S-ar putea să vă placă și

- Ia 2Document2 paginiIa 2Nadine SofiaÎncă nu există evaluări

- Proof of Cash FormatDocument7 paginiProof of Cash FormatnathanlagdamenÎncă nu există evaluări

- Bank Reconciliation ProblemsDocument2 paginiBank Reconciliation ProblemsCris Jung80% (5)

- Proof of Cash Illustrative Example - DiscussionDocument11 paginiProof of Cash Illustrative Example - DiscussionAdyangÎncă nu există evaluări

- Quiz 2B - Bank Reconciliation and Proof of CashDocument5 paginiQuiz 2B - Bank Reconciliation and Proof of CashLorence Ibañez100% (2)

- Proof of Cash Baht CompanyDocument6 paginiProof of Cash Baht CompanyCJ alandy100% (1)

- Proof of Cash Problems 4 PDF FreeDocument9 paginiProof of Cash Problems 4 PDF FreeAngieÎncă nu există evaluări

- Long Examination Cash Set ADocument3 paginiLong Examination Cash Set AprechuteÎncă nu există evaluări

- Impairment of Loans and Receivable FinancingDocument17 paginiImpairment of Loans and Receivable FinancingGelyn CruzÎncă nu există evaluări

- Seatwork 2B ASSIGNDocument5 paginiSeatwork 2B ASSIGNYzzabel Denise L. Tolentino100% (1)

- Sample Auditing Problems (Proof of Cash and Correction of Error) With SolutionDocument16 paginiSample Auditing Problems (Proof of Cash and Correction of Error) With SolutionFernan Dvra100% (1)

- Cash & Cash EquivalentsDocument4 paginiCash & Cash EquivalentsXienaÎncă nu există evaluări

- Proof of Cash-1Document7 paginiProof of Cash-1Ella MalitÎncă nu există evaluări

- RECEIVABLESDocument28 paginiRECEIVABLESClarice Ilustre Guintibano100% (1)

- Bank Recon Solutions Exercise 2 3Document7 paginiBank Recon Solutions Exercise 2 3Kevin James Sedurifa OledanÎncă nu există evaluări

- The Correct Answer Is: P105,000Document5 paginiThe Correct Answer Is: P105,000cindy100% (2)

- Proof of Cash ProblemDocument4 paginiProof of Cash ProblemHtiduj Oretubag50% (4)

- Chapter 16Document12 paginiChapter 16WesÎncă nu există evaluări

- Chapter 11 Answers RepportDocument12 paginiChapter 11 Answers RepportJudy56% (16)

- Problem 1Document3 paginiProblem 1Zyrah Manalo50% (2)

- Cash Shortage Computation: SolutionDocument4 paginiCash Shortage Computation: SolutionCJ alandyÎncă nu există evaluări

- TRAPO, Inc. Estimates Its Bad Debt Losses by Aging Its Accounts Receivable. The Aging Schedule ofDocument2 paginiTRAPO, Inc. Estimates Its Bad Debt Losses by Aging Its Accounts Receivable. The Aging Schedule ofAlvinDumanggasÎncă nu există evaluări

- Trade and Other Receivables 1. On December 31, 2013, The Accounts Receivable of Harem Company Had A Balance ofDocument11 paginiTrade and Other Receivables 1. On December 31, 2013, The Accounts Receivable of Harem Company Had A Balance ofJude SantosÎncă nu există evaluări

- Practical Accounting 1Document14 paginiPractical Accounting 1Anonymous Lih1laaxÎncă nu există evaluări

- Reviewer - Cash & Cash EquivalentsDocument5 paginiReviewer - Cash & Cash EquivalentsMaria Kathreena Andrea Adeva100% (1)

- Proof of CashDocument7 paginiProof of CashPeachy80% (5)

- FinAct ARDocument15 paginiFinAct ARnanaÎncă nu există evaluări

- Nissan FinalDocument4 paginiNissan FinalPrince Jayanmar BerbaÎncă nu există evaluări

- Cash and Cash Equivalents Basic ProblemsDocument6 paginiCash and Cash Equivalents Basic ProblemshellokittysaranghaeÎncă nu există evaluări

- 1 Far Answer KeyDocument25 pagini1 Far Answer KeyAngelie0% (1)

- Audit Prob - ReceivablesDocument27 paginiAudit Prob - ReceivablesCharis Marie Urgel100% (3)

