S-ar putea să vă placă și

- Chapter Five: The Financial Statements of Banks and Their Principal CompetitorsDocument58 paginiChapter Five: The Financial Statements of Banks and Their Principal CompetitorsYoussef Youssef Ahmed Abdelmeguid Abdel LatifÎncă nu există evaluări

- Chapter 7Document53 paginiChapter 7Baby KhorÎncă nu există evaluări

- International FInanceDocument3 paginiInternational FInanceJemma JadeÎncă nu există evaluări

- Module IV - Working Capital ManagementDocument50 paginiModule IV - Working Capital ManagementAshwin DholeÎncă nu există evaluări

- Basel 3Document32 paginiBasel 3Venkat SaiÎncă nu există evaluări

- BM Introduction To BankingDocument36 paginiBM Introduction To BankingNatasha OliviaÎncă nu există evaluări

- Lecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015Document31 paginiLecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015studentÎncă nu există evaluări

- Cash Coversion CYcleDocument29 paginiCash Coversion CYcleZohaib HassanÎncă nu există evaluări

- Strategic Planning and Control True/False QuestionsDocument28 paginiStrategic Planning and Control True/False QuestionsReneeÎncă nu există evaluări

- Standard Costing and Variance Analysis: Fall 2007 CrossonDocument20 paginiStandard Costing and Variance Analysis: Fall 2007 CrossonBernard SalongaÎncă nu există evaluări

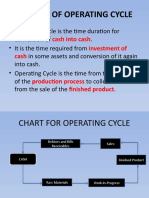

- Concept of Operating Cycle: Cash Into Cash Investment of CashDocument6 paginiConcept of Operating Cycle: Cash Into Cash Investment of CashVenket RamanaÎncă nu există evaluări

- 3.sales Variance AnalysisDocument38 pagini3.sales Variance Analysiskamasuke hegdeÎncă nu există evaluări

- Part Seven: THE Management of Financial InstitutionsDocument40 paginiPart Seven: THE Management of Financial InstitutionsIrakli SaliaÎncă nu există evaluări

- ACC51112 Balanced ScorecardDocument6 paginiACC51112 Balanced ScorecardjasÎncă nu există evaluări

- CH 8Document16 paginiCH 8emanmamdouh596Încă nu există evaluări

- Lecture 2: Exchange Rates and The Foreign Exchange Market: TopicsDocument79 paginiLecture 2: Exchange Rates and The Foreign Exchange Market: TopicsSalvio MachaÎncă nu există evaluări

- International Finance Lecture SlidesDocument27 paginiInternational Finance Lecture Slidesmaryam ashfaqÎncă nu există evaluări

- Cost ManagementDocument18 paginiCost ManagementGeo Rublico ManilaÎncă nu există evaluări

- Overhead VariancesDocument11 paginiOverhead VariancesDanica VillaganteÎncă nu există evaluări

- Duration GAP analysis: Measuring interest rate riskDocument5 paginiDuration GAP analysis: Measuring interest rate riskShubhash ShresthaÎncă nu există evaluări

- Wal-Mart's Balance Scorecard StrategyDocument13 paginiWal-Mart's Balance Scorecard StrategyMIRAL PATELÎncă nu există evaluări

- Foreign Exchange Markets, End of Chapter Solutions.Document27 paginiForeign Exchange Markets, End of Chapter Solutions.PankajatSIBMÎncă nu există evaluări

- Chapter10 Investment Function in BankDocument38 paginiChapter10 Investment Function in BankTừ Lê Lan HươngÎncă nu există evaluări

- 324 - International Parity ConditionsDocument49 pagini324 - International Parity ConditionsTamuna BibiluriÎncă nu există evaluări

- CVP Analysis Final 1Document92 paginiCVP Analysis Final 1Utsav ChoudhuryÎncă nu există evaluări

- PPT-4 Parity Conditions and Currency ForecastingDocument42 paginiPPT-4 Parity Conditions and Currency ForecastingKamal KantÎncă nu există evaluări

- B04 - Throughput AccountingDocument24 paginiB04 - Throughput AccountingAcca Books100% (1)

- Security Analysis: Chapter - 1Document47 paginiSecurity Analysis: Chapter - 1Harsh GuptaÎncă nu există evaluări

- Throughput Accounting-AccaDocument25 paginiThroughput Accounting-AccaDamalai YansanehÎncă nu există evaluări

- Variable Production Overhead Variance (VPOH)Document9 paginiVariable Production Overhead Variance (VPOH)Wee Han ChiangÎncă nu există evaluări

- Capital Structure: Overview of The Financing DecisionDocument68 paginiCapital Structure: Overview of The Financing DecisionHay JirenyaaÎncă nu există evaluări

