eoq Economic Order Q Dan JitDocument19 paginiPerbandingan Metode Eoq Economic Order Q Dan JitAgung AndriantoÎncă nu există evaluări