S-ar putea să vă placă și

- AUC-Egyptian Electricity Market - March-24-2014-10 AmDocument45 paginiAUC-Egyptian Electricity Market - March-24-2014-10 AmAsmaa IbrahimÎncă nu există evaluări

- Module 8 - WESM RulesDocument29 paginiModule 8 - WESM RulesPao CastillonÎncă nu există evaluări

- Power Tariff Structure in Thailand PDFDocument21 paginiPower Tariff Structure in Thailand PDFMurali DarenÎncă nu există evaluări

- Overview of National Grid's Balancing Services: Lilian Macleod, Strategy and Policy, Market Operation, National GridDocument9 paginiOverview of National Grid's Balancing Services: Lilian Macleod, Strategy and Policy, Market Operation, National GridroyclhorÎncă nu există evaluări

- CREM June 2020Document9 paginiCREM June 2020kamijou08Încă nu există evaluări

- Developing Microgrids in the Philippines: Key Challenges from Meralco's ExperienceDocument34 paginiDeveloping Microgrids in the Philippines: Key Challenges from Meralco's ExperienceAnabeth Tuazon SuancoÎncă nu există evaluări

- Crem Report For April 2022Document12 paginiCrem Report For April 2022elsanpedroiiÎncă nu există evaluări

- Iloilo Energy 101 05 Power 101Document27 paginiIloilo Energy 101 05 Power 101allanÎncă nu există evaluări

- Crem April 2020Document8 paginiCrem April 2020kamijou08Încă nu există evaluări

- ETI Energy Snapshot Guyana - FY20Document2 paginiETI Energy Snapshot Guyana - FY20Rocky HanomanÎncă nu există evaluări

- Pidsdps 1221Document24 paginiPidsdps 1221ASP-MHEN APLAKÎncă nu există evaluări

- Philippine electricity demand grows 10% in 2016Document14 paginiPhilippine electricity demand grows 10% in 2016Alexis CabigtingÎncă nu există evaluări

- Crem May 2020Document9 paginiCrem May 2020kamijou08Încă nu există evaluări

- Crem September 2020Document11 paginiCrem September 2020kamijou08Încă nu există evaluări

- ETI Energy Snapshot Dominican Republic - FY20Document2 paginiETI Energy Snapshot Dominican Republic - FY20Ismael YahmiÎncă nu există evaluări

- Contestable Customers (In CREM) 1,478 4,015.75Document9 paginiContestable Customers (In CREM) 1,478 4,015.75kamijou08Încă nu există evaluări

- Smart Grids Forum 2016 Presentation Heiko StaubitzDocument34 paginiSmart Grids Forum 2016 Presentation Heiko StaubitzbamiehappieÎncă nu există evaluări

- Retail Market Monitoring Report For Q1 2022Document10 paginiRetail Market Monitoring Report For Q1 2022elsanpedroiiÎncă nu există evaluări

- Propedeutico C1 PDFDocument50 paginiPropedeutico C1 PDFDani VelaÎncă nu există evaluări

- ASCE 48-11 Design of Steel Transmission Pole StructuresDocument55 paginiASCE 48-11 Design of Steel Transmission Pole StructuresJCuchapin0% (4)

- C5 109 2014 PDFDocument8 paginiC5 109 2014 PDFRazvan DonciuÎncă nu există evaluări

- The Role of GOvernment To Develop Solar Energy Industry in Indonesia - Ministry of IndustryDocument18 paginiThe Role of GOvernment To Develop Solar Energy Industry in Indonesia - Ministry of IndustryBambangÎncă nu există evaluări

- Everything You Need to Know About Your New Job InductionDocument23 paginiEverything You Need to Know About Your New Job InductionMutwiri Kaaria John100% (1)

