S-ar putea să vă placă și

- Hero Operation ManagementDocument18 paginiHero Operation ManagementtushartatawatÎncă nu există evaluări

- 1.infosys PPT FinalDocument13 pagini1.infosys PPT FinalTapan ShahÎncă nu există evaluări

- Dabur India-CorporateGovernance ReportDocument24 paginiDabur India-CorporateGovernance ReportRomesh Angom100% (1)

- TCS Organizational CultureDocument5 paginiTCS Organizational CultureRohit Kumar100% (1)

- Domino S Jubliant Foodworks Company Analysis PDFDocument32 paginiDomino S Jubliant Foodworks Company Analysis PDFVaishnaviRaviÎncă nu există evaluări

- Research Report - InfosysDocument4 paginiResearch Report - InfosysDishant KhanejaÎncă nu există evaluări

- SM AssignesDocument8 paginiSM AssignesYugandhar MakarlaÎncă nu există evaluări

- Operations Management ReportDocument38 paginiOperations Management ReportFarjana Hossain DharaÎncă nu există evaluări

- HCCB S&M PDFDocument5 paginiHCCB S&M PDFSamdeesh SinghÎncă nu există evaluări

- Tata Consultancy Services Limited: Company BackgroundDocument4 paginiTata Consultancy Services Limited: Company Backgroundrocky360Încă nu există evaluări

- Group 4 - ITC - Live ProjectDocument31 paginiGroup 4 - ITC - Live ProjectSyama kÎncă nu există evaluări

- Kuria S Case Personal OrbitDocument8 paginiKuria S Case Personal OrbitArgha SenÎncă nu există evaluări

- M3 - Valuation Question SetDocument13 paginiM3 - Valuation Question SetHetviÎncă nu există evaluări

- Market Segmentation, Targeting, and Positioning: Iribus - Iveco of ItalyDocument26 paginiMarket Segmentation, Targeting, and Positioning: Iribus - Iveco of ItalySayeed IbrahimÎncă nu există evaluări

- BSNL SwotDocument13 paginiBSNL SwotAbhishek Chaudhary100% (1)

- AshrulDocument58 paginiAshrulNilabjo Kanti Paul100% (2)

- Farmaid Tractor Limited Case StudyDocument2 paginiFarmaid Tractor Limited Case StudyRahul Savalia0% (1)

- Projectonindianautomotiveindustry and Case Study of Tata MotorsDocument26 paginiProjectonindianautomotiveindustry and Case Study of Tata MotorsMukesh Manwani100% (1)

- Financials Infosys Last 5 Years Annual Revenue History and Growth RateDocument7 paginiFinancials Infosys Last 5 Years Annual Revenue History and Growth RateDivyavadan MateÎncă nu există evaluări

- TATA MOTORS Atif PDFDocument9 paginiTATA MOTORS Atif PDFAtif Raza AkbarÎncă nu există evaluări

- Decision Sheet - MdbsDocument3 paginiDecision Sheet - MdbsGayatri BommisettyÎncă nu există evaluări

- Tata Group - Case StudyDocument10 paginiTata Group - Case StudyAbeer ArifÎncă nu există evaluări

- Bharat Electronics LimitedDocument36 paginiBharat Electronics LimiteddipanshuÎncă nu există evaluări

- Infosys Life CycleDocument6 paginiInfosys Life CycleraghupadhyaÎncă nu există evaluări

- Project Report On: Larsen & Toubro Limited (L&T)Document40 paginiProject Report On: Larsen & Toubro Limited (L&T)Rohit D GhuleÎncă nu există evaluări

- Tata Motors: Competitive AdvantageDocument9 paginiTata Motors: Competitive AdvantageAltaf KondakamaralaÎncă nu există evaluări

- Group 13 - Sec B - AEML Blueprint PDFDocument4 paginiGroup 13 - Sec B - AEML Blueprint PDFAmbuj PriyadarshiÎncă nu există evaluări

- Infosys Case - GRP No 3 - Assignment 2Document11 paginiInfosys Case - GRP No 3 - Assignment 2harsh510% (1)

- Pepe Jeans Case Study SolutionDocument8 paginiPepe Jeans Case Study SolutionShivaani AggarwalÎncă nu există evaluări

- A Presentation On WIPRO - MBA 2020 BATCHDocument18 paginiA Presentation On WIPRO - MBA 2020 BATCHAbiÎncă nu există evaluări

