S-ar putea să vă placă și

- Section 3 - SwapsDocument49 paginiSection 3 - SwapsEric FahertyÎncă nu există evaluări

- Financial Risk Management - SWAPDocument23 paginiFinancial Risk Management - SWAPChau NguyenÎncă nu există evaluări

- Chapter 4 - Swaps - 2022 - SDocument51 paginiChapter 4 - Swaps - 2022 - SĐức Nam TrầnÎncă nu există evaluări

- Swaps: Options, Futures, and Other John C. Hull 2008Document13 paginiSwaps: Options, Futures, and Other John C. Hull 2008Asim Ali FidaÎncă nu există evaluări

- Swaps: Options, Futures, and Other Derivatives, 8th Edition, 1Document40 paginiSwaps: Options, Futures, and Other Derivatives, 8th Edition, 1trevorsum123Încă nu există evaluări

- Pitele de CapitalDocument14 paginiPitele de CapitalFelix RemeteaÎncă nu există evaluări

- 1 Exercises On Swaps: 5:3% 5:4% Libor +0:6%Document6 pagini1 Exercises On Swaps: 5:3% 5:4% Libor +0:6%Rimpy SondhÎncă nu există evaluări

- Swaps: Prof Mahesh Kumar Amity Business SchoolDocument27 paginiSwaps: Prof Mahesh Kumar Amity Business SchoolasifanisÎncă nu există evaluări

- Swaps: Prof Mahesh Kumar Amity Business SchoolDocument21 paginiSwaps: Prof Mahesh Kumar Amity Business SchoolasifanisÎncă nu există evaluări

- Swaps: Prof Mahesh Kumar Amity Business SchoolDocument51 paginiSwaps: Prof Mahesh Kumar Amity Business SchoolasifanisÎncă nu există evaluări

- Example SwapDocument10 paginiExample SwapThanh Huyền TrầnÎncă nu există evaluări

- 03 InterestRateSwapsDocument123 pagini03 InterestRateSwapsAlexandra Hsiajsnaks100% (1)

- Sample Questions For SWAPDocument4 paginiSample Questions For SWAPKarthik Nandula100% (1)

- Lecture 6Document32 paginiLecture 6Nilesh PanchalÎncă nu există evaluări

- Interest Rate RiskDocument58 paginiInterest Rate RiskStevan PknÎncă nu există evaluări

- Hull OFOD10 e Solutions CH 07Document12 paginiHull OFOD10 e Solutions CH 07Vishal GoyalÎncă nu există evaluări

- Interest Rate and Currency SwapsDocument33 paginiInterest Rate and Currency SwapsMatt ToothacreÎncă nu există evaluări

- Fabozzi Ch29 BMAS 7thedDocument43 paginiFabozzi Ch29 BMAS 7thedPropertywizzÎncă nu există evaluări

- AssignmentFinance 7495Document10 paginiAssignmentFinance 7495IshitaaÎncă nu există evaluări

- SwapsDocument16 paginiSwapsLuvnica VermaÎncă nu există evaluări

- Lecture - Interest Rate SwapDocument26 paginiLecture - Interest Rate SwapKamran AbdullahÎncă nu există evaluări

- Currency SwapsDocument33 paginiCurrency SwapsManasvi ShahÎncă nu există evaluări

- Using The Swap To Transform A LiabilityDocument2 paginiUsing The Swap To Transform A LiabilityThuỷ TrìnhÎncă nu există evaluări

- CH 07 Hull Fundamentals 8 The DDocument47 paginiCH 07 Hull Fundamentals 8 The DjlosamÎncă nu există evaluări

- Slides8 StudentDocument39 paginiSlides8 StudentkmeetheebsÎncă nu există evaluări

- Swaps and Interest Rate DerivativesDocument20 paginiSwaps and Interest Rate DerivativesShankar VenkatramanÎncă nu există evaluări

- Currency and Interest Rate Swaps: Chapter TenDocument22 paginiCurrency and Interest Rate Swaps: Chapter TenNitin MahindrooÎncă nu există evaluări

- Swaps ProblemsDocument2 paginiSwaps ProblemsSapcultÎncă nu există evaluări

- Derivaties AnswersDocument3 paginiDerivaties AnswersDavid DelvalleÎncă nu există evaluări

- SwapsDocument44 paginiSwapsAditya Paul SharmaÎncă nu există evaluări

- Chapter - 7 - Solution Hull Option, Futures and Other DerivativesDocument3 paginiChapter - 7 - Solution Hull Option, Futures and Other DerivativesAn Kou0% (1)