- Crem July 2020Document9 paginiCrem July 2020kamijou08Încă nu există evaluări

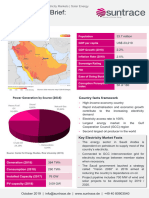

- Market_Brief_Saudi_ArabiaDocument4 paginiMarket_Brief_Saudi_ArabiaregallydivineÎncă nu există evaluări

- Green Energy Option Program ExplainedDocument22 paginiGreen Energy Option Program ExplainedCarlota VillaromanÎncă nu există evaluări

- Ies Mke Vietnam Power Sector Vision Part 2 2 PDFDocument171 paginiIes Mke Vietnam Power Sector Vision Part 2 2 PDFFan JeryÎncă nu există evaluări

- Power Sector OverviewDocument19 paginiPower Sector Overviewsaqib57Încă nu există evaluări

- Implementation of The Solar Hybrid System in A Micro-Grid SettingDocument20 paginiImplementation of The Solar Hybrid System in A Micro-Grid SettingSun TzuÎncă nu există evaluări

- Understanding The Energy Supply Chain (April 24 Baguio E-Power)Document28 paginiUnderstanding The Energy Supply Chain (April 24 Baguio E-Power)Juan IstilÎncă nu există evaluări

- Current and Emerging Challenges in PJM Energy Market: Zhenyu Fan, Tim Horger and Jeff BastianDocument7 paginiCurrent and Emerging Challenges in PJM Energy Market: Zhenyu Fan, Tim Horger and Jeff BastianlisusedÎncă nu există evaluări

- Flexible Operation NTPC'S Approach: Presented by A.K.Sinha, NTPC LTD, IndiaDocument18 paginiFlexible Operation NTPC'S Approach: Presented by A.K.Sinha, NTPC LTD, Indiamag_ktps20021520Încă nu există evaluări

- ACCURA 3700: High Accuracy Digital Power Quality MeterDocument16 paginiACCURA 3700: High Accuracy Digital Power Quality MeterLong Luong VanÎncă nu există evaluări

- Statistics in The Crem As of October 2020Document11 paginiStatistics in The Crem As of October 2020kamijou08Încă nu există evaluări

- Crem Report For November 2020Document11 paginiCrem Report For November 2020kamijou08Încă nu există evaluări

- Infrastructure PDF 2022Document22 paginiInfrastructure PDF 2022Juan Nicolás BarretoÎncă nu există evaluări

- 2 - Updates On The Energy Regulatory Framework - ERCDocument24 pagini2 - Updates On The Energy Regulatory Framework - ERCMarce MangaoangÎncă nu există evaluări

- Power 101Document29 paginiPower 101Mobile LegendsÎncă nu există evaluări

- 1-1slide K SUCHADA-hydroDocument61 pagini1-1slide K SUCHADA-hydroPae RangsanÎncă nu există evaluări

- 0 Se4all Aa Ip Zambia Presentation Beijing China FinalDocument17 pagini0 Se4all Aa Ip Zambia Presentation Beijing China FinalMehedi HasanÎncă nu există evaluări

- GUBBI Project Distribution & End-Use Efficiency ImprovementsDocument27 paginiGUBBI Project Distribution & End-Use Efficiency Improvementsgaurang1111Încă nu există evaluări

- Energy Snapshot: American SamoaDocument4 paginiEnergy Snapshot: American SamoaSr. RZÎncă nu există evaluări

- KEPCODocument27 paginiKEPCOToVanÎncă nu există evaluări

- Transmission PlanningDocument28 paginiTransmission PlanningLauren M. OlivosÎncă nu există evaluări

- 7.1. Opportunities For Scaling Up Wind Power in The Philippines by F. SibayanDocument10 pagini7.1. Opportunities For Scaling Up Wind Power in The Philippines by F. Sibayanquantum_leap_windÎncă nu există evaluări

- Presentation Independent Energy PoolDocument13 paginiPresentation Independent Energy PoolGuy RiceÎncă nu există evaluări