- Proof of CashDocument2 paginiProof of CashAiden Pats80% (5)

- SolutionDocument5 paginiSolutionClariz Angelika EscocioÎncă nu există evaluări

- This Study Resource Was: 17 Proof of CashDocument6 paginiThis Study Resource Was: 17 Proof of CashXÎncă nu există evaluări

- Petty Cash FundDocument23 paginiPetty Cash FundAnnie RapanutÎncă nu există evaluări

- Auditing Report CASE11Document18 paginiAuditing Report CASE11Coke Aidenry Saludo0% (1)

- This Study Resource Was: Chapter 18: Accounts ReceivableDocument7 paginiThis Study Resource Was: Chapter 18: Accounts ReceivableXENA LOPEZÎncă nu există evaluări

- MTDrill 2Document17 paginiMTDrill 2Cedric Legaspi TagalaÎncă nu există evaluări

- Assessment Test 2nd Cash&RecDocument6 paginiAssessment Test 2nd Cash&RecMellowÎncă nu există evaluări

- Proof of Cash ProblemsDocument2 paginiProof of Cash ProblemsSamantha Marie Arevalo100% (1)

- Auditing ProblemsDocument37 paginiAuditing ProblemsDonna Mae HernandezÎncă nu există evaluări

- Quiz 5Document7 paginiQuiz 5Arjay CarolinoÎncă nu există evaluări

- Exercises 1Document9 paginiExercises 1Anonymous QWaWnuMÎncă nu există evaluări

- Problem 1Document4 paginiProblem 1redassdawnÎncă nu există evaluări

- Cash Cash EquivalentsDocument11 paginiCash Cash EquivalentsGiulia TabaraÎncă nu există evaluări

- Gross Profit Variation Analysis: For Multiple ProductsDocument12 paginiGross Profit Variation Analysis: For Multiple ProductsJoey WassigÎncă nu există evaluări

- Bank Reconciliation - Sample ProblemDocument2 paginiBank Reconciliation - Sample ProblemKarl Wilson GonzalesÎncă nu există evaluări

- Proof of Cash: By: LailaneDocument19 paginiProof of Cash: By: LailaneGianJoshuaDayrit100% (1)

- FAR Practical Exercises Proof of CashDocument3 paginiFAR Practical Exercises Proof of CashAB CloydÎncă nu există evaluări

- Bsa 7Document2 paginiBsa 7Gray JavierÎncă nu există evaluări

- 1Document8 pagini1Cindy CrausÎncă nu există evaluări

- Inventory ReviewerDocument7 paginiInventory ReviewerPau Santos100% (5)

- Two-Date Bank ReconDocument5 paginiTwo-Date Bank Reconrhiz cyrelle calanoÎncă nu există evaluări

- Proof of Cash Adjusted Balance Method: Labels 31-Jan Receipts Disbursements 28-FebDocument4 paginiProof of Cash Adjusted Balance Method: Labels 31-Jan Receipts Disbursements 28-FebNika BautistaÎncă nu există evaluări

- Proof of CashDocument25 paginiProof of CashSoria Sophia AnnÎncă nu există evaluări

- Cash Problems SolutionDocument3 paginiCash Problems SolutionMagadia Mark JeffÎncă nu există evaluări

- Assignment 1.3 Proof of CashDocument16 paginiAssignment 1.3 Proof of CashRya Miguel AlbaÎncă nu există evaluări

- C3Document16 paginiC3Aaliyah Manuel100% (1)

- AP Computation - Cash and Cash EquivalentsDocument16 paginiAP Computation - Cash and Cash EquivalentsErnest Andales0% (1)

- Proof of Cash ProblemDocument3 paginiProof of Cash ProblemKathleen Frondozo67% (6)

- QuestionnaireDocument4 paginiQuestionnaireTroisÎncă nu există evaluări

- Auditing: Page 1 of 8Document8 paginiAuditing: Page 1 of 8jeams vidalÎncă nu există evaluări

- A Review in Managerial Economics: Prepared By: Jeams E. VidalDocument8 paginiA Review in Managerial Economics: Prepared By: Jeams E. Vidaljeams vidalÎncă nu există evaluări

- Introduction To AisDocument41 paginiIntroduction To AisMarieJoiaÎncă nu există evaluări

- PayrollcontrolsDocument2 paginiPayrollcontrolsjeams vidalÎncă nu există evaluări

