S-ar putea să vă placă și

- Practical Guides to Testing and Commissioning of Mechanical, Electrical and Plumbing (Mep) InstallationsDe la EverandPractical Guides to Testing and Commissioning of Mechanical, Electrical and Plumbing (Mep) InstallationsEvaluare: 3.5 din 5 stele3.5/5 (3)

- Analysis of CostsDocument26 paginiAnalysis of CostsTanvi ThakurÎncă nu există evaluări

- Theory of CostsDocument39 paginiTheory of CostsAbu Aalif Rayyan100% (2)

- Cost AnalysisDocument48 paginiCost AnalysisSADEEQ AKBARÎncă nu există evaluări

- Theory of Production CostDocument17 paginiTheory of Production CostDherya AgarwalÎncă nu există evaluări

- Costs of ProductionDocument15 paginiCosts of Productionchaudhary samavaÎncă nu există evaluări

- Cost Analysis: Mr. P. Nandakumar Assistant Professor KvimisDocument27 paginiCost Analysis: Mr. P. Nandakumar Assistant Professor KvimisNanda KumarÎncă nu există evaluări

- Presentation ON COST : By:-Alok MadhavDocument16 paginiPresentation ON COST : By:-Alok MadhavAlok MadhavÎncă nu există evaluări

- CostDocument23 paginiCostManish GuptaÎncă nu există evaluări

- 2.4.theory of CostDocument28 pagini2.4.theory of CostMotuma AdugnaÎncă nu există evaluări

- Short Run Costs: Dr. Rakesh Kumar Sharma SBSBS, Thapar University PatialaDocument41 paginiShort Run Costs: Dr. Rakesh Kumar Sharma SBSBS, Thapar University PatialaJohn SteveÎncă nu există evaluări

- Cost AnalysisDocument17 paginiCost AnalysisrohityadavalldÎncă nu există evaluări

- CH 7 Costs of Production Spring 2023Document52 paginiCH 7 Costs of Production Spring 2023sayidÎncă nu există evaluări

- Fy Eco - Mod 3Document34 paginiFy Eco - Mod 3MOHINI NADKARNIÎncă nu există evaluări

- CA CPT Micro Economics PPT Theory of CostDocument119 paginiCA CPT Micro Economics PPT Theory of CostShobi DionelaÎncă nu există evaluări

- Cost Short Run and Long RunDocument78 paginiCost Short Run and Long Run0241ASHAYÎncă nu există evaluări

- Cost FunctionDocument58 paginiCost FunctionAishwarya ChauhanÎncă nu există evaluări

- Introduction To Economics (Econ. 101)Document31 paginiIntroduction To Economics (Econ. 101)Nahom MasreshaÎncă nu există evaluări

- Cost AnalysisDocument20 paginiCost AnalysisManoj NagÎncă nu există evaluări

- 7b5f53 Analysis of Cost and Revenue 25-04Document21 pagini7b5f53 Analysis of Cost and Revenue 25-04Shamsuddin SheikhÎncă nu există evaluări

- Module 3Document21 paginiModule 3sujal sikariyaÎncă nu există evaluări

- Cost of ProductionDocument61 paginiCost of ProductionPankit KediaÎncă nu există evaluări

- The Theory and Estimation of Cost: Unit-IVDocument26 paginiThe Theory and Estimation of Cost: Unit-IVSurya NarayanaÎncă nu există evaluări

- Managerial Economics: Cost Analysis (Document20 paginiManagerial Economics: Cost Analysis (Pankaj BhardwajÎncă nu există evaluări

- CFO CH 8Document55 paginiCFO CH 8ashchua21Încă nu există evaluări

- Introduction To Economics (Econ. 101)Document27 paginiIntroduction To Economics (Econ. 101)Ali HassenÎncă nu există evaluări

- Module-6 Cost and Revenue AnalysisDocument46 paginiModule-6 Cost and Revenue Analysiskarthik21488Încă nu există evaluări

- Costs of Production Concepts and Short Run Cost CurvesDocument174 paginiCosts of Production Concepts and Short Run Cost Curvesjawahar babuÎncă nu există evaluări

- Cost Analysis: Dr. Mohsina HayatDocument36 paginiCost Analysis: Dr. Mohsina HayatFaizan QudsiÎncă nu există evaluări

- Lec06 Cost Concepts & Interrelations - Optimum Level of Input Use and Optimum ProductionDocument8 paginiLec06 Cost Concepts & Interrelations - Optimum Level of Input Use and Optimum ProductionAZIZRAHMANABUBAKARÎncă nu există evaluări