- Swaps: Problem 7.1Document4 paginiSwaps: Problem 7.1Hana LeeÎncă nu există evaluări

- @note 6 Ch07Hull-swap - PrintDocument66 pagini@note 6 Ch07Hull-swap - PrintzZl3Ul2NNINGZzÎncă nu există evaluări

- FIN30014 - Week 9Document33 paginiFIN30014 - Week 9Jason DanielÎncă nu există evaluări

- 14 Interest Rate and Currency SwapsDocument28 pagini14 Interest Rate and Currency SwapslalitjaatÎncă nu există evaluări

- Swap Contract: What Is Swaps?Document12 paginiSwap Contract: What Is Swaps?Ubraj NeupaneÎncă nu există evaluări

- Levich Ch13 Net Assignment SolutionsDocument24 paginiLevich Ch13 Net Assignment Solutionsveda20Încă nu există evaluări

- FMI7e ch15Document39 paginiFMI7e ch15lehoangthuchienÎncă nu există evaluări

- SwapsDocument19 paginiSwapsUtsav ThakkarÎncă nu există evaluări

- Interest Rate Swaps Currency Swaps Chapter 9Document20 paginiInterest Rate Swaps Currency Swaps Chapter 9armando.chappell1005Încă nu există evaluări

- Chapter 13 Currency and Interest Rate SwapsDocument24 paginiChapter 13 Currency and Interest Rate SwapsaS hausjÎncă nu există evaluări

- Currency and Interest Rate Swaps: Chapter TenDocument22 paginiCurrency and Interest Rate Swaps: Chapter TenEvan SwagerÎncă nu există evaluări

- Swap ContractsDocument11 paginiSwap ContractsSanya rajÎncă nu există evaluări

- Interest Rate Swap: Odie PichappanDocument11 paginiInterest Rate Swap: Odie PichappanManish AnandÎncă nu există evaluări

- EFB344 Lecture07, FRAs and SwapsDocument35 paginiEFB344 Lecture07, FRAs and SwapsTibet LoveÎncă nu există evaluări

- HW NongradedDocument4 paginiHW NongradedAnDy YiMÎncă nu există evaluări

- Derivatives PresentationDocument62 paginiDerivatives Presentationivyfinest100% (1)

- BOBODocument3 paginiBOBO杜顺历Încă nu există evaluări

- SwapsDocument38 paginiSwapsNavleen KaurÎncă nu există evaluări

- Swaps: Interest Rate SwapDocument9 paginiSwaps: Interest Rate Swapdinesh8maharjanÎncă nu există evaluări

- Financial Engineering C3 Assessment: Submitted By: Mohammad Sameer Ansari (IMB2020008)Document1 paginăFinancial Engineering C3 Assessment: Submitted By: Mohammad Sameer Ansari (IMB2020008)Mohammad Sameer AnsariÎncă nu există evaluări

- Session 6 - FDDocument26 paginiSession 6 - FDDaksh KhullarÎncă nu există evaluări

- SwapDocument37 paginiSwapRitik MishraÎncă nu există evaluări

- Swaps NewDocument46 paginiSwaps NewJoseph Anbarasu100% (5)

- Interest Rate Parity, Money Market Basis Swaps, and Cross-Currency Basis SwapsDocument14 paginiInterest Rate Parity, Money Market Basis Swaps, and Cross-Currency Basis Swapsultr4l0rd100% (1)

- The Pros and Cons of Closed-End Funds: How Do You Like Your Income?: Financial Freedom, #136De la EverandThe Pros and Cons of Closed-End Funds: How Do You Like Your Income?: Financial Freedom, #136Încă nu există evaluări

- Personal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyDe la EverandPersonal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyÎncă nu există evaluări

- Financial Risk Management: A Simple IntroductionDe la EverandFinancial Risk Management: A Simple IntroductionEvaluare: 4.5 din 5 stele4.5/5 (7)

- Nelson Mckee Has Been Filing Agent For 908 Registrants Such As Jpmac, Deutsche, PHH, Lehman, Thornburg, HarborviewDocument23 paginiNelson Mckee Has Been Filing Agent For 908 Registrants Such As Jpmac, Deutsche, PHH, Lehman, Thornburg, Harborview83jjmackÎncă nu există evaluări

- Malamaal Weekly Fund: Investment StrategyDocument2 paginiMalamaal Weekly Fund: Investment StrategyVishant ChopraÎncă nu există evaluări