- AP Ppe Quizzer QDocument28 paginiAP Ppe Quizzer Qkimberly bumanlagÎncă nu există evaluări

- Internal Audit Manual PhilippinesDocument295 paginiInternal Audit Manual PhilippinesAnonymous dtceNuyIFI100% (8)

- Final Visit Inventory AuditDocument7 paginiFinal Visit Inventory Auditjeams vidalÎncă nu există evaluări

- Seth Harvey Hendeve IPPPE ME QuizDocument4 paginiSeth Harvey Hendeve IPPPE ME Quizjeams vidalÎncă nu există evaluări

- Internal Control - Accounts Receivable and Credit SalesDocument4 paginiInternal Control - Accounts Receivable and Credit Salesjeams vidalÎncă nu există evaluări

- Interim Visit 2Document2 paginiInterim Visit 2jeams vidalÎncă nu există evaluări

- 2015 Senior Thesis TopicsDocument12 pagini2015 Senior Thesis TopicspamelaÎncă nu există evaluări

- Richly Roboca IPPPE ME QuizDocument4 paginiRichly Roboca IPPPE ME Quizjeams vidalÎncă nu există evaluări

- Materiality LevelDocument1 paginăMateriality Leveljeams vidalÎncă nu există evaluări

- Bank Reconciliation: Irene Mae C. Guerra, CPADocument25 paginiBank Reconciliation: Irene Mae C. Guerra, CPAjeams vidalÎncă nu există evaluări

- What Is A Cash Flow StatementDocument3 paginiWhat Is A Cash Flow Statementjeams vidalÎncă nu există evaluări

- An Analysis of Basic Accounting Practices of MicroenterprisesDocument10 paginiAn Analysis of Basic Accounting Practices of Microenterprisesjeams vidalÎncă nu există evaluări

- IMPREST Vs FLUCTUATINGDocument2 paginiIMPREST Vs FLUCTUATINGjeams vidalÎncă nu există evaluări

- A Review in Managerial Economics: Prepared By: Jeams E. VidalDocument8 paginiA Review in Managerial Economics: Prepared By: Jeams E. Vidaljeams vidalÎncă nu există evaluări

- IMPREST Vs FLUCTUATINGDocument2 paginiIMPREST Vs FLUCTUATINGjeams vidalÎncă nu există evaluări

- Chapter Three: Product Costing and Cost Accumulation in A Batch Production EnvironmentDocument71 paginiChapter Three: Product Costing and Cost Accumulation in A Batch Production Environmentjeams vidalÎncă nu există evaluări

- 4 - Accounting For OverheadDocument12 pagini4 - Accounting For Overheadjeams vidalÎncă nu există evaluări

- Determinants of Accounting Practices Among Street Food VendorsDocument15 paginiDeterminants of Accounting Practices Among Street Food VendorsShamae AfableÎncă nu există evaluări

- A Review in Managerial Economics: Prepared By: Jeams E. VidalDocument8 paginiA Review in Managerial Economics: Prepared By: Jeams E. Vidaljeams vidalÎncă nu există evaluări

- Conceptual Framework: (Underlying Assumptions and Qualitative CharacteristicsDocument25 paginiConceptual Framework: (Underlying Assumptions and Qualitative Characteristicsjeams vidalÎncă nu există evaluări

- Cost Accounting & Control: (Introduction and OverviewDocument16 paginiCost Accounting & Control: (Introduction and Overviewjeams vidalÎncă nu există evaluări

- Assignment: Multimedia Keyboards Comfort Type KeyboardsDocument1 paginăAssignment: Multimedia Keyboards Comfort Type Keyboardsjeams vidal0% (2)

- Basic Accountin-WPS OfficeDocument4 paginiBasic Accountin-WPS Officejeams vidalÎncă nu există evaluări

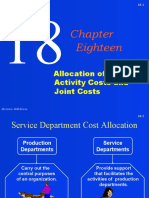

- Eighteen: Allocation of Support Activity Costs and Joint CostsDocument67 paginiEighteen: Allocation of Support Activity Costs and Joint Costsjeams vidalÎncă nu există evaluări

- Tez PortalDocument1 paginăTez Portalkiran BawadkarÎncă nu există evaluări

- Articles of Partnership ExampleDocument4 paginiArticles of Partnership ExamplePiaMarielVillafloresÎncă nu există evaluări