- Theory of Cost NewDocument4 paginiTheory of Cost NewMahesh ViswanathanÎncă nu există evaluări

- Production and Cost FunctionDocument42 paginiProduction and Cost FunctionHealthEconomics_USaNÎncă nu există evaluări

- Chapter11 - Production-And-Cost-Analysis1Document24 paginiChapter11 - Production-And-Cost-Analysis1Sandara beldoÎncă nu există evaluări

- COST - Economics11Document24 paginiCOST - Economics11Nishita SharmaÎncă nu există evaluări

- GRP PPT Cost CurvesDocument49 paginiGRP PPT Cost Curvesparulmathur85Încă nu există evaluări

- Cost and Revenue Curves: Relationship Between AR and MR, Price Elasticity of Demand and RevenueDocument19 paginiCost and Revenue Curves: Relationship Between AR and MR, Price Elasticity of Demand and RevenueNitesh BhattaraiÎncă nu există evaluări

- BIE201 Handout03Document22 paginiBIE201 Handout03andersonmapfirakupaÎncă nu există evaluări

- AGRIDocument10 paginiAGRIwangolo EmmanuelÎncă nu există evaluări

- PAN African E-Network Project D B M: Iploma in Usiness AnagementDocument77 paginiPAN African E-Network Project D B M: Iploma in Usiness AnagementOttilieÎncă nu există evaluări

- Traditional and Modern Theory of Cost)Document39 paginiTraditional and Modern Theory of Cost)LALIT SONDHI100% (4)

- COST ConceptsDocument22 paginiCOST ConceptsPriya KalaÎncă nu există evaluări

- The Costs of Production: Ayesha Afzal Assistant Professor Lahore School of EconomicsDocument19 paginiThe Costs of Production: Ayesha Afzal Assistant Professor Lahore School of EconomicsAsad KhanÎncă nu există evaluări

- Unit 4 Cost and RevenueDocument59 paginiUnit 4 Cost and RevenueSangam KarkiÎncă nu există evaluări

- Theory of CostDocument23 paginiTheory of CostAnwesha KarmakarÎncă nu există evaluări

- MN 304 - Production Economics - 6Document59 paginiMN 304 - Production Economics - 6Nipuna Thushara WijesekaraÎncă nu există evaluări

- Cost Function NotesDocument7 paginiCost Function Noteschandanpalai91100% (1)

- Econ IIDocument28 paginiEcon IIworkinehamanuÎncă nu există evaluări

- Concept of CostDocument41 paginiConcept of CostgunjanporwalÎncă nu există evaluări

- Microeconomics Group - 2Document99 paginiMicroeconomics Group - 2auhsoj raluigaÎncă nu există evaluări

- 2 - Chapter 5 - Supply Decision - Short & Long Run CostDocument38 pagini2 - Chapter 5 - Supply Decision - Short & Long Run CostHadilÎncă nu există evaluări

- Managerial Economics Cost and Production AnalysisDocument39 paginiManagerial Economics Cost and Production AnalysisDr Gayatri GuptaÎncă nu există evaluări

- Theory of CostDocument42 paginiTheory of CostSujan BhattaraiÎncă nu există evaluări

- ECO 211 Week 9 Lectures - Theory of CostDocument33 paginiECO 211 Week 9 Lectures - Theory of CostClaireÎncă nu există evaluări

- Analysis of Cost and RevenueDocument28 paginiAnalysis of Cost and RevenueSaurav SubediÎncă nu există evaluări

- CostDocument23 paginiCostsneh2k10Încă nu există evaluări

- Theory of Cost and ProfitDocument25 paginiTheory of Cost and ProfitFaisal C. LivaraÎncă nu există evaluări

- TopicThree-Theory of Costs-ECO 401Document18 paginiTopicThree-Theory of Costs-ECO 401Mister PhilipsÎncă nu există evaluări

- Cost Concepts: Dr. Saad NawazDocument16 paginiCost Concepts: Dr. Saad NawazArslan MunawarÎncă nu există evaluări

- Lecture 5 & 6: Theory of CostsDocument14 paginiLecture 5 & 6: Theory of CoststagashiiÎncă nu există evaluări

- Theory of Cost: Sonu ChowdhuryDocument21 paginiTheory of Cost: Sonu Chowdhuryzahra naheedÎncă nu există evaluări