- Electric Power Industry Reform Act (Epira)Document13 paginiElectric Power Industry Reform Act (Epira)Michael DarmstaedterÎncă nu există evaluări

- Understanding the Unbundled Electric BillDocument29 paginiUnderstanding the Unbundled Electric BillMiko GorospeÎncă nu există evaluări

- E I B C R O: Nergy Nvestment and Usiness Limate Eport For Bserver CountriesDocument54 paginiE I B C R O: Nergy Nvestment and Usiness Limate Eport For Bserver CountriesAbdurabu AL-MontaserÎncă nu există evaluări

- Status of Myanmar Electric Power and Hydropower PlanningDocument18 paginiStatus of Myanmar Electric Power and Hydropower PlanningTHAN HANÎncă nu există evaluări

- Policy Notes On EpiraDocument8 paginiPolicy Notes On EpiraAngeline De GuzmanÎncă nu există evaluări

- Bec BagalkotDocument57 paginiBec BagalkotharishÎncă nu există evaluări

- Distributed Generation & Renewable Energy Technologies: by Mohammed ADocument31 paginiDistributed Generation & Renewable Energy Technologies: by Mohammed Ahabte gebreial shrashrÎncă nu există evaluări

- Empowering State Governments A New Era of State Participation in The Nigerian Electricity Sector - EMRCDocument70 paginiEmpowering State Governments A New Era of State Participation in The Nigerian Electricity Sector - EMRCEdward ObokohÎncă nu există evaluări

- (E4) IndonesiaDocument36 pagini(E4) IndonesiaKarlinaÎncă nu există evaluări

- Thailand Electric Power SystemDocument23 paginiThailand Electric Power SystemThomas OrÎncă nu există evaluări

- SIRIM - Overview of PV Industry Rev 1kks by SEDADocument34 paginiSIRIM - Overview of PV Industry Rev 1kks by SEDAIrwan OmarÎncă nu există evaluări

- Wireless Communications Design Handbook: Space Interference: Aspects of Noise, Interference and Environmental ConcernsDe la EverandWireless Communications Design Handbook: Space Interference: Aspects of Noise, Interference and Environmental ConcernsEvaluare: 5 din 5 stele5/5 (1)

- Environmental Impact of Energy Strategies Within the EEC: A Report Prepared for the Environment and Consumer Protection, Service of the Commission of the European CommunitiesDe la EverandEnvironmental Impact of Energy Strategies Within the EEC: A Report Prepared for the Environment and Consumer Protection, Service of the Commission of the European CommunitiesÎncă nu există evaluări

- Tajikistan's Winter Energy Crisis: Electricity Supply and Demand AlternativesDe la EverandTajikistan's Winter Energy Crisis: Electricity Supply and Demand AlternativesÎncă nu există evaluări

- Cybersecurity Policy FrameworkDocument44 paginiCybersecurity Policy FrameworkAhmed100% (1)

- Cybersecurity Framework Version 1.1 OverviewDocument12 paginiCybersecurity Framework Version 1.1 OverviewLlauca XavierÎncă nu există evaluări

- Nutanix: NCP-MCI-5.15 ExamDocument7 paginiNutanix: NCP-MCI-5.15 ExamAlvin BosqueÎncă nu există evaluări

- FMD-F-11-02.14.4 Work Permit Hot Work PermitDocument2 paginiFMD-F-11-02.14.4 Work Permit Hot Work PermitAlvin Bosque50% (2)

- Framework For Improving Critical Infrastructure CybersecurityDocument55 paginiFramework For Improving Critical Infrastructure CybersecurityTanat TonguthaisriÎncă nu există evaluări

- Summary of Cost Estimates Per End Users - OCB OPI O6-Dawn Raid Toolkits and Other Tools For InvestigationDocument11 paginiSummary of Cost Estimates Per End Users - OCB OPI O6-Dawn Raid Toolkits and Other Tools For InvestigationAlvin BosqueÎncă nu există evaluări