- PT Rea Kaltim Plantations PDFDocument4 paginiPT Rea Kaltim Plantations PDFAnggah KhanÎncă nu există evaluări

- Black Book PDFDocument69 paginiBlack Book PDFManjodh Singh BassiÎncă nu există evaluări

- TOGAF An Open Group Standard and Enterprise Architecture RequirementsDocument17 paginiTOGAF An Open Group Standard and Enterprise Architecture RequirementssilvestreolÎncă nu există evaluări

- The Input Tools Require Strategists To Quantify Subjectivity During Early Stages of The Strategy-Formulation ProcessDocument24 paginiThe Input Tools Require Strategists To Quantify Subjectivity During Early Stages of The Strategy-Formulation ProcessHannah Ruth M. GarpaÎncă nu există evaluări

- Aqua Health PDFDocument1 paginăAqua Health PDFJoseph Gavier M. FrancoÎncă nu există evaluări

- Din 11864 / Din 11853: Armaturenwerk Hötensleben GMBHDocument70 paginiDin 11864 / Din 11853: Armaturenwerk Hötensleben GMBHkrisÎncă nu există evaluări

- Six Sigma Black Belt Wk1 Define Amp MeasureDocument451 paginiSix Sigma Black Belt Wk1 Define Amp Measuremajid4uonly100% (1)

- Management Theory and Practice - Chapter 1 - Session 1 PPT Dwtv9Ymol5Document35 paginiManagement Theory and Practice - Chapter 1 - Session 1 PPT Dwtv9Ymol5DHAVAL ABDAGIRI83% (6)

- Critically Discuss The Extent of Directors Duties and The Changes Made by The Companies Act 2006Document14 paginiCritically Discuss The Extent of Directors Duties and The Changes Made by The Companies Act 2006Lingru WenÎncă nu există evaluări

- Sample Club BudgetsDocument8 paginiSample Club BudgetsDona KaitemÎncă nu există evaluări

- Business CombinationDocument20 paginiBusiness CombinationabhaybittuÎncă nu există evaluări

- Ifrs 5Document2 paginiIfrs 5Foititika.netÎncă nu există evaluări

- 782 Sap SD Credit or Risk ManagementDocument12 pagini782 Sap SD Credit or Risk Managementrohit sharmaÎncă nu există evaluări

- Advanced Competitive Position AssignmentDocument7 paginiAdvanced Competitive Position AssignmentGeraldine Aguilar100% (1)

- Save Capitalism From CapitalistsDocument20 paginiSave Capitalism From CapitalistsLill GalilÎncă nu există evaluări

- Anastasia Chandra - .Akuntanis A 2014 - Tugas 6xDocument21 paginiAnastasia Chandra - .Akuntanis A 2014 - Tugas 6xSriÎncă nu există evaluări

- Six Sigma Control PDFDocument74 paginiSix Sigma Control PDFnaacha457Încă nu există evaluări

- KULITDocument68 paginiKULITdennycaÎncă nu există evaluări

- Consumer Behavior Assignment: Stimulus GeneralizationDocument3 paginiConsumer Behavior Assignment: Stimulus GeneralizationSaurabh SumanÎncă nu există evaluări

- Argument On Workplace SafetyDocument2 paginiArgument On Workplace SafetyEeshan BhagwatÎncă nu există evaluări

- ch14 ExercisesDocument10 paginich14 ExercisesAriin TambunanÎncă nu există evaluări

- 1 Electrolux CaseDocument3 pagini1 Electrolux CaseAndreea Conoro0% (1)

- Economics and Finance Personal StatementDocument1 paginăEconomics and Finance Personal StatementNicolescu AdrianÎncă nu există evaluări

- ALKO Case StudyDocument13 paginiALKO Case StudyAnass MessaoudiÎncă nu există evaluări

- RDL1 - Activity 1.2Document1 paginăRDL1 - Activity 1.2EL FuentesÎncă nu există evaluări

- 51977069Document1 pagină51977069Beginner RanaÎncă nu există evaluări

- AideD&D n5 Basse-Tour (Suite Pour Un Diamant)Document7 paginiAideD&D n5 Basse-Tour (Suite Pour Un Diamant)Etan KrelÎncă nu există evaluări

- Sales SUALOGDocument21 paginiSales SUALOGEynab Perez100% (1)