- Mba TitlesDocument6 paginiMba Titlesanmol_singh_27Încă nu există evaluări

- What Is Urban PlannigDocument4 paginiWhat Is Urban PlannigDesy Mulyasari DesyÎncă nu există evaluări

- Magazine Nov 2022Document62 paginiMagazine Nov 2022fatrag amloÎncă nu există evaluări

- Taxes: Part One: Obliged ToDocument4 paginiTaxes: Part One: Obliged ToStaciaRevianyMegeÎncă nu există evaluări

- For Reading DevelopmentDocument5 paginiFor Reading DevelopmentJayson DapitonÎncă nu există evaluări

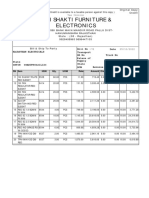

- Shri Shakti Furniture & Electronics: Credit OrginalDocument1 paginăShri Shakti Furniture & Electronics: Credit OrginalRahul BansalÎncă nu există evaluări

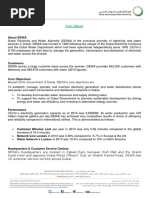

- Dewa FactDocument3 paginiDewa FactfayasÎncă nu există evaluări

- RBHDocument38 paginiRBHjerkÎncă nu există evaluări

- Peter Thiel Lecture Set - Stanford University CS183Document267 paginiPeter Thiel Lecture Set - Stanford University CS183Johanna Lopez100% (1)

- CRUDIFY - The Best Crude Oil Intraday Trading StrategyDocument11 paginiCRUDIFY - The Best Crude Oil Intraday Trading StrategyRajeswaran DhanagopalanÎncă nu există evaluări

- Welcome To Indian Railway Passenger Reservation EnquiryDocument2 paginiWelcome To Indian Railway Passenger Reservation EnquiryChhaviÎncă nu există evaluări

- Walmart Economic IndicatorsDocument10 paginiWalmart Economic IndicatorsJennifer Scott100% (1)

- Diajukan OlehDocument23 paginiDiajukan OlehdheaÎncă nu există evaluări

- Bangalore Architects and Builders 2014-15 Edition - ArchitectsDocument4 paginiBangalore Architects and Builders 2014-15 Edition - ArchitectsAnisha LaluÎncă nu există evaluări

- Pension Plan Reporting of Foreign Bank and Financial AccountsDocument3 paginiPension Plan Reporting of Foreign Bank and Financial AccountsCorey Slagle100% (1)

- SOAL LATIHAN INTER 1 - Chapter 4Document14 paginiSOAL LATIHAN INTER 1 - Chapter 4Florencia May67% (3)

- Arbitration CaselistDocument12 paginiArbitration CaselistDaniel FordanÎncă nu există evaluări

- Chapter 2Document14 paginiChapter 2Pantaleon EdilÎncă nu există evaluări

- Cas Final ReportDocument15 paginiCas Final ReportMaria KochańskaÎncă nu există evaluări

- 08 LSF - Load Momment IndicatorDocument4 pagini08 LSF - Load Momment IndicatorenharÎncă nu există evaluări

- Don't Support Nuclear Energy!Document2 paginiDon't Support Nuclear Energy!koreangoldfishÎncă nu există evaluări

- Questionnaire Organic FoodDocument4 paginiQuestionnaire Organic FoodYuvnesh Kumar50% (2)

- Your Next Holiday DestinationDocument11 paginiYour Next Holiday DestinationReyna BautistaÎncă nu există evaluări

- Catalogo GROFE IngDocument50 paginiCatalogo GROFE IngAlvaro Antonio Cristobal AtencioÎncă nu există evaluări

- Engineering Economy Chapter # 02Document55 paginiEngineering Economy Chapter # 02imran_chaudhryÎncă nu există evaluări

- DCPD Editorial Ebook Till Sep 29, 19Document181 paginiDCPD Editorial Ebook Till Sep 29, 19segnumutraÎncă nu există evaluări

- SA Climate Action and Adaptation PlanDocument92 paginiSA Climate Action and Adaptation PlanDavid IbanezÎncă nu există evaluări

- Gulf Business - April 2011Document92 paginiGulf Business - April 2011motivatepublishingÎncă nu există evaluări

- Statistik MBADocument41 paginiStatistik MBAFarisÎncă nu există evaluări

- Establishing A Stock Exchange in Emerging Economies: Challenges and OpportunitiesDocument7 paginiEstablishing A Stock Exchange in Emerging Economies: Challenges and OpportunitiesJean Placide BarekeÎncă nu există evaluări