- BP and The Consolidation of The Oil IndustryDocument3 paginiBP and The Consolidation of The Oil IndustrySwati VermaÎncă nu există evaluări

- Erp in Tata MotorsDocument3 paginiErp in Tata Motorslakshmibabymani100% (1)

- TCS Marketing PrinciplesDocument2 paginiTCS Marketing PrinciplesAshutosh TulsyanÎncă nu există evaluări

- Talent Managemnt Process in TATA MOTORSDocument2 paginiTalent Managemnt Process in TATA MOTORSAnimesh Jain100% (2)

- Global Operations of TATA GroupDocument28 paginiGlobal Operations of TATA GroupbhavanaÎncă nu există evaluări

- Dabur SCMDocument36 paginiDabur SCMEkta Roy0% (1)

- United Phosphorus LTDDocument90 paginiUnited Phosphorus LTDAashish PrajapatiÎncă nu există evaluări

- Swot Analysis of Om Logistics Limited - 193971474Document2 paginiSwot Analysis of Om Logistics Limited - 193971474Anonymous nepVmXh100% (1)

- Inventory Management Project ReportDocument110 paginiInventory Management Project Reportk eswariÎncă nu există evaluări

- LSCM Assign....Document13 paginiLSCM Assign....ARPITA BAGHÎncă nu există evaluări

- Strategic Plan of Indian Tobacco Company (ItcDocument27 paginiStrategic Plan of Indian Tobacco Company (ItcJennifer Smith100% (1)

- Itc DiversificationDocument22 paginiItc DiversificationEkta SoniÎncă nu există evaluări

- Internal Analysis of InfosysDocument3 paginiInternal Analysis of InfosysWilliam McconnellÎncă nu există evaluări

- MM AssignmentDocument11 paginiMM AssignmentAayush Agrawal100% (1)

- Infosys Case StudyDocument2 paginiInfosys Case StudyPrashasti Tandon0% (1)

- Larsen & Toubro-WPS OfficeDocument5 paginiLarsen & Toubro-WPS OfficeNihal SonkusareÎncă nu există evaluări

- Casestudy Kalsi AgroDocument3 paginiCasestudy Kalsi AgroGPLÎncă nu există evaluări

- TCS A System Approach To Human Resource DevelopmentDocument3 paginiTCS A System Approach To Human Resource DevelopmentPranavPalSingh0% (1)

- TCS - An Organizational OutlookDocument23 paginiTCS - An Organizational OutlookAbhishek MinzÎncă nu există evaluări

- Final ProjectDocument55 paginiFinal Projectshiv infotechÎncă nu există evaluări

- Five Forces Analysis Indian Automobile IndustryDocument10 paginiFive Forces Analysis Indian Automobile IndustryAmit BharwadÎncă nu există evaluări

- Eureka Forbes LimitedDocument77 paginiEureka Forbes LimitedDipanjan DasÎncă nu există evaluări

- Cipla Performance AnalysisDocument33 paginiCipla Performance Analysis9987303726Încă nu există evaluări

- Pearl Global Industries LimitedDocument9 paginiPearl Global Industries LimitedAnisha NandaÎncă nu există evaluări

- VLINK SIP Project ReportDocument51 paginiVLINK SIP Project ReportABHINAV SHANKHDHARÎncă nu există evaluări

- Project MaricoDocument23 paginiProject Maricoharishma29100% (1)

- Dividend Policy PDFDocument45 paginiDividend Policy PDFMaherAh KhAnÎncă nu există evaluări

- Dividend Decision Dividend Decision: Walter and Gordon Model of DividendDocument20 paginiDividend Decision Dividend Decision: Walter and Gordon Model of DividendMayank AnandÎncă nu există evaluări

- Dividend Policy: By:Hina R. AntalaDocument36 paginiDividend Policy: By:Hina R. AntalaHina GajeraÎncă nu există evaluări

- Dividend PolicyDocument24 paginiDividend PolicyAnjali SinghÎncă nu există evaluări

- IBBBBDocument21 paginiIBBBBCtal RajÎncă nu există evaluări

- Ceo IndiaDocument7 paginiCeo IndiaCtal RajÎncă nu există evaluări

- HCL Campus Brochure 2012Document4 paginiHCL Campus Brochure 2012Ctal RajÎncă nu există evaluări