- Answers To Chapter 7 - Interest Rates and Bond ValuationDocument8 paginiAnswers To Chapter 7 - Interest Rates and Bond ValuationbuwaleedÎncă nu există evaluări

- Portfolio Selection Using Sharpe, Treynor & Jensen Performance IndexDocument15 paginiPortfolio Selection Using Sharpe, Treynor & Jensen Performance Indexktkalai selviÎncă nu există evaluări

- Chapter 2 - The Business Plan Road Map To SuccessDocument52 paginiChapter 2 - The Business Plan Road Map To SuccessFanie SaphiraÎncă nu există evaluări

- Product Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingDocument23 paginiProduct Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingTapiwa Tbone MadamombeÎncă nu există evaluări

- Answers To End of Chapter Questions and Applications: 3. Imperfect MarketsDocument2 paginiAnswers To End of Chapter Questions and Applications: 3. Imperfect Marketssuhayb_1988Încă nu există evaluări

- Financial Derivatives: Prof. Scott JoslinDocument49 paginiFinancial Derivatives: Prof. Scott Joslinarnav100% (2)

- Financial Statement Analysis PPT 3427Document25 paginiFinancial Statement Analysis PPT 3427imroz_alamÎncă nu există evaluări

- Debt Funds SimplifiedDocument28 paginiDebt Funds SimplifiedPriyankaKadamÎncă nu există evaluări

- Flexible BudgetDocument30 paginiFlexible BudgetTebaterrorÎncă nu există evaluări

- Working Capital Practice SetDocument12 paginiWorking Capital Practice SetRyan Malanum AbrioÎncă nu există evaluări

- Definition, Nature & Scope of WCDocument12 paginiDefinition, Nature & Scope of WCAshish Gautam0% (1)

- Consolidated Financial StatementsDocument7 paginiConsolidated Financial StatementsParvez NahidÎncă nu există evaluări

- Balanced Scorecard and Benchmarking StrategiesDocument12 paginiBalanced Scorecard and Benchmarking StrategiesGaurav Sharma100% (1)

- A. B. C. D. E.: Capital Costs, Operating Costs, Revenue, Depreciation, and Residual ValueDocument30 paginiA. B. C. D. E.: Capital Costs, Operating Costs, Revenue, Depreciation, and Residual ValueAfroz AlamÎncă nu există evaluări

- Ias 2Document23 paginiIas 2Syed Salman Sajid100% (4)

- Calculate Cost of CapitalDocument21 paginiCalculate Cost of CapitalsachitÎncă nu există evaluări

- CA Inter FM-ECO Chapter 6 Key ConceptsDocument23 paginiCA Inter FM-ECO Chapter 6 Key ConceptsAejaz MohamedÎncă nu există evaluări

- Optimal production planning using linear programmingDocument10 paginiOptimal production planning using linear programmingYat Kunt ChanÎncă nu există evaluări

- Formulae Sheets: Ps It Orp S It 1 1Document3 paginiFormulae Sheets: Ps It Orp S It 1 1Mengdi ZhangÎncă nu există evaluări

- Makerere University College of Business and Management Studies Master of Business AdministrationDocument15 paginiMakerere University College of Business and Management Studies Master of Business AdministrationDamulira DavidÎncă nu există evaluări

- Assignment 3Document7 paginiAssignment 3Abdullah ghauriÎncă nu există evaluări

- Derivatives Markets: Futures, Options & SwapsDocument20 paginiDerivatives Markets: Futures, Options & SwapsPatrick Earl T. PintacÎncă nu există evaluări

- CAPM GuideDocument15 paginiCAPM GuideEnp Gus AgostoÎncă nu există evaluări

- Chapter 3 Valuation and Cost of CapitalDocument92 paginiChapter 3 Valuation and Cost of Capitalyemisrach fikiruÎncă nu există evaluări

- Income Tax Guide UgandaDocument13 paginiIncome Tax Guide UgandaMoses LubangakeneÎncă nu există evaluări

- Presentation 2. Understanding The Interest Rates. The Yield To MaturityDocument30 paginiPresentation 2. Understanding The Interest Rates. The Yield To MaturitySadia SaeedÎncă nu există evaluări

- 14 Fixed Income Portfolio ManagementDocument60 pagini14 Fixed Income Portfolio ManagementPawan ChoudharyÎncă nu există evaluări

- Duration Convexity Bond Portfolio ManagementDocument49 paginiDuration Convexity Bond Portfolio ManagementParijatVikramSingh100% (1)

- Chapter 12 Bond Portfolio MGMTDocument41 paginiChapter 12 Bond Portfolio MGMTsharktale2828Încă nu există evaluări