- KB 4 D Marc Slides 1626293010926Document91 paginiKB 4 D Marc Slides 1626293010926Alvin BosqueÎncă nu există evaluări

- PCC Shuttle Schedule and Driver Details for July 2021Document1 paginăPCC Shuttle Schedule and Driver Details for July 2021Alvin BosqueÎncă nu există evaluări

- DRAFT PR - OCB OPI O6-Dawn Raid Toolkits and Other Tools For InvestigationDocument5 paginiDRAFT PR - OCB OPI O6-Dawn Raid Toolkits and Other Tools For InvestigationAlvin BosqueÎncă nu există evaluări

- Cybersecurity Policy FrameworkDocument44 paginiCybersecurity Policy FrameworkAhmed100% (1)

- DRAFT PPMP - OCB OPI O6-Dawn Raid Toolkits and Other Tools For InvestigationDocument6 paginiDRAFT PPMP - OCB OPI O6-Dawn Raid Toolkits and Other Tools For InvestigationAlvin BosqueÎncă nu există evaluări

- 1.2.1.3 Lab - Compare Data With A HashDocument4 pagini1.2.1.3 Lab - Compare Data With A HashAsad MahmoodÎncă nu există evaluări

- Transportation Research Part EDocument15 paginiTransportation Research Part EAlvin BosqueÎncă nu există evaluări

- Annual Market Assessment Report: Philippine Electricity Market CorporationDocument97 paginiAnnual Market Assessment Report: Philippine Electricity Market CorporationAlvin BosqueÎncă nu există evaluări

- Knowledge Is Your Best Defense.: Cybercriminals YOUDocument1 paginăKnowledge Is Your Best Defense.: Cybercriminals YOUAlvin BosqueÎncă nu există evaluări

- 10 Tips Recognize and Prevent Insider Threats PDFDocument1 pagină10 Tips Recognize and Prevent Insider Threats PDFAlvin BosqueÎncă nu există evaluări

- 1.2.1.3 Lab - Compare Data With A HashDocument4 pagini1.2.1.3 Lab - Compare Data With A HashAsad MahmoodÎncă nu există evaluări

- 10 Tips For Physical SecurityDocument1 pagină10 Tips For Physical SecurityAlvin BosqueÎncă nu există evaluări

- 1.2.1.3 Lab - Compare Data With A HashDocument4 pagini1.2.1.3 Lab - Compare Data With A HashAsad MahmoodÎncă nu există evaluări

- Mallcom - Annual - Report - 2020-21.pdf (2020-2021)Document144 paginiMallcom - Annual - Report - 2020-21.pdf (2020-2021)abhishekÎncă nu există evaluări

- Affidavit Declaring Consent To RevocationDocument5 paginiAffidavit Declaring Consent To RevocationcvilleweeklyÎncă nu există evaluări

- Air and Space LawDocument6 paginiAir and Space LawANJALI RAJ100% (1)

- SC Rules Grace Poe Qualified for PresidencyDocument3 paginiSC Rules Grace Poe Qualified for PresidencyJae LeeÎncă nu există evaluări

- Orlando FreeFall Ride LawuitDocument65 paginiOrlando FreeFall Ride LawuitWFTVÎncă nu există evaluări

- Application Under Section 144 of The Code of Civil Procedure Application For Restitution of PropertyDocument5 paginiApplication Under Section 144 of The Code of Civil Procedure Application For Restitution of Propertyvishalfunckyman100% (2)

- Rizal's Love for His Country Amid Spain's Decadent Colonial Rule in the PhilippinesDocument6 paginiRizal's Love for His Country Amid Spain's Decadent Colonial Rule in the PhilippinesJuna Grace GetuabanÎncă nu există evaluări

- Module 1Document13 paginiModule 1MARITES M. CUYOSÎncă nu există evaluări

- CA-141 Public Land Act ClassificationDocument5 paginiCA-141 Public Land Act ClassificationJULIUS MIRALOÎncă nu există evaluări