- IB1Document40 paginiIB1Ctal RajÎncă nu există evaluări

- Econ 252 Spring 2011 Problem Set 2 SolutionDocument13 paginiEcon 252 Spring 2011 Problem Set 2 SolutionTu ShirotaÎncă nu există evaluări

- Active CirculantDocument4 paginiActive CirculantPaola AndreaÎncă nu există evaluări

- AbstractDocument6 paginiAbstractFaizan AhmedÎncă nu există evaluări

- Sharekhan ProjectDocument53 paginiSharekhan Projectamitmaurya188% (8)

- Find Ur SelfDocument4 paginiFind Ur SelfMervixShasiÎncă nu există evaluări

- Atlas Fin CaseDocument11 paginiAtlas Fin CaseAniruddhaÎncă nu există evaluări

- List of Books by Author Steven M. BraggDocument5 paginiList of Books by Author Steven M. BraggAriyanto100% (1)

- Putnam White Paper: The Outlook For U.S. and European BanksDocument12 paginiPutnam White Paper: The Outlook For U.S. and European BanksPutnam InvestmentsÎncă nu există evaluări

- Nflplayers Finance 16412 TrueDocument7 paginiNflplayers Finance 16412 Trueapi-313709590Încă nu există evaluări

- Crisostomo Vs SEC DigestDocument1 paginăCrisostomo Vs SEC Digestmelaniem_1Încă nu există evaluări

- Capital One vs. Surrey Equities, Senergy Et AlDocument32 paginiCapital One vs. Surrey Equities, Senergy Et AlJayÎncă nu există evaluări

- China Ritar Power Corp.: Global Energy & Industrials: ChinaDocument5 paginiChina Ritar Power Corp.: Global Energy & Industrials: Chinaanalyst_reportsÎncă nu există evaluări

- Problem 8-19: Answer: C. 9,000,000Document2 paginiProblem 8-19: Answer: C. 9,000,000Kien Alwyn Timola57% (7)

- Financial Accounting Past Present and FutureDocument12 paginiFinancial Accounting Past Present and Futureindri070589Încă nu există evaluări

- Mcs 035Document256 paginiMcs 035Urvashi Roy100% (1)

- Companies Joint Venture Agreement TemplateDocument5 paginiCompanies Joint Venture Agreement TemplateSreeÎncă nu există evaluări

- Amer SWOT AnalysisDocument3 paginiAmer SWOT Analysisshadynader100% (1)

- Choiseul Top100 2019Document64 paginiChoiseul Top100 2019JM KoffiÎncă nu există evaluări

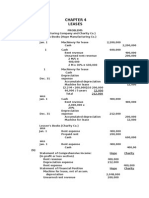

- Financial Accounting 2 Chapter 4Document27 paginiFinancial Accounting 2 Chapter 4Elijah Lou ViloriaÎncă nu există evaluări

- Case Analysis - Arundel PartnersDocument4 paginiCase Analysis - Arundel PartnersEduardo Mira25% (4)

- PensionDocument2 paginiPensionRatna Sari100% (1)

- Assignment On HRM PracticeDocument24 paginiAssignment On HRM PracticeSnowboy Tusher50% (2)

- Nfjpia Mock Board 2016 - AfarDocument8 paginiNfjpia Mock Board 2016 - AfarLeisleiRago50% (2)

- Full Feasibility AnalysisDocument13 paginiFull Feasibility Analysisapi-288010181Încă nu există evaluări

- Sankalp Intervention: Team PrashaktDocument39 paginiSankalp Intervention: Team PrashaktSanjanaÎncă nu există evaluări

- Interim Order in The Matter of Goldmine Industries LimitedDocument14 paginiInterim Order in The Matter of Goldmine Industries LimitedShyam SunderÎncă nu există evaluări

- Epgpx01 Term Iii End Term Examination: Indian Institute of Management RohtakDocument3 paginiEpgpx01 Term Iii End Term Examination: Indian Institute of Management Rohtakkaushal dhapareÎncă nu există evaluări

- Direct Tax Summary Notes For IPCC JKQK1AK0Document24 paginiDirect Tax Summary Notes For IPCC JKQK1AK0Vivek ShimogaÎncă nu există evaluări

- 1 The Importance of Business ProcessesDocument17 pagini1 The Importance of Business ProcessesFanny- Fan.nyÎncă nu există evaluări

- Primer On Investment BankingDocument2 paginiPrimer On Investment BankingRaul KoolÎncă nu există evaluări