- Analyze Transactions Affecting Balance Sheet Items 2. Analyzing Transactions Affecting Income Statement ItemsDocument4 paginiAnalyze Transactions Affecting Balance Sheet Items 2. Analyzing Transactions Affecting Income Statement ItemsRevise PastralisÎncă nu există evaluări

- Narra Vs Redmont and Gamboa Vs Teves CaseDocument132 paginiNarra Vs Redmont and Gamboa Vs Teves CaseAnonymous r1cRm7FÎncă nu există evaluări

- Access Bank PLC and SubsidiariesDocument2 paginiAccess Bank PLC and SubsidiariesRizzleÎncă nu există evaluări

- RD020 Process QuestionnaireDocument1.120 paginiRD020 Process Questionnairesurewaugh100% (1)

- 00f GML System Naaim Final Humphrey LloydDocument34 pagini00f GML System Naaim Final Humphrey Lloydtempor1240Încă nu există evaluări

- Strategic Management: CASE STUDY - Steinway and SonsDocument5 paginiStrategic Management: CASE STUDY - Steinway and SonsNaeem Ul HassanÎncă nu există evaluări

- Bookkeeping NC 3 Review GuideDocument6 paginiBookkeeping NC 3 Review GuideCatherine Hidalgo100% (1)

- Kpo BpoDocument43 paginiKpo Bpogeorgebabyc100% (1)

- BFIDocument14 paginiBFIMc Reidgard RomblonÎncă nu există evaluări

- Investment Appraisal Relevant Cash Flows AnswersDocument8 paginiInvestment Appraisal Relevant Cash Flows AnswersdoannamphuocÎncă nu există evaluări

- Impact of GST On Indian Economy: Vishal Singh Chouhan Mba-Fs 3 SemDocument16 paginiImpact of GST On Indian Economy: Vishal Singh Chouhan Mba-Fs 3 SemstrewÎncă nu există evaluări

- PJC 2010 Prelim H2 Econs P2 (Marking Scheme)Document29 paginiPJC 2010 Prelim H2 Econs P2 (Marking Scheme)incognito2008100% (1)

- Central Bank of Bahrain Volume 3-Insurance PART BDocument26 paginiCentral Bank of Bahrain Volume 3-Insurance PART BZaheer AhmadÎncă nu există evaluări

- Case StudiesDocument158 paginiCase StudiesvijkingÎncă nu există evaluări

- International Financial ManagementDocument25 paginiInternational Financial ManagementNaeem MughalÎncă nu există evaluări

- The Key Benefits of Forming a CorporationDocument12 paginiThe Key Benefits of Forming a CorporationKanwarveer SinghÎncă nu există evaluări

- Dormant CompanyDocument3 paginiDormant CompanyAvaniJainÎncă nu există evaluări

- Unit - 2Document14 paginiUnit - 2sero100% (1)

- TIPS Vs TreasuriesDocument8 paginiTIPS Vs TreasurieszdfgbsfdzcgbvdfcÎncă nu există evaluări

- Arabized Hospital Management System ProjectDocument7 paginiArabized Hospital Management System ProjectSakthi ManojÎncă nu există evaluări

- Bank of PunjabDocument52 paginiBank of Punjabmuhammadtaimoorkhan87% (15)

- Analysis of Arcelor Mittal M&ADocument32 paginiAnalysis of Arcelor Mittal M&Aroli singhÎncă nu există evaluări

- Business Environment Assignment Titan IndustriesDocument8 paginiBusiness Environment Assignment Titan IndustriesAnuj Singh50% (2)

- SWOT Analysis Campaign Bolts and Nuts ProductionDocument7 paginiSWOT Analysis Campaign Bolts and Nuts Productionminimoy86Încă nu există evaluări

- VIETNAM-JAPAN SUPPORTING INDUSTRIES EXHIBITIONDocument116 paginiVIETNAM-JAPAN SUPPORTING INDUSTRIES EXHIBITIONJeffÎncă nu există evaluări

- Clothing Retailers Financial Statements AnalysisDocument15 paginiClothing Retailers Financial Statements Analysisapi-277769092Încă nu există evaluări

- CFA-Quiz #4Document7 paginiCFA-Quiz #4joezh3Încă nu există evaluări

- Tan Lay Hong Family Owned FirmDocument43 paginiTan Lay Hong Family Owned FirmUmar RazakÎncă nu există evaluări

- Hilton Blackstone Case StudyDocument31 paginiHilton Blackstone Case StudyArush Sharma100% (1)

- Chapter 8: International StrategyDocument25 paginiChapter 8: International StrategyKashif Ullah KhanÎncă nu există evaluări