- O. Henry Power PointDocument11 paginiO. Henry Power PointGülruÎncă nu există evaluări

- Ar 341 343d - Major Plate No.1 - 20x30Document2 paginiAr 341 343d - Major Plate No.1 - 20x30Ge HalasanÎncă nu există evaluări

- Philippine Council for NGO Certification History StandardsDocument26 paginiPhilippine Council for NGO Certification History StandardsDarlyn EtangÎncă nu există evaluări

- Atty Uribe Lecture Notes on Credit TransactionsDocument11 paginiAtty Uribe Lecture Notes on Credit TransactionsResin BagnetteÎncă nu există evaluări

- History Research Project: The Life of A Democratic Leader Nelson Mandela's Long Walk To Freedom Composed by Tristan Chetty Grade 6SDocument7 paginiHistory Research Project: The Life of A Democratic Leader Nelson Mandela's Long Walk To Freedom Composed by Tristan Chetty Grade 6SDanielle Chetty100% (2)

- Legal Studies 125 Course on Human Rights InvestigationsDocument9 paginiLegal Studies 125 Course on Human Rights InvestigationsMel BrittÎncă nu există evaluări

- Purchase Order for Flexible CableDocument2 paginiPurchase Order for Flexible Cableresful islamÎncă nu există evaluări

- Behind The LieDocument28 paginiBehind The LieARIHAN SHARMAÎncă nu există evaluări

- Case Title: Topic: DoctrineDocument3 paginiCase Title: Topic: DoctrineDaniela SandraÎncă nu există evaluări

- Form 3301-General Information (Application/Renewal For License To Use Texas State Seal)Document3 paginiForm 3301-General Information (Application/Renewal For License To Use Texas State Seal)DoirÎncă nu există evaluări

- Rights and Privileges of PDLDocument30 paginiRights and Privileges of PDLDigos City District JailÎncă nu există evaluări

- Neruda, Jan - VampireDocument3 paginiNeruda, Jan - VampireRicky Leonard PereiraÎncă nu există evaluări

- Shuwakitha ChandrasekaranDocument10 paginiShuwakitha ChandrasekaranVeena Kulkarni DalaviÎncă nu există evaluări

- IFoA congratulates qualifiers for new designationsDocument1 paginăIFoA congratulates qualifiers for new designationsantiqurrÎncă nu există evaluări

- Romeo P. Busuego, Catalino F. Banez and Renato F. Lim, Petitioners, vs. The Honorable Court of Appeals and The Monetary Board of The CentralDocument1 paginăRomeo P. Busuego, Catalino F. Banez and Renato F. Lim, Petitioners, vs. The Honorable Court of Appeals and The Monetary Board of The CentralchaÎncă nu există evaluări

- CC Unit 5, TransportationDocument30 paginiCC Unit 5, TransportationAzure NguyenÎncă nu există evaluări

- Law On SuccessionDocument46 paginiLaw On SuccessionIris FenelleÎncă nu există evaluări

- Secretary of Labor Has Jurisdiction to Cancel Private Employment Agency LicenseDocument4 paginiSecretary of Labor Has Jurisdiction to Cancel Private Employment Agency LicenseZachary Philipp LimÎncă nu există evaluări

- Edwards Lifesciences LLC v. Medtronic Corevalve LLC, C.A. No. 12-23-GMS (D. Del. Dec. 27, 2013)Document6 paginiEdwards Lifesciences LLC v. Medtronic Corevalve LLC, C.A. No. 12-23-GMS (D. Del. Dec. 27, 2013)gbrodzik7533Încă nu există evaluări

- Montalban v. MaximoDocument1 paginăMontalban v. MaximoReymart-Vin Maguliano100% (1)

- Centrifuga Sharples AE 16 PDFDocument35 paginiCentrifuga Sharples AE 16 PDFMARCO VERAMENDIÎncă nu există evaluări