- IAS 12 - Income Tax: Prepared By: Sir Hamza Abdul HaqDocument33 paginiIAS 12 - Income Tax: Prepared By: Sir Hamza Abdul HaqSrabon BaruaÎncă nu există evaluări

- Assignment 6 SolutionsDocument4 paginiAssignment 6 SolutionsjoanÎncă nu există evaluări

- General Banking PDFDocument394 paginiGeneral Banking PDFSeenu Vaas100% (2)

- Compound Interest and SIDocument2 paginiCompound Interest and SISanathoi MaibamÎncă nu există evaluări

- Funds Flow Theory PDFDocument7 paginiFunds Flow Theory PDFLalrinfela RalteÎncă nu există evaluări

- Rika Ristiani - Akuntansi Keuangan Menengah 2 - TM-02Document5 paginiRika Ristiani - Akuntansi Keuangan Menengah 2 - TM-02MARCHO AGUSTAÎncă nu există evaluări

- Separate Financial Statements: International Accounting Standard 27Document5 paginiSeparate Financial Statements: International Accounting Standard 27Maruf HossainÎncă nu există evaluări

- Apply Principles of Professional PracticeDocument15 paginiApply Principles of Professional PracticeBelay Kassahun100% (2)

- Supreme Team FlyerDocument1 paginăSupreme Team FlyerMichael HaighÎncă nu există evaluări

- NBFC Compliance and Return - Taxguru - inDocument7 paginiNBFC Compliance and Return - Taxguru - incaaashishupadhyay9579Încă nu există evaluări

- Comparative Study of Loans and Advances of Commercial BanksDocument22 paginiComparative Study of Loans and Advances of Commercial BanksNoaman AkbarÎncă nu există evaluări

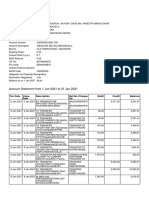

- Account Statement PDFDocument12 paginiAccount Statement PDFYuvraj Gogoi100% (1)

- Tugas 2 Akuntansi ManajemenDocument3 paginiTugas 2 Akuntansi ManajemenSherlin KhuÎncă nu există evaluări

- Sbi Account Jan 2021Document2 paginiSbi Account Jan 2021Manoj GaurÎncă nu există evaluări

- IBIG 04 03 Projecting 3 StatementsDocument76 paginiIBIG 04 03 Projecting 3 Statements0 5Încă nu există evaluări

- FGV-36590658 Dated 05.10.2022 at 16.11.2022Document5 paginiFGV-36590658 Dated 05.10.2022 at 16.11.2022Suhada DaudÎncă nu există evaluări

- Audited Consolidated Financial StatementDocument42 paginiAudited Consolidated Financial StatementAbigail EjiroÎncă nu există evaluări

- Chapter 6Document20 paginiChapter 6Federico MagistrelliÎncă nu există evaluări

- ASR3 Materials - Auditing Equity and Debt InvestmentsDocument4 paginiASR3 Materials - Auditing Equity and Debt InvestmentsHannah Jane ToribioÎncă nu există evaluări

- Nigerian - Banks Fitch Mar17Document12 paginiNigerian - Banks Fitch Mar17Funso Ade100% (1)

- Your Commercial Card Statement: MR Imran Munir Narmi Limited 19 Thorpe Road London E17 4LADocument4 paginiYour Commercial Card Statement: MR Imran Munir Narmi Limited 19 Thorpe Road London E17 4LAaoshi321Încă nu există evaluări

- GovAcc HO No. 3 - The Government Accounting ProcessDocument9 paginiGovAcc HO No. 3 - The Government Accounting Processbobo kaÎncă nu există evaluări

- Exam Schedule Winter 2016Document1 paginăExam Schedule Winter 2016Don't SayÎncă nu există evaluări

- IC Real Estate Customer Database 11256Document2 paginiIC Real Estate Customer Database 11256SATISH WORDBOXÎncă nu există evaluări

- View Invoice - ReceiptDocument1 paginăView Invoice - Receiptspeak2ebiniÎncă nu există evaluări

- Fraud Risk Assessment: An Empirical AnalysisDocument11 paginiFraud Risk Assessment: An Empirical AnalysisGDPÎncă nu există evaluări

- Merrick Bank DepositDocument2 paginiMerrick Bank DepositSeth Alley100% (1)

- Rahul Sir Maths Questions Special of Compound InterestDocument3 paginiRahul Sir Maths Questions Special of Compound InterestAnjan BahugunaÎncă nu există evaluări